That does make sense. But its a bit sad that management doesn’t put up any commentary on their new hospital’s progress.

Posts in category Value Pickr

Investing Basics – Feel free to ask the most basic questions (15-08-2024)

In some of the Analyst research reports refer Concall updates for the Quarter – where u can find commentary from CEO/CFO.

In screener.in, documents tab, Concall Quarterly notes u can find the same.

Refer below links for Company reports:

https://www.icicidirect.com/mailimages/Co_reports.htm

https://www.screener.in/company/IONEXCHANG/consolidated/#documents

Hope this helps.

Kilburn Engineering – Huge undervaluation (15-08-2024)

Thank you Kartik for the update. Business is doing well. There is a little upside/ no upside left as per my analysis. Currently trading at 27x forward PE.

Disclosure: Only Initiated the tracking position at lower levels. One of my misses despite business doing well.

Arman Financial Services Ltd (15-08-2024)

I see huge impairment losses this quarter, 43 Crores ! Because of this, even though revenues grew, margins took a hit and the net profit is down considerably as well. Can someone shed some light on how to read this? Is this a one time thing and we should focus on revenue growth or is there a potential for asset quality to deteriorate further? Thanks.

Unemployed investors portfolio (15-08-2024)

Added rel infra around 187

Increased position in shilpa medicare 530

Increased position in brand concept

Sold edelweiss,csl finance, barbeque nation

Waaree Renewables – old Sangam Advisors – can it keep on renewing? (15-08-2024)

Few of my takeaways from Q1 FY25 of Waaree Renewable Technologies

Waaree Renewable Technologies is riding high on India’s renewable energy wave, with a robust order book of 2,191 MW and successful execution of 217 MW in Q1 FY25. The company’s revenue soared by 83.31% year-on-year to INR 236.35 crores, reflecting strong momentum in the sector. With the government’s ambitious target of 500 GW grid-connected renewable capacity by 2030, Waaree seems well-positioned to capitalize on this growth trajectory.

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

The company is diversifying beyond solar EPC into areas like battery energy storage systems (BESS), pump storage, and hybrid projects. This strategic pivot aims to capture a larger slice of the evolving renewable energy pie. Waaree’s exclusive partnership with 5B Maverick for pre-fabricated solar solutions could be a game-changer, potentially accelerating project deployment timelines.

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

India’s renewable energy sector is witnessing a shift from pure-play solar to integrated solutions. The emergence of green hydrogen and the push for round-the-clock (RTC) power are reshaping the landscape. Waaree’s foray into these segments aligns well with these emerging trends.

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬:

Government support remains strong, with increased budget allocations and ambitious targets. The introduction of Approved List of Models and Manufacturers (ALMM) for solar modules provides a boost to domestic players. Rising corporate interest in captive renewable energy projects and the nascent green hydrogen sector offer additional growth avenues.

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬:

Module price volatility remains a concern, though Waaree claims to mitigate this through back-to-back contracts. Land acquisition delays and monsoon-related disruptions can impact project timelines. The sector’s heavy reliance on government policies and targets poses a potential risk if there’s a shift in priorities.

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

Questions were raised about the sustainability of high EBITDA margins (17% in Q1 FY25). Management maintained that 15% is a sustainable level, attributing fluctuations to project-specific factors. The company’s ability to maintain these margins in a competitive landscape will be crucial to watch.

𝐂𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐋𝐚𝐧𝐝𝐬𝐜𝐚𝐩𝐞:

Waaree claims to differentiate itself through better margins compared to peers (who reportedly operate at 9-9.5% margins). The management attributes this to their long-standing vendor relationships and selective project approach. However, as the sector grows more competitive, maintaining this edge could become challenging.

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

The management hinted at executing around 1.8 GW of projects in the next 9-12 months. The company’s bid pipeline stands at an impressive 15.5 GW, indicating strong future growth potential.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

Waaree operates an asset-light model, requiring minimal capex for growth. The focus seems to be on reinvesting cash flows to fuel growth rather than significant capital expenditures or shareholder returns.

𝐎𝐩𝐩𝐨𝐫𝐭𝐮𝐧𝐢𝐭𝐢𝐞𝐬 & 𝐑𝐢𝐬𝐤𝐬:

Opportunities lie in the expanding BESS market (estimated at INR 14 lakh crores by 2030) and emerging sectors like green hydrogen. Risks include potential policy shifts, intensifying competition, and execution challenges in new technology areas.

𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐂𝐥𝐢𝐦𝐚𝐭𝐞:

The regulatory landscape appears supportive, with policies like ALMM benefiting domestic players. However, the sector’s heavy dependence on government initiatives makes it vulnerable to policy changes.

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

There’s growing interest from both government entities (NTPC, SECI, SJVN) and private players in outsourcing EPC work, benefiting companies like Waaree. The trend towards integrated renewable solutions is driving demand for comprehensive service providers.

Disclaimer: This is a general analysis and does not constitute financial advice.

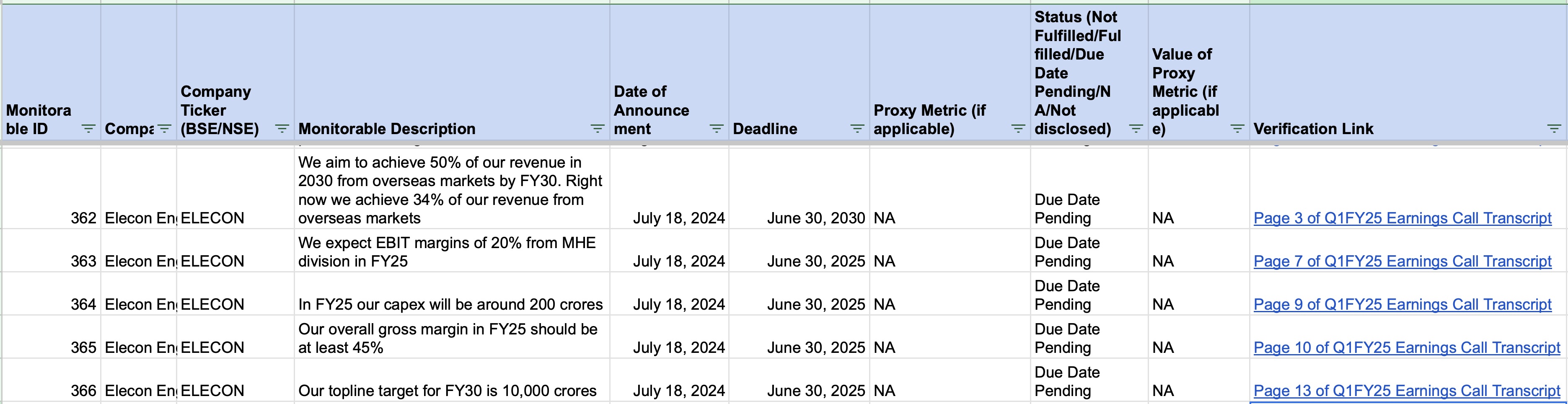

Elecon Engineering Limited (15-08-2024)

In the below tracker, I have started tracking important company goals for ELECON. These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

- Company Ticker: For identifying the company

- Monitorable Description: Description of the goal or metric being tracked

- Date of Announcement: When the monitorable was announced

- Deadline: Target date for achieving the monitorable

- Status: Current progress (e.g., Not Fulfilled, Pending)

- Verification Link: A link to see where I got the information about the goal.

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables-20.xlsx (141.2 KB)

Post Script: DM if you want me to track the monitorables for any specific company.

Screener.in: The destination for Intelligent Screening & Reporting in India (15-08-2024)

Hi Kowshick,

As I pointed out in my post, the data is already there based on which the charts are populated. Here I was looking for a way that the data is accessible to us in the screener.

Apeejay Surendra Park Hotels – Potential Value Unlocking (15-08-2024)

Park Hotels India is engaged in the hospitality business operating under the brand names of “THE PARK “, “THE PARK Collection “, “Zone by The Park “, “Zone Connect by The Park ” and “Stop by Zone “. The company also owns the iconic brand Flury’s which is present in 82 outlets pan India.

Presence: The company currently operates 27 hotels, which are spread across different categories such as luxury boutique, upscale, and upper midscale. These hotels are present in various cities in India including Kolkata, New Delhi, Chennai, Hyderabad, Bangalore, Mumbai, Coimbatore, Indore, Goa, Jaipur, Jodhpur, Jammu, Navi Mumbai, Visakhapatnam, Port Blair, and Pathankot, offering a total of 2,395 keys as of Mar 31, 2024. The company has 6 hotels scheduled for launch in the next 12 months, with a total of 228 keys. The Kolkata project alone is expected to generate around Rs. 100 crore

of cash annually for the next three years, starting FY 2025-26.

The promoters of the Company are Karan Paul, Priya Paul and Group companies. The company raised Rs 920 crore via an IPO in Feb 2024, out of which Rs 550 crore has been utilized to repay the entire outstanding debt of the company

Key Financials

| Mar-22 | Mar-23 | Mar-24 | Mar-25E | |

|---|---|---|---|---|

| Sales | 255 | 506 | 579 | 598 |

| Operating Profit | 46 | 159 | 192 | 235 |

| OPM % | 18% | 31% | 33% | 39% |

| Other Income | 12 | 18 | 13 | 15 |

| Interest | 60 | 62 | 66 | 14 |

| Depreciation | 40 | 49 | 51 | 61 |

| Profit before tax | -42 | 65 | 89 | 175 |

| Tax % | -33% | 27% | 22% | 35% |

| Net Profit | -28 | 48 | 69 | 114 |

| EPS in Rs | -1.61 | 2.75 | 3.22 | 6.50 |

| Net Worth | 508 | 555 | 1198 | 1312 |

| Total Debt | 654 | 617 | 100 | 125 |

Key Strengths of the company:

Highest Occupancy Rate in Industry: The company has one of the highest occupancy rates in India with ~90% occupancy across all its major hotels.

Growth in F&B income: The share of F&B income in ASPHL’s revenues has historically been high (43% in FY2024) compared to its peers. Addition of Flury’s brand where the company is looking to aggressively expand number of outlets will further support the 10% historical growth in this segment

Deleveraged balance sheet: Its net worth improved to Rs. 1,198.0 crore as on March 31, 2024 from Rs. Rs. 555.7 crore as on March 31, 2023, and the gearing reduced to 0.1 times as on March 31, 2024 from 1.1 times as on March 31, 2023. Company is currently net cash and has unutilized funds of ~Rs 12 crore from the IPO.

Key Weaknesses:

**Expansion plan:**The company has planned greenfield hotel projects, on its existing owned land, in Kolkata (EM Bypass) and Pune. which will have 250 and 200 rooms, respectively. While the Kolkata project is to be entirely funded from the proceeds of real estate monetisation, the cost of the Pune project will also be ~Rs. 200 crore. Since the company is already operating at 90%+ occupancy at its existing hotels, further revenue growth in the hotel segment would be contingent on project execution of these two projects

Cyclical Industry: The operating performance of hotels remains vulnerable to seasonality, general economic cycles and exogenous factors, the company will need to continue investments in renovation and

refurbishment of hotels to ensure delivery of high quality of service.

Key Operational Metrics

| Q4 FY23 | Q3 FY24 | Q4 FY24 | FY24 | |

|---|---|---|---|---|

| RevPAR | 6414 | 6562 | 6847 | 6170 |

| Occupancy | 93.20% | 90.10% | 91.70% | 92.10% |

| ARR | 6884 | 7286 | 7463 | 6699 |

Valuation: The company is trading at 34x 1Y fwd P/E which is at a discount to existing players. Company has appreciated 15% from the IPO price but still has a good runway for growth, and is now significantly deleveraged, which will help support expansion plans. EV/EBITDA is also reasonable at 16x.

Disclosure: Invested.

Links

https://www.bseindia.com/xml-data/corpfiling/AttachHis/ea3a792e-c58c-4f30-bef8-1e284b0ad9c8.pdf

Genesys International – Product Monetisation (15-08-2024)

GENESYS INT.pdf (1.2 MB)

RESULTS Q1FY25