- Q1 FY25 revenue was Rs. 7,439 million, up 13% year-over-year

- EBITDA was Rs. 1,275 million with 17% margins

- Domestic and international businesses grew at healthy double digits

- Highest ever quarterly domestic revenues achieved

- Focus on expanding into non-auto, tech-agnostic and xEV segments

- Setting up special process facility for aerospace to enable higher value-added business

- Signed MoU to acquire 55 acres for future greenfield expansion

- Investing in automation for Swedish operations to improve profitability

- Strong growth in 2-wheeler segment driven by rural economy

- SUVs performing well in passenger vehicle segment

- Some softness seen in European passenger vehicles

- Slowdown in EV adoption rates in Western markets

- Targeting 20% overall revenue growth for FY25

- Expecting 30-35% growth in aerospace revenues

- Non-auto, tech-agnostic and xEV segments projected to grow 40-50% CAGR

- Commissioning new 4,000-ton press to expand product portfolio

- Exploring opportunities in chassis and suspension aluminum components

- Rs. 4,500 million CAPEX planned for FY25, mostly brownfield expansions

- Working towards 20% EBITDA margin target in medium term

- Swedish subsidiary margins expected to reach 11-12% by FY26

- Aluminum forging business margins improving but still below targets

- Some delays in aerospace orders from a key customer

- Logistics issues leading to higher international freight costs

- Potential slowdown in international business in second half of FY25

- Strong order book of Rs. 16.9 billion provides revenue visibility

- Growing opportunities in EV exports as OEMs face cost pressures

- Increasing content per vehicle in premium motorcycles

- New business wins in Swedish subsidiary to improve profitability

Posts in category Value Pickr

Sansera Engineering (16-08-2024)

Va Tech Wabag (16-08-2024)

- VA Tech Wabag is celebrating its centenary year, marking 100 years of presence in the water technology industry.

- Consolidated revenue grew 13% year-over-year to INR 627 crores

- Consolidated EBITDA increased 23% to INR 81 crores with 13% margin

- PAT grew 31% to INR 55 crores

- Order book stands at INR 11,000 crores

- Net cash position remains positive

- Focus on emerging markets like India, Middle East, Africa, Southeast Asia

- Divestment of Romanian subsidiary completed as part of strategy to reduce European exposure

- Targeting new areas like semiconductor, compressed biogas, green hydrogen, and digitization/AI

- Aiming to increase international revenue share to at least 50% of total

- Shift towards technologically challenging projects like desalination and water reuse

- Growing opportunities in One City One Operator projects in India and internationally

- Increasing focus on O&M business for better margins and cash flow visibility

- Indian government’s emphasis on water supply and treatment projects for 100 large cities

- Growing demand for desalination and wastewater treatment projects globally

- Targeting 15-20% annual revenue growth

- EBITDA margin guidance of 13-15%

- Entering semiconductor ultra-pure water, compressed biogas, and green hydrogen segments

- Exploring partnerships to enhance capabilities in new areas

- Aiming to more than double revenues within this decade at attractive margins

- Targeting order book of INR 15,000-16,000 crores for next year

- Asset-light approach

- No long-term debt on books

- Large project pipeline of INR 6,000 crores where company is preferred bidder

- Political/economic risks in some international markets mitigated through payment securities

Ami Organics – Pharma Intermediates & Specialty Chemicals (16-08-2024)

- Revenue grew 15% year-on-year to Rs. 176.7 crores in Q1 FY25

- Advanced Pharmaceutical Intermediates segment grew 16.6% to Rs. 135 crores

- Specialty Chemicals segment grew 10% to Rs. 42 crores

- Gross margin improved to 42.1% from 40% in Q4 FY24

- EBITDA margin declined to 16.7% from 22.1% in Q1 FY24

- Establishing Enchem AMI Organics as a subsidiary for electrolyte manufacturing

- Expanding electrolyte additives capacity to 2,000 metric tonnes

- Developing 8 new electrolyte additives beyond VC and FEC

- Expanding into Japan market after successful PMDA inspection

- Promoting new molecules from Baba Fine Chemicals to Korean and Japanese customers

- Ankleshwar plant expansion on track – remaining 2 blocks to be completed by Q2 FY25

- 16 MW solar power plant project initiated, expected completion by Q2 FY25

- Electrolyte additives capacity expansion on track for completion by end of FY25

- Targeting 25% revenue growth for FY25

- Aiming to reach 20%+ EBITDA margins by Q3/Q4 FY25

- Expecting asset turnover of 3-4x for Ankleshwar plant at full utilization

- Confident of meeting 25% growth guidance for FY25

- Expecting sequential growth in coming quarters

- Fermion contract to fully ramp up in FY26

- Peak sales for Apixaban and Rivaroxaban expected in FY26

- 15% YoY revenue growth despite industry challenges, driven by pharma segment

- Margins under pressure but expected to improve with higher utilization and better product mix

- New growth drivers like electrolytes, Japan expansion, and CDMO contracts in pipeline

Action construction equipment ltd (16-08-2024)

Finally the Defence order comes in. Order value is not given, but i suspect the rough terrain cranes might be around 6-8 cr and Special Forklifts might be around 60-70cr. Hope the company can share the order value and execution timeframe.

Seamec Limited: formidable player in niche space; in a dull & boring sector (16-08-2024)

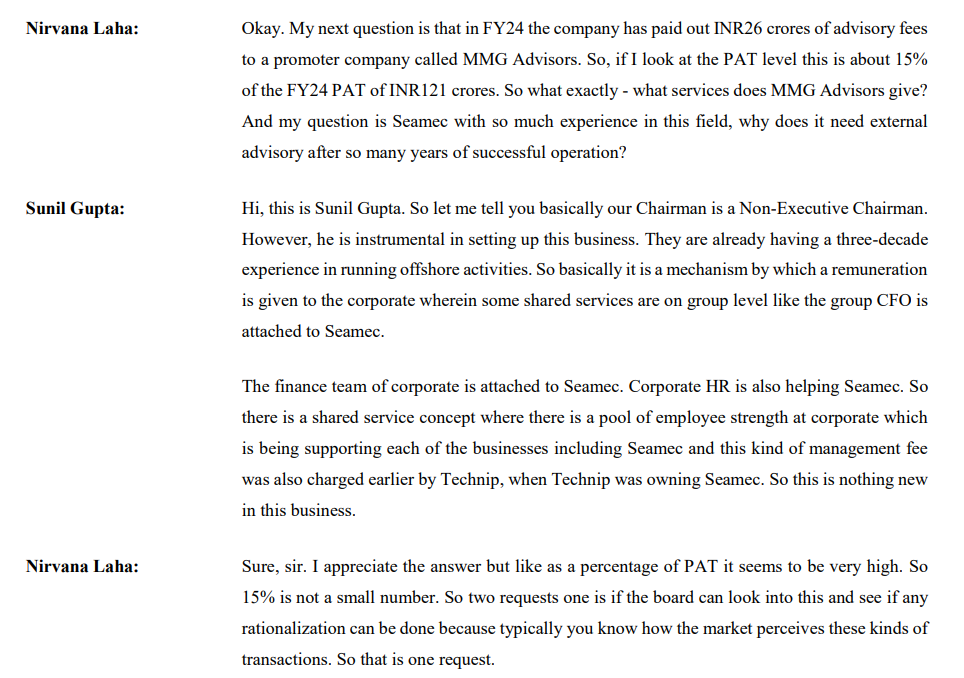

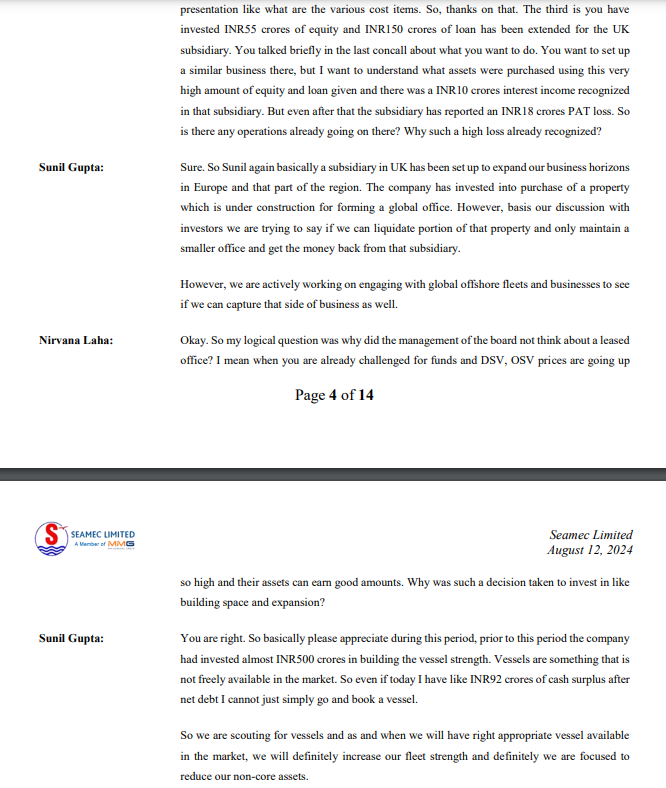

A couple of corporate governance issues to be aware of in Seamec

- Payment of hefty advisory fees to a related party company owned by Directors (Amounting to 4% of revenue or 10% of cash PAT whichever is lower). Management says this is a way of compensating corporate for shared services.

- Heavy investments in UK subsidiary, supposedly for setting up an office to tap into North Sea markets (55Cr via equity and 145Cr+ via loans). Management has said that in response to investor concerns they are seeing how to liquidate part of these investments and bring them back to the standalone entity.

A few other thoughts about Seamec

-

The OSV/DSV industry seems interestingly poised with no new supply of vessels expected in the next few years. Contract rates for these vessels should keep going up as and when contracts expire. This should result in operating leverage. An industry article which talks about the situation for OSVs – https://www.rivieramm.com/news-content-hub/news-content-hub/many-happy-returns-for-osv-owners-in-2024-and-beyond-79086

-

At the same time, buying a 2nd hand vessel from the market may not deliver desired ROCEs because 2nd hand vessels prices are also very high. Here, Seamec has an advantage, as its parent company HAL Offshore is going to transfer a couple of vessels to Seamec over the next few years. One DSV, NPP Nusantara, will get transferred to Seamec in Sep 2025 for a purchase price of INR 200Cr. At this purchase price and the prevailing charter rates, Seamec should be able to make good ROCEs.

-

3 of its existing DSVs are nearing end of life and will need replacement in the next couple of years. Remains to be seen how these get replaced. Any delays may impact revenues temporarily. Management has hinted that there is an outside chance for extension of life by Govt of India considering the criticality of these vessels and the prevailing market conditions.

-

While Seamec gets almost all of its revenues from ONGC, even ONGC is heavily dependent on Seamec and HAL Offshore for its DSV needs. So the dependency is mutual.

Disc: Not invested yet, tracking. Invested in another O&G ancillary play, Deep Industries.

SG Mart- Can it successfully create a marketplace? (16-08-2024)

Do they have a website? Or they take orders only on WhatsApp and their phones.

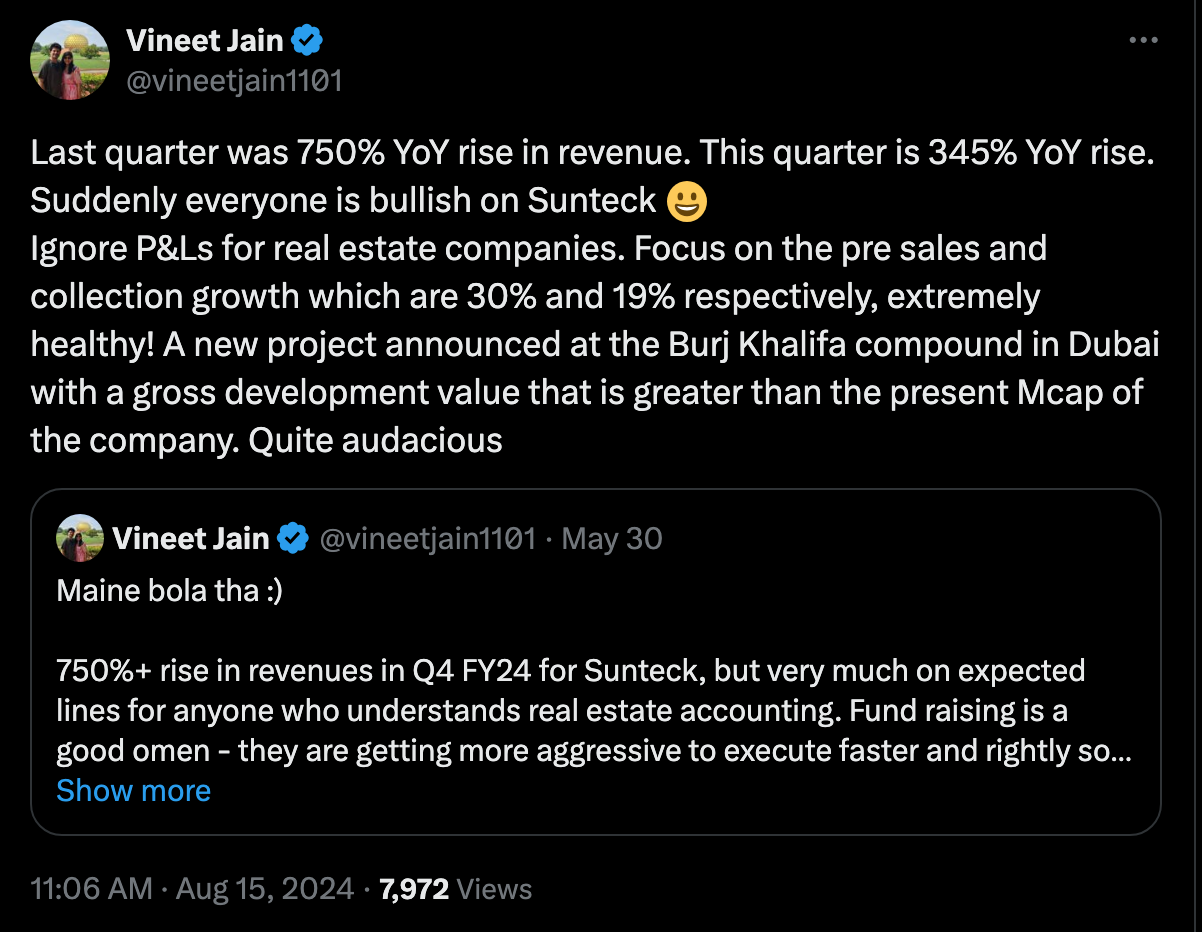

Sunteck Realty – Quality Real Estate Company (16-08-2024)

Sharing the latest results and investor presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/ab86bada-4eee-4812-b171-b357471ffd96.pdf

Also sharing a tweet by Vineet Jain

https://x.com/vineetjain1101/status/1823956832550879413

I am just tracking. No investment.

dr.vikas

IRM Energy – A new kid on the (listed CGD) block (16-08-2024)

@kalpesh4430 it wasnt removed. Even in quarter ending June 4.5 Cr was paid to the promoter(s)

Cambridge Technology Enterprises (16-08-2024)

One development in this company which could change the fortunes of the company. The development is in its USA subsidiary company – Cambridge Technology Financial Services Inc (CTFSI)

Have a look at its website for more information – https://www.ctfsi.com/

Background of team at CTFSI – https://www.ctfsi.com/about-us/#people

All the people from Goldman Sachs, Citi Bank, JP Morgan, MasterCard, Accenture, etc.

This linkedin post suggest that some new product is developed – CTFSI – Cambridge Technology Financial Services, Inc. on LinkedIn: #AIOperationalized | 10 comments

They have also hired Brett Adams (Has 17 years of experience at MasterCard)

As of now, the numbers in the P&L are not so attractive…

Want to understand their product more clearly, please connect with me for any discussion