New stock Gujarat Toolroom Ltd. Anyone has any Idea why its quarterly profit zooms and promoters exited to null. It will be very helpful in understanding such companies. It may be a another fraud or another CG Power.

Posts in category Value Pickr

Rudra’s PF and Information attic (16-08-2024)

Hello Kapil,

You can basically leverage all the data that is present in the Data Sheet and build analysis/charts around those. Unfortunately the shareholding information is not added to that sheet and hence you can’t bring those data for further analysis in an automated manner.

Ayan’s Portfolio (16-08-2024)

Update

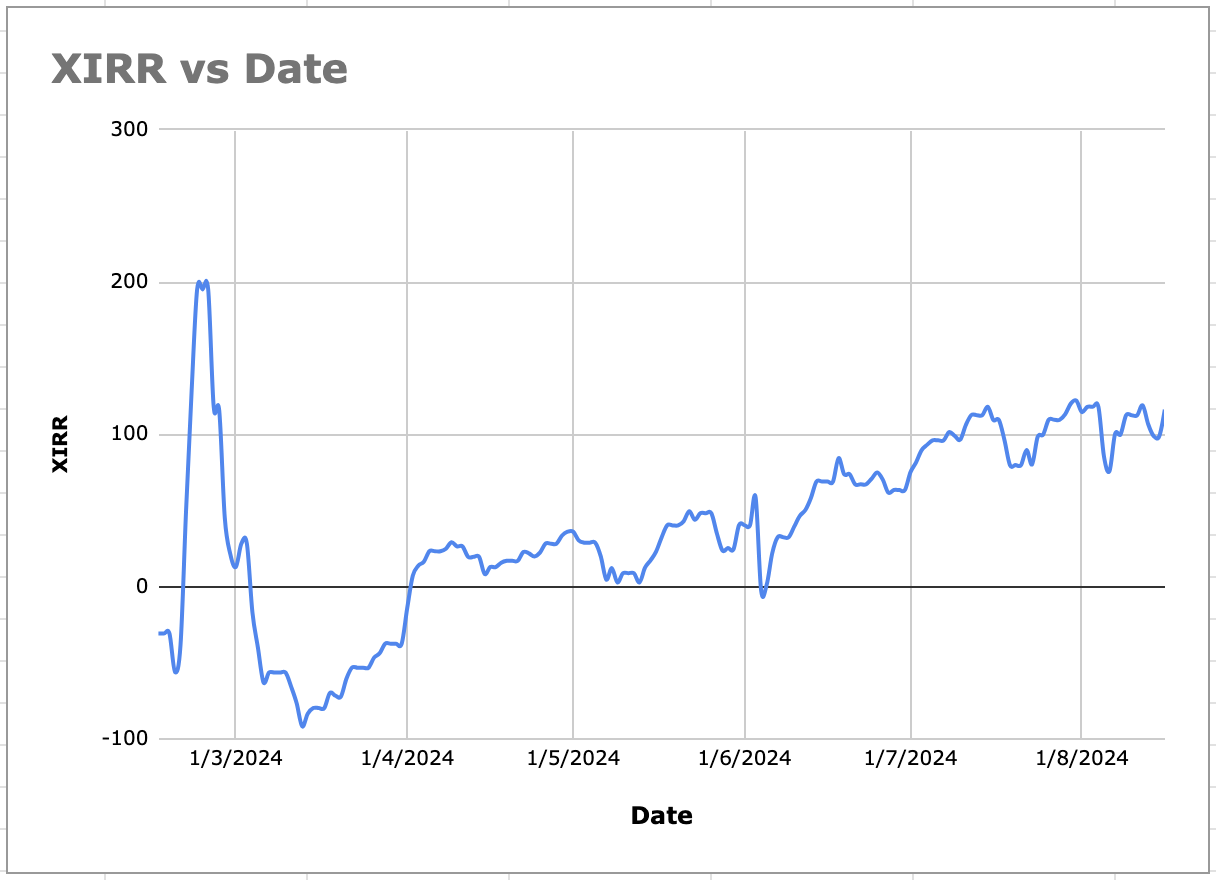

Today marks exactly 6 months into my investment journey. While at the time of starting this journey, I had set myself a target of an annual return of 30%, I am pleased to announce that at present I am running at 116.23% XIRR.

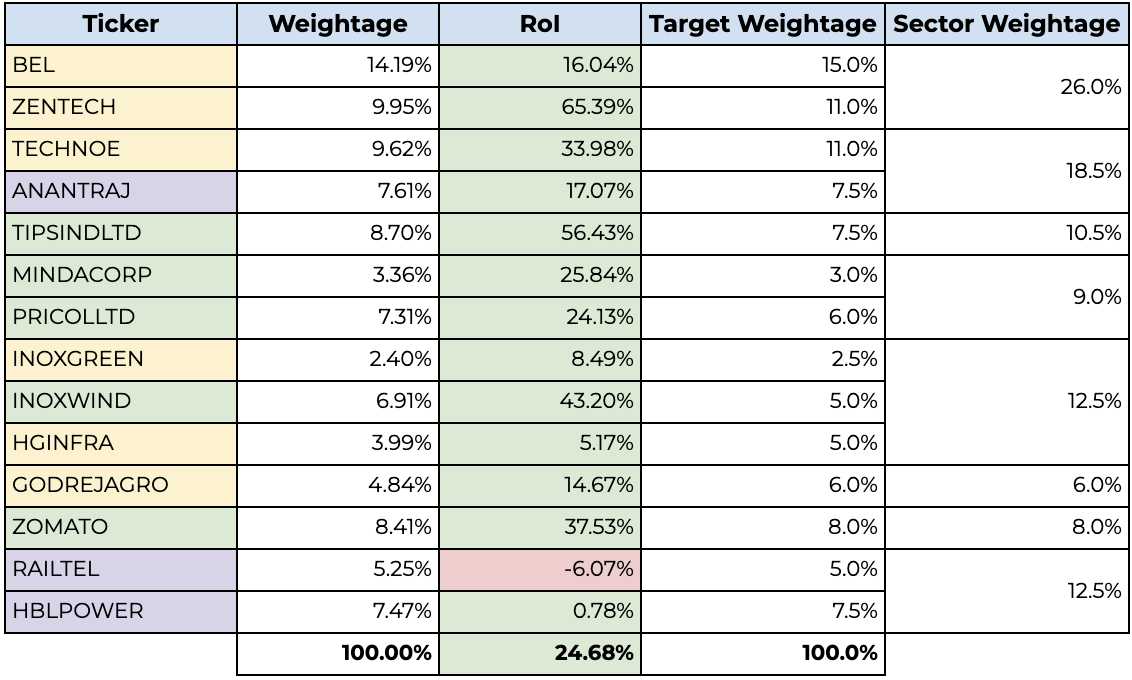

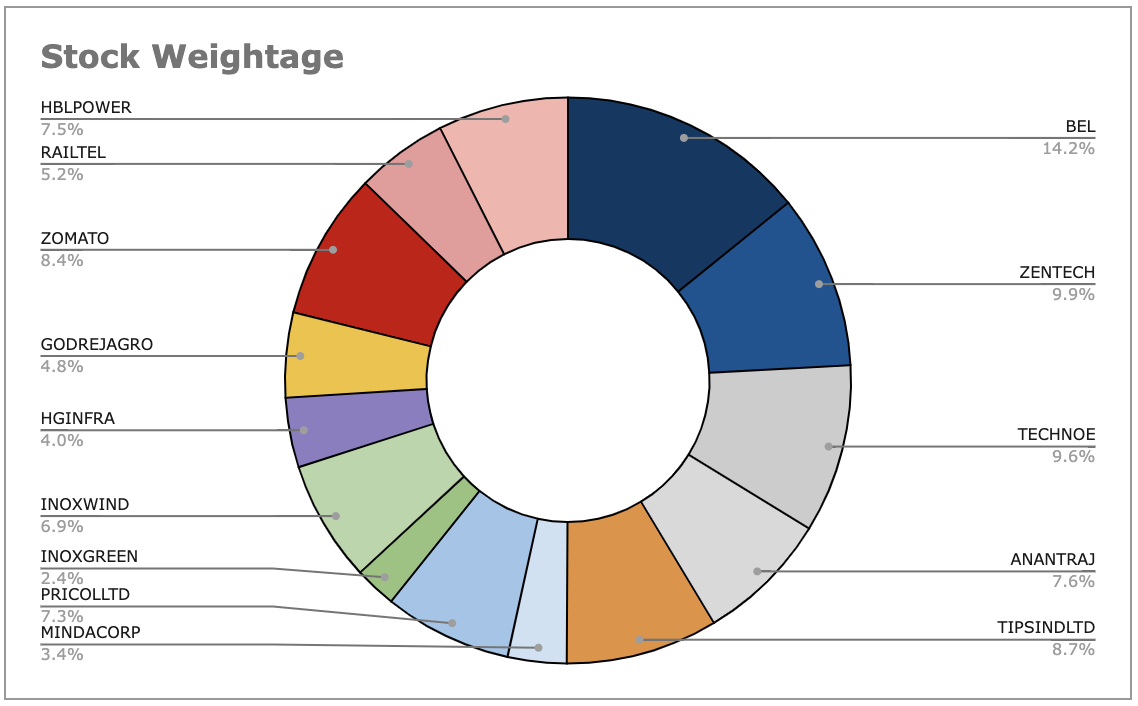

There have been some changes made to my portfolio as can be seen from its current snapshot.

As you can see, I have made the following main sectoral changes in my portfolio mix:

- Replaced hospital stocks with Data Centre stocks – while the aging Indian population multi decadal play is legit, I realised that the Data Center industry is likely to experience an explosive growth in the coming few years. I hence, loaded up on Techno Electric and Anant Raj (and to an extent, Railtel)

- Replaced hotels with railway stocks – hotel stocks seemed to have reached saturation and instead I chose to ride the railway (band)wagon

The stocks HBLPOWER (on KAVACH theme) and Railtel are yet to give me substantial results, but I’m prepared to hold them for the next 2-3 months at least.

The stocks HBLPOWER (on KAVACH theme) and Railtel are yet to give me substantial results, but I’m prepared to hold them for the next 2-3 months at least. - Lastly, I’ve reduced allocation in auto-ancillaries and exited JTL Industries in favour of retail consumption plays like Zomato and Godrej Agrovet (expected growth from its palm oil business) and renewables – Inox Wind and Green and HG Indra (solar entry).

I’ve also been maintaining a daily XIRR log, which seems to be forming a pattern after a significant amount of inputs. While I haven’t timed the market and have been investing a small amount every single day over the past six months, there seems to be certain trends and levels of resistance and support formed on the chart below. I might look to partially book profits and enter slightly heavier whenever the graph reaches the said points of resistance and support.

DHP India Ltd – Regulators and Fittings (16-08-2024)

Same here. This is the trouble with such small Cos.

Seamec Limited: formidable player in niche space; in a dull & boring sector (16-08-2024)

Thanks, it was an interesting read. So the demand seems to be more than the supply for atleast the next 3 years.

If anyone wants to read about the different types of OSVs:

DHP India Ltd – Regulators and Fittings (16-08-2024)

Never expected to see it crack this low. Although reduced my exposure significantly over last few quarters, never had the heart to let go the balance in the manic sell off last 2 sessions.

At 30% discount to its MF holdings, I really hope the fall stops here, however bad the performance and management may be.

S Chand- Transforming into a Complete Education content provider (16-08-2024)

- Q1 FY25 was a steady quarter despite national elections and heatwave impacting school operations

- Consolidated operating revenues were Rs 1,107 million, similar to Q1 last year

- Highest ever gross margins at 72% vs 69% last year

- EBITDA of Rs 84 million vs Rs 136 million last year

- Minor PAT loss of Rs 30 million vs Rs 11 million profit last year

- Lowest Q1 working capital metrics in company history – receivable days below 100 for first time

- Net cash position of Rs 882 million, up from Rs 600 million in Q4 FY24

- Engaged in content licensing partnerships with tech majors for Gen AI/LLM models

- Forging strategic partnerships in test preparation segment

- Focus on hybrid/blended learning model combining physical books and digital content

- Limited adoption of new NCERT curriculum by schools so far

- Expecting 40-50% adoption of new curriculum by schools this year if NCERT releases books on time

- Full adoption expected to take 2-3 years

- Expecting double-digit operating revenue growth in FY25

- Upgraded EBITDA margin guidance to 17-19% range

- Gross margins expected to be higher in FY25

- NCERT expected to release new syllabus books for more classes by end of 2024

- S Chand has books ready for all classes under new curriculum

- Timing of NCERT book releases crucial for adoption and revenue impact

- Full benefit of NCF expected to reflect in 2-3 years

- Focus on blended learning approach with digital supplements to physical books

- S Chand Academy, TestCoach and other digital platforms currently free, monetization expected in future

- New revenue stream from content licensing for AI models

- Maintaining strong cash position, not considering share buybacks currently

- May look at buybacks next year if cash reserves cross Rs 100 crore threshold

- Well-positioned to benefit from NCF implementation over next 2-3 years

- Focusing on blended learning and digital content alongside core publishing business

- Strong working capital management and cash position

- Confident of double-digit growth and margin expansion in FY25

Company/Equity Research using NSE/BSE website (16-08-2024)

how to differentiate between trading volumes and delivery using NSE/BSE data?

Blue Star ~ Leading player in RAC & Commercial Refrigeration (Market Leader) (16-08-2024)

India’s AC market is HOT! Blazing summers & rising incomes = AC gold rush. Overtaking China by 2045? Ambitious, but not impossible. This could be a game-changer for the industry.

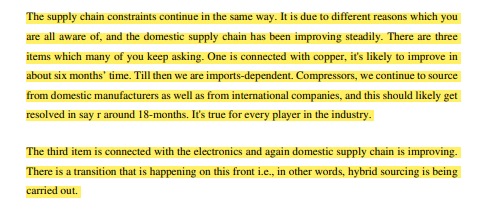

Supply chain woes continue to plague the AC industry. Copper & compressors are the main culprits. Domestic production is slowly improving but still heavily reliant on imports. Expect prices to stay high for a while.

New chillers for data centers & brine chillers mean they’re aiming for bigger fish in the market. Smart move to diversify & tap into growing sectors.