Q1 result is on the expected lines. The question is how long it will take to sell the hotel?

Posts in category Value Pickr

Sarda energy and minerals ltd (14-08-2024)

NCLT gives nod to Sarda Energy’s acquisition of SKS Power for Rs 2,200 cr

Nava Bharat Ventures : Turnaround story (14-08-2024)

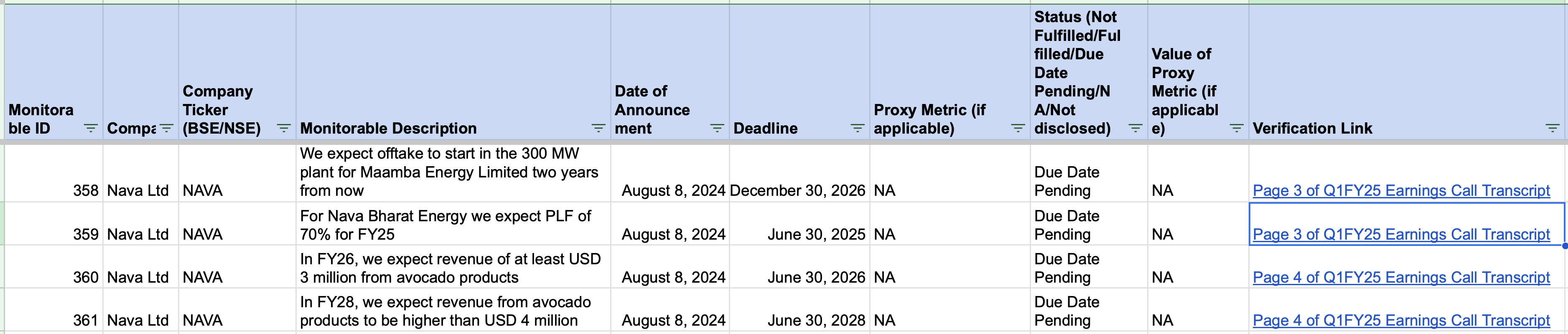

In the below tracker, I have started tracking important company goals for NAVA. These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

- Company Ticker: For identifying the company

- Monitorable Description: Description of the goal or metric being tracked

- Date of Announcement: When the monitorable was announced

- Deadline: Target date for achieving the monitorable

- Status: Current progress (e.g., Not Fulfilled, Pending)

- Verification Link: A link to see where I got the information about the goal.

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables-18.xlsx (143.2 KB)

Post Script: DM if you want me to track the monitorables for any specific company.

DHP India Ltd – Regulators and Fittings (14-08-2024)

Any updates from AGM ?

The company continues to struggle and there is no qualitative commentary available in the quarterly financial statements. There is a decent amount of unrealized gain for the investments parts which is in line with the markets. However, the operational performance continues to remain sluggish and worrying.

Triveni Turbines Ltd – High Quality Engineering Play? (14-08-2024)

Few of my takeaways from Q1 FY25 of Triveni Turbine

Triveni Turbine Limited (TTL) appears poised for continued growth, driven by robust demand across geographies and segments. The company reported a stellar Q1 FY25 with 23% revenue growth and 32% PAT growth year-over-year. Order inflows surged 40% to reach a record ₹6.36 billion, providing strong visibility for future quarters. With exports now contributing 66% of order inflows, TTL is successfully expanding its global footprint.

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

TTL is pursuing several key initiatives to drive future growth:

- Expanding product range to higher megawatt turbines (up to 120 MW) to address larger industrial markets

- Strengthening presence in the API turbine segment for oil & gas applications

- Growing aftermarket and refurbishment business, especially in international markets

- Setting up US subsidiary to tap local opportunities

- Continued focus on R&D and new technology development

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

- Shift towards renewable energy and waste-to-energy projects globally

- Growing demand for energy efficiency solutions in industrial applications

- Increasing aftermarket potential as installed base expands

- Geographical diversification of revenue streams

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬:

- Global push for energy transition and decarbonization

- Revival in industrial capex, especially in sectors like steel, cement, etc.

- Government initiatives like Inflation Reduction Act in US boosting clean energy investments

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬:

- Macroeconomic uncertainties in some export markets

- Volatility in commodity prices impacting customer decisions

- Intensifying competition in the API turbine segment

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

Analysts expressed concerns about sustainability of margins and domestic market slowdown. Management assured that margins are not a concern given higher export mix and aftermarket contribution. On domestic slowdown, they expect a revival in coming quarters as enquiries have picked up recently.

𝐂𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐋𝐚𝐧𝐝𝐬𝐜𝐚𝐩𝐞:

TTL faces competition from global majors in exports markets. However, its technological capabilities, cost competitiveness and localization strategies are helping gain market share. In the domestic market, TTL remains one of the leading players.

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

No specific guidance was provided, but the management expressed confidence in delivering strong growth in FY25, both in order inflows and revenues. Margins are expected to remain healthy, aided by favorable product mix.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

TTL plans to maintain its asset-light model while increasing investments in R&D, people and customer-facing initiatives. The company aims to remain free cash flow positive and maintain its dividend payout policy.

𝐎𝐩𝐩𝐨𝐫𝐭𝐮𝐧𝐢𝐭𝐢𝐞𝐬 & 𝐑𝐢𝐬𝐤𝐬:

Key opportunities include expanding addressable market through new product development, growing aftermarket business and geographical expansion. Risks include macroeconomic uncertainties, increased competition and potential technology disruptions.

𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐂𝐥𝐢𝐦𝐚𝐭𝐞:

Favorable policy push towards clean energy and industrial decarbonization across geographies is creating opportunities for TTL’s solutions.

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

Customers are increasingly focused on energy efficiency and clean energy solutions. TTL is well-positioned to cater to these evolving needs with its broad product portfolio and technological capabilities.

Disclaimer: This is a general analysis and does not constitute financial advice.

EPL – Essential Packaging Company (14-08-2024)

Regarding opting for same pricing in sustainable

recycling tubes, this is what the company had said in q4fy24 concall, I am paraphrasing here:

‘Pricing for sustainable tubes is pretty much the same as normal tubes, this is a strategic decision so that the shift to sustainable tubes isn’t slowed due to someone else offering normal tubes at lower prices. Also, they don’t want to loose wallet share because of this.’

They try to price it higher wherever possible, so doesn’t seems to have any pricing power yet.

With too many geographies there are many moving parts and probability of some thing going wrong is higher. Mgmt guidance is for double digit revenue growth with 20% ebitda margin.

Disc: Invested with zero returns in this for past 3 years.

Singer – Possible turnaround a.k.a. Symphony (14-08-2024)

This is a head-scratching disclosure. At an investment of only Rs, 15 lacs, production capacity will be increased from 90,000 units to 6,30,000. Anyone with insights into the sewing machine markets please share your thoughts.

3B Blackbio DX Ltd (14-08-2024)

PLEASE share the whole pdf of Nuvama coverage.

I think they cover many small caps in that cover. It will be very interesting to study other worthy small caps.

PLEASE

Ceigall India Limited (14-08-2024)

Company has just received an additional order approx 1000 crore from Kanpur Central Bus Terminal and the Bhubaneswar Metro project.

Please update any red flag against the company or promotors.

Ceigall India Limited (14-08-2024)

Founded in 2002, Ceigall India Limited is an infrastructure construction company with expertise in specialized structural projects, including elevated roads, flyovers, bridges, railway overpasses, tunnels, highways, expressways, and runways.[1]

Key Points [ edit ]

Business Profile [1] Ceigall has expertise in constructing state and national highways, specialized structures such as elevated corridors, bridges, flyovers, and rail over-bridges, along with maintenance of highways

Business Model [1] Their operations comprise EPC and HAM projects across 10 Indian states. It also handles independent and contractual O&M projects and subcontracts. In FY24, revenue was 66.05% from EPC, 26.34% from HAM, and 0.32% from O&M.[2]

Project Details [3] The company has completed over 34 projects, including 16 EPC, 1 HAM, 5 O&M, and 12 Item Rate projects in the roads and highways sector. Currently, it has 18 ongoing projects, comprising 13 EPC and 5 HAM projects.

Rapid Growth & Transition [1] They have grown at a CAGR of 50.13% between FY21 and FY24. Over the last two decades, the company has transitioned from a small construction firm to an established EPC player, showcasing expertise in the design and construction of various road and highway projects, including specialized structures.

Enhanced Bidding Capabilities [3] The company is eligible to bid for single NHAI EPC projects up to Rs 5,700 crore and single NHAI HAM projects up to Rs 5,500 crore. Additionally, it is empaneled with the Delhi Metro Rail Corporation Limited for upcoming tenders.

Clientelle [4] Since its inception, Ceigall has executed numerous projects with the Public Works Department (PWD) in Punjab, the National Highways Authority of India, and the Ministry of Road Transport and Highways (MoRTH) through tenders. Other notable public sector clients include IRCON, Military Engineer Services (MES), and Bihar State Road Development Corporation Limited (BSRDCL).

Geographical Revenue Bifurcation [5]

- Punjab: 51%

- Jammu and Kashmir: 14%

- Haryana: 9%

- Himachal Pradesh: 1%

- Maharashtra: 1%

- Bihar: 1%

- Uttar Pradesh: 23%

Strong Order Book [6] Their order backlog stood at Rs 9470.84 crore as of June 30, 2024. This is 3.13 times the FY2024 revenue. As of June 30, 2024, projects awarded by NHAI contributed 80.31% to the Order Book