https://x.com/drjimmy2407/status/1824667061764644977?t=1Wz01TNPTpRDtWBif2ecvw&s=19

Some SME companies guiding for good growth for next 1-2 years

https://x.com/drjimmy2407/status/1824667061764644977?t=1Wz01TNPTpRDtWBif2ecvw&s=19

Some SME companies guiding for good growth for next 1-2 years

(post deleted by author)

IEX weekly chart you have put up shows a nice rounding structure. The early bottom phase of the rounding structure is as marked by you by horizontal range in lighter shade. In these kind of structures, the targets to look out for are usually the previous tops or all time highs visible on the structure.

Fundamentally I don’t track IEX too closely, (it is vulnerable to govt regulations and diktats) but overall chart structure looks good.

The whole roadmap of finding out sectors to look out for is laid out in the previous post. That should provide some idea about how to go about things, rather than me spoon feeding regarding sectors and stocks. Whenever I find any good idea at that point of time at an attractive entry price, I share it on 52 weeks high thread.

Currently we are in a broad based bull run and hence there will be a lot of sectors showing strength, or signs of reversal etc.

I agree with this analysis, I am getting veey similar figures. I assumed a networth of 25k but it all depends on dividend payout. Anyways, PAT is expected to be min 4000cr.

Given all this, I am very surprised at why DIIs are not showing interest. What is the anti thesis here?

I do not see any capital risk, maybe lower ROA but with Aset light model, ROE is more apt. Eitherway, I do not understand the downside risk that market seems to be assigning here.

Hi, I am unable to understand how this company alone can generate OPMs 10pc ++ higher than their peers large or small, the answers given in the call on overheads and procurement don’t seem convincing. Surely atleast one of their peers would know how to operate like them?

Portfolio Update Aug 2024

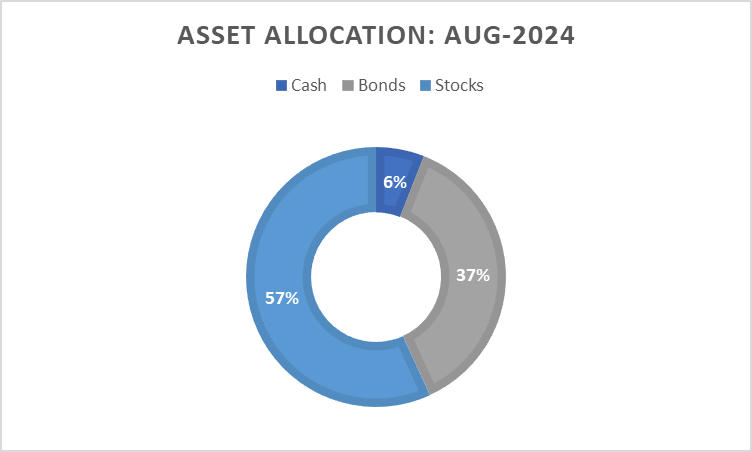

Asset allocation:

Equity allocation is now tending towards my target of 60%, now at 57% (vs. last quarter at 49%). Half of the change has come due to equity run up in last 3 months and half due to sale of my debt mutual fund which i deployed in equity during election and budget dips. I was also able to trim my direct bond holdings wherever liquidity was available.

I beleive it will be very difficult for me to acheive 60% equity allocation target if market does not show a dip. Cash level (6%) is higher than last quarter due to some profit taking.

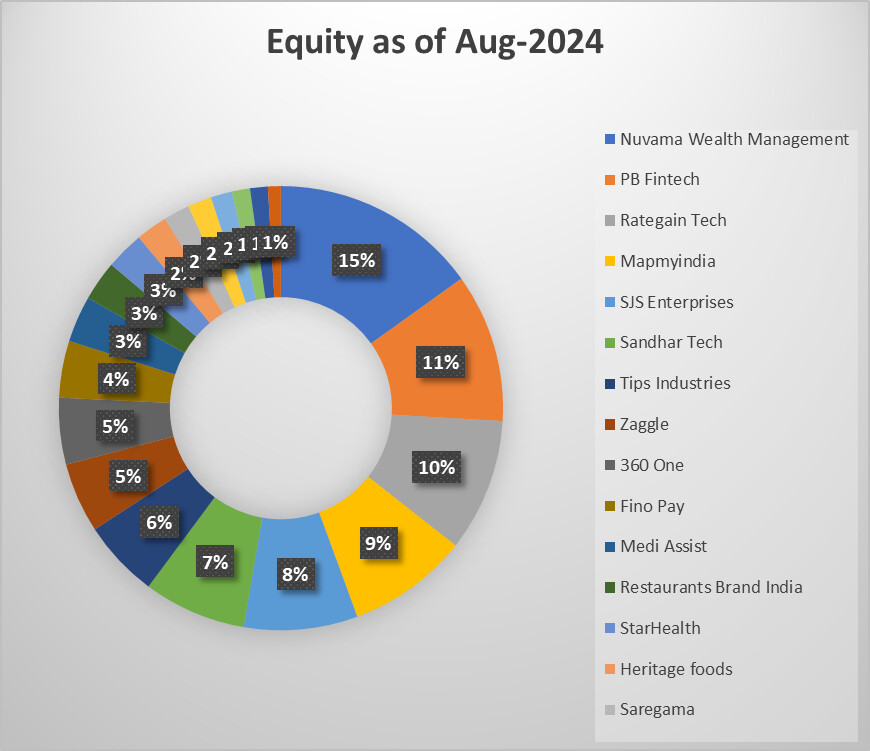

Stocks:

Before we get into my portfolio activity, let me acknowledge I felt very nervous about the heights. I am not able to ramp up the portfolio too much. However, if I look back, I ramp up my position only when price moves-up.

I evaluated each of my position on two conditions: 1. Look at each name to see if I will make investment today If I was buying the stock for the first time (its attractive or not). 2. Will I buy the stock if its down 20% or more.

Of the 20 positions, I have concluded to increase allocation on 13 positions. Some ramp up of allocations will be on dip, some on price increase (particulalry smaller positions). Only 6 had no change and only one trim (largely due to high allocation).

Having said that I am feeble and can change my view anytime.

Exits/Trims: Many R&D stocks, Sandhar (trim), and Ami Organics (exit), NAM-India (exit) PB Fintech (trim), MapmyIndia (trim). Rategain (trim), Saregama (trim)

Trimmed many stocks due to recent sharp run up. While Saregama was trimmed as results were not upto the mark.

Ami Organics exit: normalised extrapolation puts business at 30+PE (assuming 150 crore profit in FY25 which is almost double of their best in recent years) so I am not so comfortable. I might be under-estimating the operating leverage in the business though. A price dip or earnings surprise I look forward to change my view. I would rather tread cautious at such market levels and keep cash for any opportune time.

NAM-India exit: sharp run up. Profits in FY25 might be suppressed due to esop cost. Market turn may result in pressure on market related firms. Also managed overall allocation to market related firms given I have large exposure to Nuvama, and likelihood of further rampup in 360One.

New Entries/Ramp ups: SJS Enterprises (new), Fino Pay (new), Medi Assist (new), Zaggle (new), Heritage foods (new), Nuvama (Rampup), Star Health (rampup), Goldiam (new), EFC ltd. (new), Strides Pharma (new), Updater Services (new).

SJS: I have ramped up this significantly to 8% of my portfolio within a quarter. A high margin business (EBITDA -25%, some peers exhibit similar margin so not an exception), low value (content of SJS products in a vehicle is less than 1%) but high impact (marketing/looks, asethetics), active management (few past acquisitions have been super helpful to fill gap or prodcuts/tech), and low or no debt.

Medi Assist: A proxy to India’s health insurance (mainly group). Most of the peers are not able to make profits (good enough) but Medi Assis makes 21-24% margins. Grows at 15-18% topline and likely to grow earnings in 20-25% range due to margin improvement. Acquires companies ( making low margins) and bring them to its own margin level within a year time.

EFC: Strong growth guidance (almost 100% this year and may be 40-40% in coming years). Tailing Sage One and hoping corp gov is ok. Management acknolwedges business does not have any differentiation. So a scale and integration is key to acheive efficiency and efficiency may be the differentiator as they scale up. lets see.

Updater Services: Available at 20x OCF. Topline to grow in mid teens and bottomline may grow in 20-25% range. On PE basis also ~20 PE current year.

Highlights: 360 One and Nuvama continue to deliver solid results. So minor ramp up in Nuvama. I look forward to ramp up 360 one as results were astounding.

PB Fintech grew its premium at scorching rate of 78% YoY. However, recent stock run up makes me bit nervous. My target when I entered PB was 75k crore mcap in FY27. This has been reached has of last trade on 16th August. So this will be on trim mode.

Please note thate: I am wrong in 47% of my stock pickings so please do not follow me.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation . I work for a investment advisory firm. My portfolio is not a recommendation for anyone. Some of these stocks might be in clients portfolio as well so please be aware of vested interest.

Thank You for this tracker. Can this be a google sheet with anonymous access ?

I think you have created one tracker for PGEL as well. Super effort.

Most of the results/concalls are done. Can feel the volatility increasing in the market and wanted to concentrate my portfolio below 10 stocks. Exited, Concor, Titan, Intellect and carrying 15-20% cash.

Currently at 12 stocks, Next exit candidates – Zodiac, Titanin, phantom and raclgear (not fully sure on this one).

Entered Rategain – ~4% at 770, feel like have entered at sub-optimal levels, but looking to hold it for longer term and might add more at lower levels.

Short Thesis –

Studying Krishca, Jash, CNC companies, protean, aarti pharmalabs etc.