You are right. No stop loss in this strategy. In my case cochin is down by 16%. But you can twist the strategy for urself, if you are not ok with big drawdowns, like you may keep 15% or 20% as a threshold till you can take pain and then get out of that stock. I am rhinking of 15% stop loss after initial purchase , so may be selling cochin.

Posts in category Value Pickr

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (13-08-2024)

Good things – Debt has come down by 172cr to 130 cr, Left with approximately INR 130 crores from Axis Finance Limited at the rate of 10.75% and as per mgmt will result in significant reduction in finance costs from ensuing quarters. I am expecting 4 cr int cost and 5 cr depreciation going forward.

Another positive news from this results, All pledged shares of promoter group would also be released with immediate effect. Hence forth investors dont see threating message while buying Kamat.

Negatives- Yes dilution to an extent of 5%, glad this is limited to 5% which happen in most cases where promoters see huge value. Even if the value is there in acquired companies, that will be loss for minority share holders as we dont see any value in the next 3 yrs. By this promoters kept their holdings intact as theirs will be diluted to pref allotment. Hope they buy another 5% by yr end and allow share rerating.

We can expect good results in q3 and q4 and q1fy26 and I think those results only help the stock in rerating. For now just accumulate if it falls below 200.

Next FY probably we can expect 30 EPS considering 3.3 cr equity shares.

Aptus Value Housing : Is valuation justified or just another HFC? (13-08-2024)

Few of my takeaways from Q1 FY25 of Aptus Value Housing Finance

𝐂𝐨𝐫𝐩𝐨𝐫𝐚𝐭𝐞 𝐓𝐫𝐚𝐣𝐞𝐜𝐭𝐨𝐫𝐲:

Aptus Value Housing Finance demonstrated strong performance in Q1 FY25, with 27% YoY AUM growth to Rs. 9,072 crores and 21% PAT growth to Rs. 172 crores. The company maintains a positive outlook on growth opportunities in Tier 2-4 cities, driven by low mortgage penetration and significant housing shortage. Management expressed confidence in achieving their 30% disbursement growth guidance for FY25.

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

- Geographic expansion: Opening 40 new branches in FY25, including in new states like Maharashtra and Odisha.

- Technology adoption: Implemented a mobile-first lead management system to improve efficiency and productivity.

- Digital channels: Increased focus on customer referral app, construction ecosystem app, and social media channels for lead generation.

- Productivity enhancement: Rationalization of collection team and focus on improving per-employee productivity.

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

- Increasing penetration in existing geographies

- Contiguous expansion into new states

- Focus on digital channels for lead generation

- Emphasis on productivity and cost efficiency

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬:

- Low mortgage penetration in Tier 2-4 cities

- Significant housing shortage in target markets

- Government initiatives supporting affordable housing sector

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬:

- Potential cyclicality in affordable housing segment

- Rising interest rates impacting borrowing costs

- Competition from other players in the affordable housing finance space

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

-

Concern: Slowdown in Tamil Nadu growth

Response: Management acknowledged issues but expects 20% growth in FY25 with corrective measures in place -

Concern: Rising 30+ DPD

Response: Attributed to seasonality and elections; expect improvement in coming quarters -

Concern: NIM compression

Response: Expect 10-15 bps NIM compression due to rising borrowing costs

𝐂𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐋𝐚𝐧𝐝𝐬𝐜𝐚𝐩𝐞:

Aptus faces competition from other affordable housing finance companies and small finance banks targeting similar customer segments in Tier 2-4 cities.

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

- 30% overall disbursement growth for FY25

- 20% disbursement growth in Tamil Nadu

- Credit cost guidance of 0.3-0.35% for FY25

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

The company maintains a strong capital position with a net worth of Rs. 3,800 crores. No specific capital raising plans were discussed, indicating sufficient capital for near-term growth.

𝐎𝐩𝐩𝐨𝐫𝐭𝐮𝐧𝐢𝐭𝐢𝐞𝐬 & 𝐑𝐢𝐬𝐤𝐬:

Opportunities:

- Large addressable market in underserved segments

- Expansion into new geographies

- Leveraging technology for improved efficiency

Risks:

- Potential asset quality deterioration in economic downturn

- Increased competition in affordable housing finance

- Regulatory changes impacting business model

𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐂𝐥𝐢𝐦𝐚𝐭𝐞:

The company benefits from priority sector classification for housing finance. Management mentioned adapting to recent RBI circulars on disbursement practices.

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

The management indicated strong on-ground demand for both home loans and small business loans in their target markets.

Smallcap momentum portfolio (13-08-2024)

@vamsi00797 You are right. There is no stop loss concept and the stock will remain till it falls below the 25th rank.

GRSE is down 13% for me!

Markel Corporation – a case study to value insurance companies (13-08-2024)

MKL – Markel – August 1st 2024:

We are betting more on the jokey than we are on the business. We are extremely biased with the calibre of the management because we adore and admire Thomas Gayner. We may be as blindsided with Thomas Gaynor as we were with Frans Van Houten (Philips NV). We might know what the business does but we really do not understand the insurance industry. Both of us have a slightly different method of valuing the business- neither of which is in detail. We have merely done a conservative (according to us) yet general back of the envelope valuation and made the 1st position in this stock at $1550.

What we still have to figure out and agree upon is – when should we sell the stock? How do we know that we were wrong in our thesis?

As of the writing,

- the business has a manageable debt of approximately $3.8 billion versus a net profit of about $2 billion per year

- Officers and directors own approximately 1.71% of the common stock

- Thomas Gaynor personally purchased shares from the open market in the beginning of 2024 (he agreed at a conference that he found the shares to be undervalued at the at the price he purchased – estimate that to be approximately $1300)

- has a record of taking more reserves than are really needed

- pension assets are greater than pension obligations

- has reduced outstanding shares from 13.99 million in 2013 to 13.13 million in 2023

- no dividends are being declared

- Buffett had a general rule of paying 1.2 times of book value for Berkshire stock to be repurchased.

The following are the risks that we identified:

a) The insurance side of business (Depending on the type of insurance they underwrite) does not have past the data to price the risk and this could be a possible detractor to future performance in the form of huge insurance payouts. (writing insurance they shouldn’t write and an epidemic/CNBC type event)

b) Human Nature: The insurance executives try to show growth in written premiums by sacrificing the quality of underwriting.

c) Accounting risk (two parts): Firstly Thomas Gayner has said that Markel (and he) has more conservative estimates of the reserves than are needed, but on the flip side, buys/acquires subsidiaries for Markel ventures by using the EBIT and EBITA multiple concepts. Secondly, Markel (and Thomas Gayner) value Markel ventures by the amount of EBIT and EBITDA they generate – this is contradictory to how WEB valued his operating subsidiaries.

d) ILS (Insurance Linked Securities): This is something new that they have introduced to contain risk. They are the first players in this game and therefore any new hot buzzword is always a red flag. This were the 4 risks identified on the operating side of businesses (as of August 1st 2024).

e) The market venture side of the business faces the risk just in the same way as private equity because there exists the risks of overpaying (paying too much for too little value in return i.e ISCAR type of deal with WEB) and secondly the risk of being blindsided by them wanting to close the deal (this however might be in check for as long as Thomas Gayner is at helm but you never know for sure).

Valuation of HH:

HH has gone for something that he calls asset-based earnings valuation. He assumes that Markel will earn approximately 7 percent (net) on assets of approximately $24 billion (current market value of the stocks plus bond portfolio). This translates to a net profit of approximately 1618M dollars. Applying a PE multiple of 11 implies a market cap of approximately $18.4 billion. This implies a current value of approximately $1421.00 per share at about 13 million outstanding shares. Ten years out applying the rule of 72 implies that the net profit would be approximately 3360M. Again applying a PE multiple of 11 implies market cap of approximately $36.9 billion. Assuming if outstanding shares remain constant at 13 million the per share value could be $2843. Value line predicts outstanding shares to be 8M by 2027-29 period. I personally find this to be very optimistic but it’s possible only if we experience a period of depressed values from the current overpriced valuations of the entire market in August 2024. By looking at the previous 10 years I expect the outstanding shares to be approximately 12 million which would imply a per share value of $3075 dollars. HH Has made a note of holding the stocks for as long as the bonds plus stocks portfolio are growing. He notes that MKL will not grow the portfolio but rather provide some stability.

Valuation of MH:

Markel initially came on our radar during Q2 2023 when Tom Russo added Markel to his portfolio. My remark at the time was “We got to buy it at about 16B Mcap implies a price of 1200 USD per share.” I cannot recall how that valuation was done. Markel was also added to two other portfolios during Q3 and Q4 2024 as well. However there are no comments for that. It once again came on the radar in Q1 2024 and my valuation at the time was as follows: has total debt of about 3.8 billion and a net debt of about 0.2 million. PE multiples have been around 20X+ but has come down since interest rates went up to 13-7-10-8x. Revenues grew from 4.3 billion to 16.6 billion in 10 years whereas operating margins ranged from 12-3-13-18% (current). Interest expense is approximately 180 million. And there is some preferred dividends an minority interest being given out. PAT margins at 6-10-18-8-12% (current). OS from 12.59 to 13.3M over the last 10 years. I came up with the future market cap of 13.2-19.8-23.4-26.4B (I can’t say if this was a 5/10 year valuation and neither can I remember how I got this numbers. The above valuation was done in Q1 2024).

Five years out I assume revenues to be in the range of 20-21-22 billion. I assume profit margins of 6% to 9% to 12%. Applying AP multiple of 8X, 10X and 13X implies a market cap of 9.6 billion, 18.9 billion and 34 billion. Average market cap comes to about $20.8 billion ($1600 per share 5 yrs out). Applying a at 20% margin of safety in this case, results in a market cap of $16.64 billion ($1280 per share). This valuation (revenues and profit margins) includes (a) interest and dividend income and (b) gain or loss on sale of investments. These numbers however do not include the per share value of the stock and bond portfolio at its current market value of approximately $24 billion.

This however should not be seen as a stand alone asset on a per share basis because this is recorded as a part of assets on the balance sheet with liabilities on the other side of the balance sheet. Total assets – total liabilities = common equity; which might be a reliable substitute but it doesn’t make much sense in an insurance operation or the one that Markel has. This is how I would value the stocks and bond portfolio: I assume a market decline of about 30% and as a result an equal draw down on the market value of the stock and bond portfolio from 24B to 16.8B. In addition, I assume that reserves of 24 billion are off by 50% and therefore would require an additional $12 billion (which is to come out of the depressed stock and bond portfolio). This equates to 16.8B – 12B = 4.8B (This is what is left for equity holders, if Markel has had a disastrous year and survives, if it doesn’t, then all bets are off!). This implies a 4.8B/13M shares $369 per share of value. Adding this to the original $1600 avg value 5 years out, gives 1600+369 = $1969 value (on our conservative basis). On a best case basis, this would be 34000M/13M = 2615 +369 = $2984 value (Our best case. This could be higher because we have assumed a worst case for the $369 stock + bond portfolio value). On a worst case basis, this would be 9600M/13M = $738 + $369 = $1107 value per share. This concludes to $1107 on the downside, $1969 on a base case and $2984 on a best case basis. From the current price of $1550, this implies a downside of -$443 vs an upside of +$1434 (a 3.2x upside versus the downside).

Smallcap momentum portfolio (13-08-2024)

Hello Sir @visuarchie – trust you are doing good.

i am sure you may have answered this earlier but just wanted to make sure nothing changed – basically, if a stock keeps going down after we added we’ll not exit it until it falls out of top 25 as there is no stoploss concept here – is this correct understanding/applicable even now? the reason i ask is cochin shipyard and GRSE seem to keep falling almost since i started the pf around last month but they still need to be in the pf owing to their ranking (obviously high ranking given the runup they had in the past 6 months)

Deep Industries (DIL) (13-08-2024)

DEEP Q1FY25:

• Order book for Deep Industries – INR 1246 crores, reflecting a 12% year-over-year growth. Company is witnessing highest ever bidding pipeline which could further enhance the order book going forward.

• Industry news: The winners of the ninth round of Centre’s Open acreage licensing policy (OALP) are likely to be announced in next couple of months. There have been news reports that to accelerate the exploration and production, the government is also planning to announce 10th round of OALP. Both these rounds put together would bring in around 50 blocks under exploration, thereby providing immense opportunities for the Company for oil and gas support services.

As you all might be aware, prior to OALP under hydrocarbon exploration and licensing policy (HELP), separate rounds of new exploration and licensing policy (NELP), Coal – Bed Methane (CBM) and Discovered Small Fields (DSF) were also held by Government. Under NELP, 32 blocks out of total 254 blocks awarded are operational. Additionally, 33 CBM blocks and 2 DSF blocks recently announced are also potential opportunities for the Company.

• Dolphin offshore:

o PRABHA BARGE: The update on Barge asset Prabha is that the refurbishment is now in the final stage of completion and we expect it to contribute to revenue from next quarter (Q3) onwards.

Prabha would be deployed in the markets of Mexican region. So optimistically there operating day rates are more than 320 in a year, and so the rates what we are getting expression are in range of $50,000 a day. So, this particular asset would be deployed on those regions with similar kind of day rates.

We already are in advanced talks with few clients and we are deliberately not closing because we are trying since it is under refurbishment; we are of the view that we have a good amount of time to explore and get the better rates. So, contracts and expressions are already available with us. We are just looking in for the opportunity and we are going to time it in such a way that on one hand and we have equipment ready and on the other hand we have an order to be executed ready for signing.

So, we believe that on full year basis, a single barge can earn revenue of 90-100 crore. Could be 130-140crs if deployed on 300+ days and 50K$ rates.

o We have few opportunities available for Diving Support Vessel (DSV), Platform Supply Vessel (PSV) and Anchor Handling Tugs (AHT) in both local and international market and we are evaluating the same in terms of their margins and payback.

DSV and PSVs are not available as of now with Dolphin, so we are evaluating opportunities on getting some good contract. We may buy those assets. Targeting more than 15% ROCE from those assets. (Currently market is tight for these assets)

We have tugs (Tug Handling Boat) available, but they a not in class condition, so we’ll have to do refurbishment in that tug as well. So, we would be taking that in task based on the award of contract. We have SDS as well which is diving support system. So, in addition to tugs we have SDS as well. Those assets are also not in working condition, so we’ll have to get them in class.

o We have reported revenue of around 8 or some crore. So, this is particularly for a project which we have taken for execution for one of the DSV which we would be executing for our client where in our scope, it is sourcing, preparing and getting that asset is in class. So, with our experience of getting Prabha in class, we have taken parallel project for some small project, the revenue for which may be spread over three or four quarters, yeah. We are expecting total for us would be in range of around 40 to 50 crores over a period of projects.

We have kept ourself open for evaluating similar and other type of opportunities which are coming in our way.

o Dolphin shipping: it’s an associate or a sister company of Dolphin Offshore Enterprises. They also have one office in Mumbai and one or two tugs are also there with some receivables are also there.

• We are clearly expecting some awards to get awarded in one to 2 quarters.

• INCREASED OUTSOURCING OF INHOUSE OPERATIONS: One of the ideas was especially for the gas business or the gas processing business was that not only are the new orders being more prone to outsourcing, but existing operations could also be outsourced because people are just tired of managing the business themselves. Are we seeing that in actuality, are some of the bids that we’re bidding or some of the business that we’re winning, is it coming from captive processes now being outsourced?

Yeah, yeah. We got awarded some tender only last quarter. I think it was in this quarter or last quarter like I’m not very sure about it. So, we got the gas processing, gas compression facility which our client had and they outsourced the facility for smooth operation and maintenance. And that was also the one of the contracts that we got awarded. So likewise, we are sure that this concept is now getting very popular. And going forward, those will also be adding to our stream of business.

• Kandla Energy and Chemicals: It’s a very small investment of around 2 cr. They are owning one office in Ahmedabad and one land in Kutch, which is very much ideal land for setting up factory. So, few assets are still left. And since the value was not that much, and the manufacturing which they used to be in can be helpful in our synergy of drilling, so we decided to go for it.

So, we are going to set up a new plant over there? We as of now, we are just evaluating various opportunities what we can do out of that particular land and their original capacity of manufacturing those chemicals. So as of now, it is little early to say what exactly we will be going to do.

• In booster compressor, the demand is not coming up as per our anticipation and so there we are going slow. RAAS, we would be doing around 18 to 20 crore this year, that is what our expectation is.

• Euro Gas JV contract is still under evaluation.

• We’re looking at buying 3 new rigs during the year, which is again firm orders. In next four to six months, we’ll commercialize them.

CRAFTSMAN AUTOMATION – Diversified Light Engineering Company (13-08-2024)

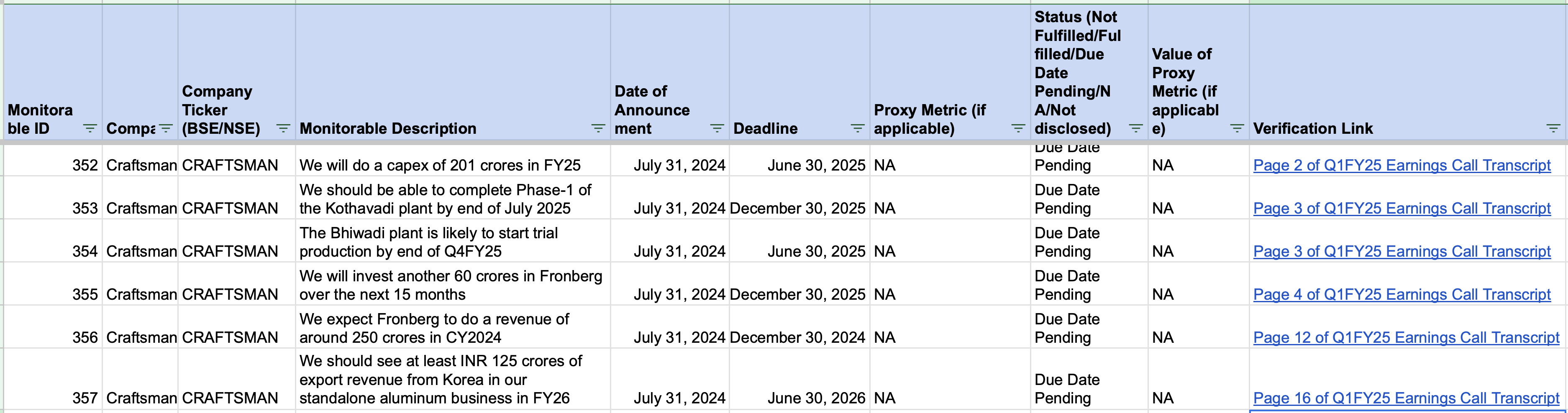

In the below tracker, I have started tracking important company goals for Craftsman. These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

- Company Ticker: For identifying the company

- Monitorable Description: Description of the goal or metric being tracked

- Date of Announcement: When the monitorable was announced

- Deadline: Target date for achieving the monitorable

- Status: Current progress (e.g., Not Fulfilled, Pending)

- Verification Link: A link to see where I got the information about the goal.

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables-17.xlsx (142.9 KB)

Post Script: DM if you want me to track the monitorables for any specific company.

Piccadily Agro Industries Ltd (13-08-2024)

United Spirits and Radico posted good Q1 numbers.

ValuePickr- Mumbai (13-08-2024)

Hello, I would like to join the WA group, have sent the request.