Kotak has lower debt to equity ratio (<5.00x) than other 3 (>6.5x), which means they are using higher proportion of their own funds (which has no interest cost associated with it). Another metric to check can be Interest spread, (Interest yield-Cost of funds, ignores effects of leverage)

I do not know if there is difference in customer segments, haven’t studied the business in detail.

Posts in category Value Pickr

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (18-08-2024)

Sky Gold ltd. – Will it reach the sky? (18-08-2024)

Sky Gold covered in this blog

I am just sharing

dr.vikas

Persistent Systems-Potential Multibagger (18-08-2024)

ok got it thr was stock split…nseindia trendlyne doesnt update past quarters data…

Companies With First ever concalls OR Investor Presentations (18-08-2024)

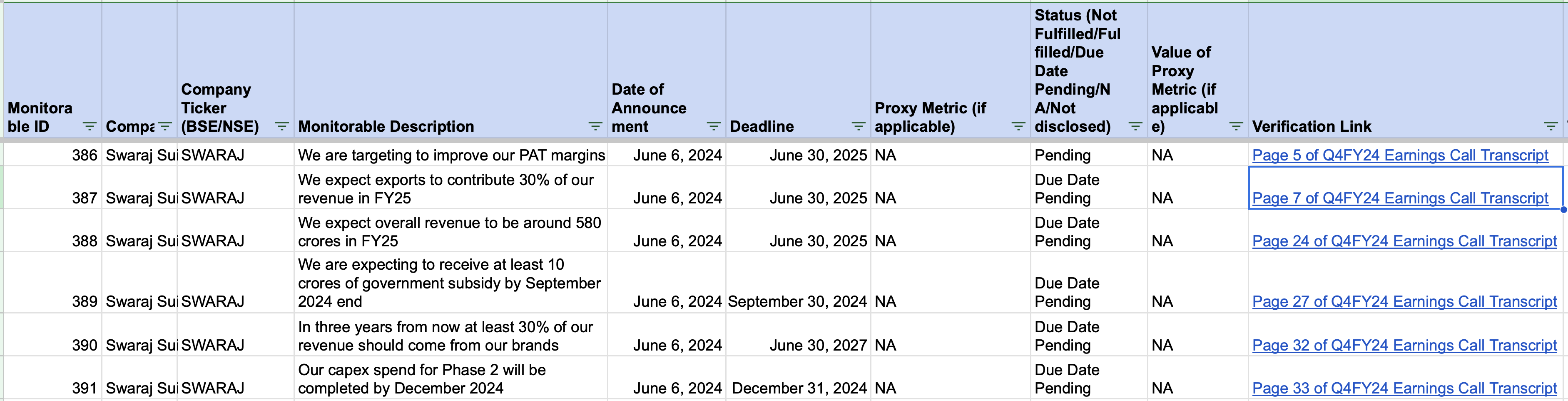

Swaraj Suitings did their first concall

SWARAJ_12062024134352_Regu30InvestorMeetTranscript.pdf (554.9 KB)

In the below tracker, I have started tracking important company goals for Swaraj Suitings. These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

- Company Ticker: For identifying the company

- Monitorable Description: Description of the goal or metric being tracked

- Date of Announcement: When the monitorable was announced

- Deadline: Target date for achieving the monitorable

- Status: Current progress (e.g., Not Fulfilled, Pending)

- Verification Link: A link to see where I got the information about the goal.

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables-24.xlsx (143.0 KB)

Post Script: DM if you want me to track the monitorables for any specific company.

Persistent Systems-Potential Multibagger (18-08-2024)

why is basic & diluted EPS for Jun’23 quarter different in consolidated statement filed this year and last year?

in Current filing it is 15.25 & 14.87 for Jun’23 quarter

last year filing its 30.5 & 29.75

Fineotex Chemical Limited (FCL) (18-08-2024)

-

Consolidated revenue of INR 1,419 million for Q1 FY2025, up 7.3% year-over-year

-

EBITDA of INR 353 million, up 11.8% YoY, with 24.8% margin

-

PAT of INR 292 million, up 11.7% YoY, with 20.6% margin

-

Textile segment: 46% of revenue

-

Cleaning and hygiene segment: 54% of revenue

-

Successfully raised INR 3,425 million through preferential allotment to support growth

-

Appointed Dr. Amit Prabhakar Pratap as Additional Director to leverage his expertise

-

Exploring manufacturing partnerships with Eurodye in Asia to improve efficiency

-

Focus on sustainable and eco-friendly product lines

-

Expansion into international textile hubs over past 3 years

-

Ongoing development of new products to meet changing customer demands

-

Textile industry showing signs of recovery after a challenging 2023

-

Geopolitical issues and container shortages impacting shipping and raw material costs

-

Increased freight costs and container shortages presenting challenges

-

Currency fluctuations impacting costs

-

Company aims to repeat performance of last 3-4 years in coming years

-

Expects to maintain comfortable EBITDA and gross margins

-

Funds raised will be used for organic and inorganic growth opportunities

-

New facility expected to be operational by end of current financial year

-

Opportunities in sustainable solutions for textile and cleaning industries

-

Increasing demand in textile sector as inventory levels normalize

-

Growing interest in sustainable solutions from customers

Garware Hi-tech films (Earlier Garware polyester) (18-08-2024)

First of all, great observation!!!

But I have one counter arguments:-

If the company purchased a piece of land for ₹100 cr, then it means it spent only ₹100 cr to use that piece of land, and hence, whatever profits it earns in next 20 years, or 50 years, it should be valued on the basis of ₹100 cr only, not the ₹1500 cr, because the difference ₹1400 was never spent. And whenever it decides to sell the land for, say ₹1500 cr at CMP, the ₹1400 cr will come as profit automatically.

RACL Geartech Limited (18-08-2024)

**Takeaways from chairman message **

- RACL Geartech achieved annual revenues of ₹42,303.55 Lakhs, a significant increase from last year’s ₹36,734.37 Lakhs.

- EBITDA grew to ₹10,192 Lakhs, marking a 12.4% increase year-over-year.

- The Gajraula Plant became 100% compliant with green electrical energy from January 1, 2024.

- RACL was nominated as a Tier 1 supplier by a German car manufacturer for their Parking Lock Mechanism for electric vehicles.

- They received a nomination from another German customer for supplying gears for pedal-assisted electric bicycle gearboxes.

- The company won First Prize in the Engineering product category for “Highest Export Performance for FY 2022-23” from the UP government.

- Optimistic about maintaining healthy growth in FY 2024-25 and beyond.

Global economy and Indian economy:

- The global economy is showing signs of growth but faces risks from high debt levels and geopolitical conflicts.

- India is poised to become the third-largest economy by 2027, surpassing Japan and Germany.

- India achieved a growth rate of 8.2% for FY 2023-24, driven primarily by government infrastructure investments.

- Challenges include geopolitical tensions, fluctuations in financial markets, trade disruptions, and extreme weather events.

Global automobile industry:

- Projected to grow from USD 29.09 billion in 2023 to USD 42.86 billion by 2032 (CAGR of 4.4%).

- Facing transformations like the shift to electrified powertrains and focus on software differentiation.

- China surpassed Germany in light-vehicle exports in 2022.

- Challenges include declining demand, socio-demographic changes, shift to EVs, and financial pressures on suppliers.

Indian automobile industry:

- Two-wheeler segment leads the market due to growing middle class and young population.

- Achieved record passenger vehicle sales of 393,074 units in January 2024.

- EV market expected to reach US$ 7.09 billion by 2025.

- Government supports 100% FDI through automatic route and has extended the PLI scheme for the sector.

Auto components industry in India:

- Turnover stood at Rs. 2.9 lakh crore (US$ 36.1 billion) in H1 2023-24, with 12.6% revenue growth.

- Exports grew by 2.7% to Rs. 85,870 crore (US$ 10.4 billion) in H1 2023-24.

- Expected to contribute 5-7% to India’s GDP by 2026.

- Focus on sustainable solutions, lightweight materials, and efficient production processes.

Industry Impact:

- Represents 2.3% of India’s GDP and employs over 1.5 million people.

- Consists of businesses of all sizes, from large corporations to small enterprises.

Investment landscape:

- FDI inflow of US$ 35.65 billion from April to December 2023.

- Government aims for 30% of all vehicles to be electric by 2030.

Opportunities:

- Demand for fuel-efficient vehicles in emerging markets.

- Changing lifestyles and consumer preferences driving growth.

- Market expansion into Asian and BRIC nations.

Strengths:

- Ongoing growth of the automobile sector.

- Innovation and technology investments, especially in EVs and alternative fuels.

- Cost management through manufacturing facilities in Asia.

Threats:

- Intense competition in the industry.

- Economic issues like recessions and unemployment.

- Fuel price fluctuations affecting consumer choices.

Weaknesses:

- High consumer bargaining power in a demand-driven market.

- Government regulations impacting growth.

- High employee turnover and difficulty in retaining skilled workers.

Awards and recognition:

- Gajraula plant became 100% Green Electrical Energy compliant.

- First Prize for Highest Export Performance from UP Government.

- Nomination for supplying gears for electric bicycle gearboxes.

- Partnership with BMW Motorrad as title sponsor for GS Trophy India Qualifier.

- Nomination as Tier 1 supplier for Parking Lock Mechanism for electric cars.

Performance overview and key developments:

- Total revenue of Rs 423.03 Crore in FY 2023-24.

- Exports accounted for 73% of total sales, domestic sales 27%.

- Revenue increased by 15.16%, EBITDA by 12.39%, and Profit Before Tax by 4.69% compared to previous year.

- Diversified product portfolio with growth in passenger car and commercial vehicle segments.

- Focus on technological upgrades, skill development, and quality enhancement to meet future mobility challenges.

Small Pharma, Big Dreams: Inside Sanjivani Paranteral’s Growth Plan (18-08-2024)

Possible Turnaround. This article by Nuvama gives a historical perspective also. Very high risk as the account was NPA and restructured. Taken a small position when i saw entry of Ashish Kacholia & Monika Garware.

My portfolio updates and investment journey (18-08-2024)

Sir please share your thoughts on Strides pharma.