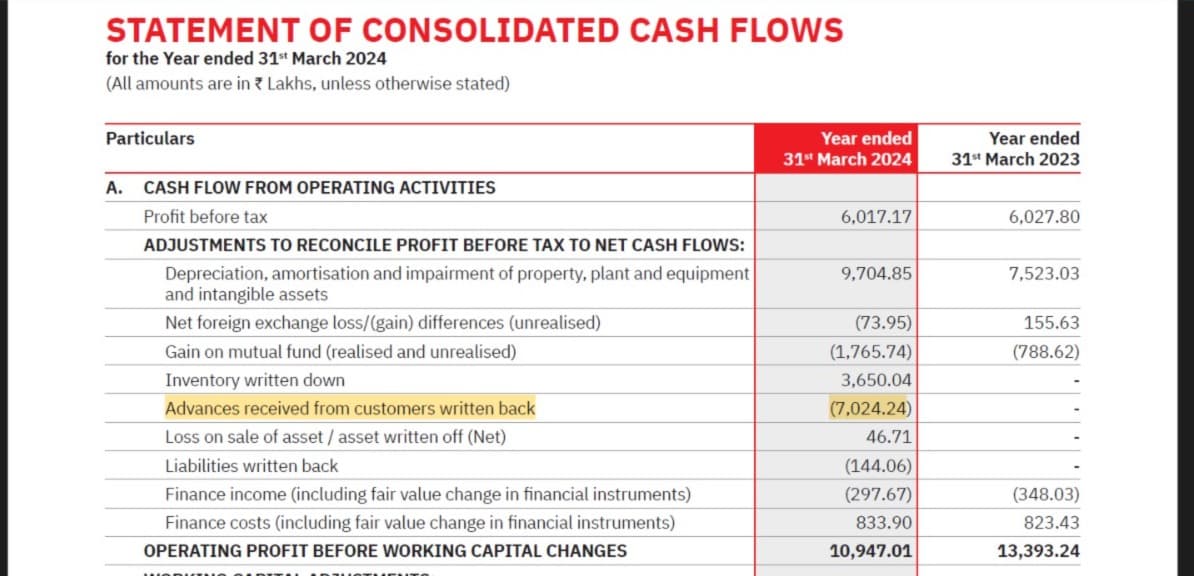

Any disclosure/further info on Advances written back ?

Any disclosure/further info on Advances written back ?

Terrible results. Exited. How are they going to get to 1Billion revenue in 5 years with this rate.

Few of my takeaways from Q1 FY25 of Britannia Industries

𝐂𝐨𝐫𝐩𝐨𝐫𝐚𝐭𝐞 𝐓𝐫𝐚𝐣𝐞𝐜𝐭𝐨𝐫𝐲:

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

Industry Tailwinds:

Industry Headwinds:

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

Competitive Landscape:

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

Opportunities & Risks:

Opportunities:

Risks:

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

Majority revenue still comes from steel trading and there is no pricing power there.

But my thesis for investment in Shankara has been –

(1) Growing Non Steel segment +

(2) Demerger value unlocking.

Both are still available. My concern is whether they can continue to grow non steel segment proftably and would their addl capacity at manufacturing can prove to be beneficial.

Let me know if anyone has any thoughts on this.

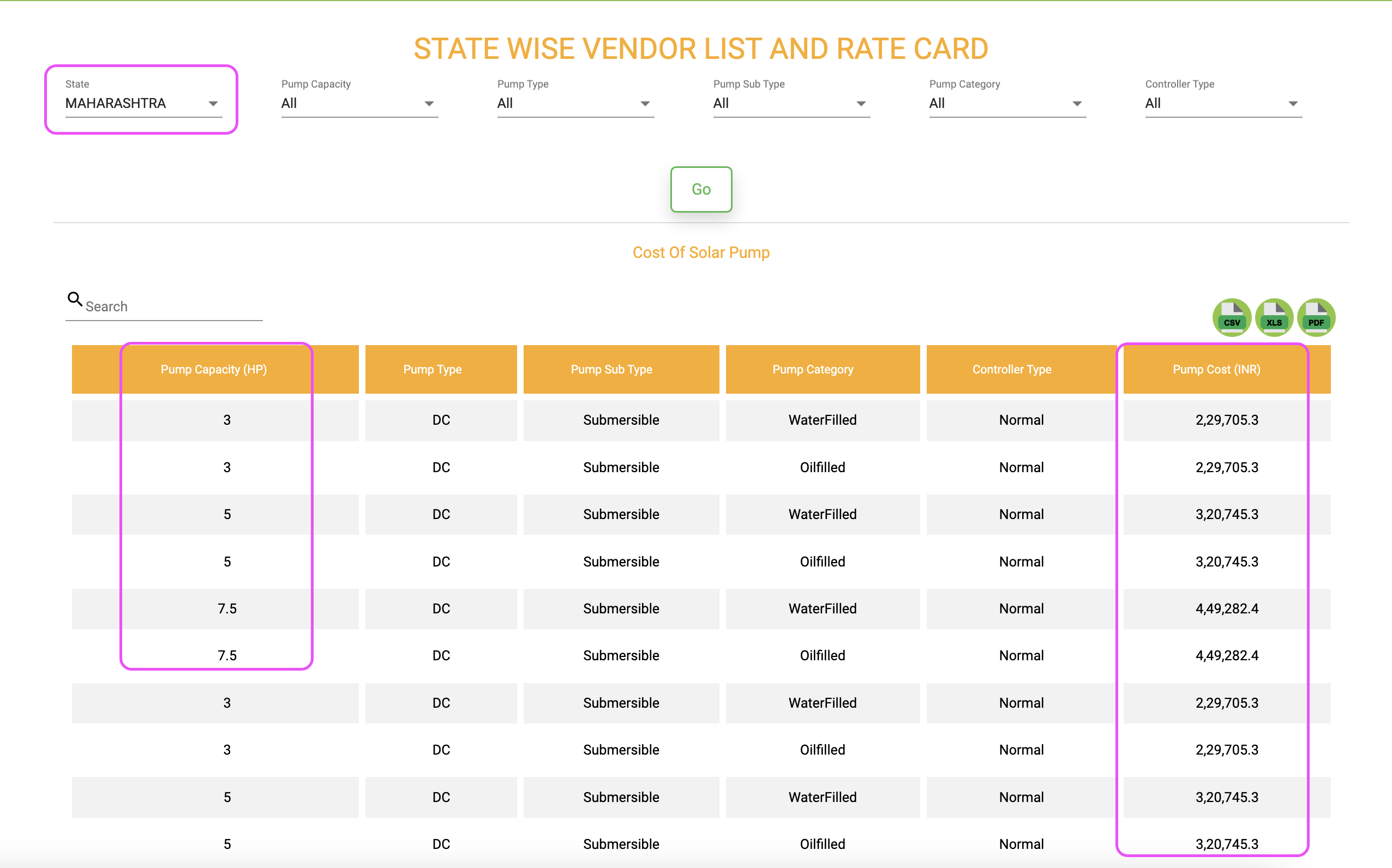

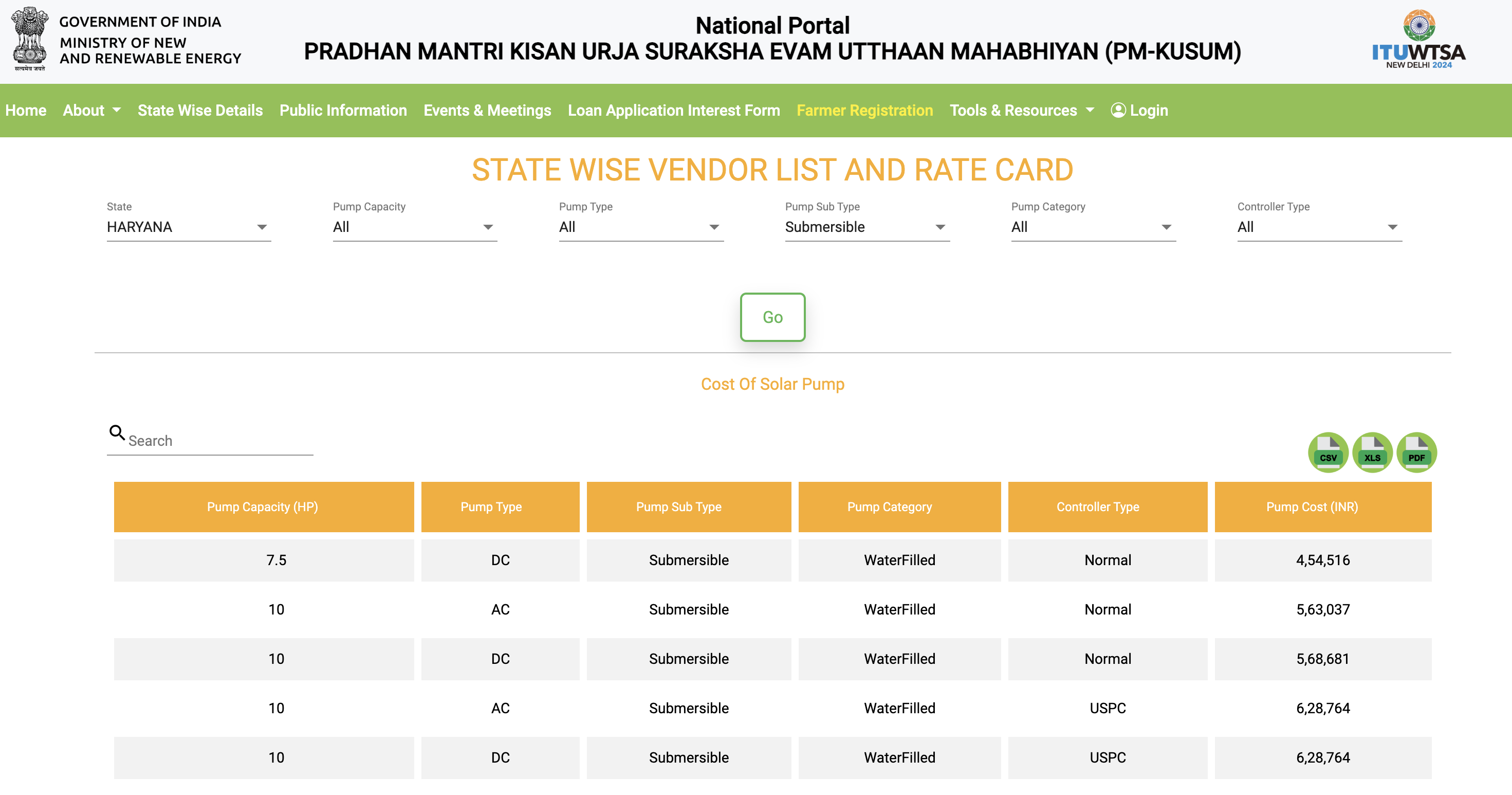

The rate card is fixed. It depends on the size of the pump.

Look at this data on the MNRE website:

For Maharashtra:

For Haryana:

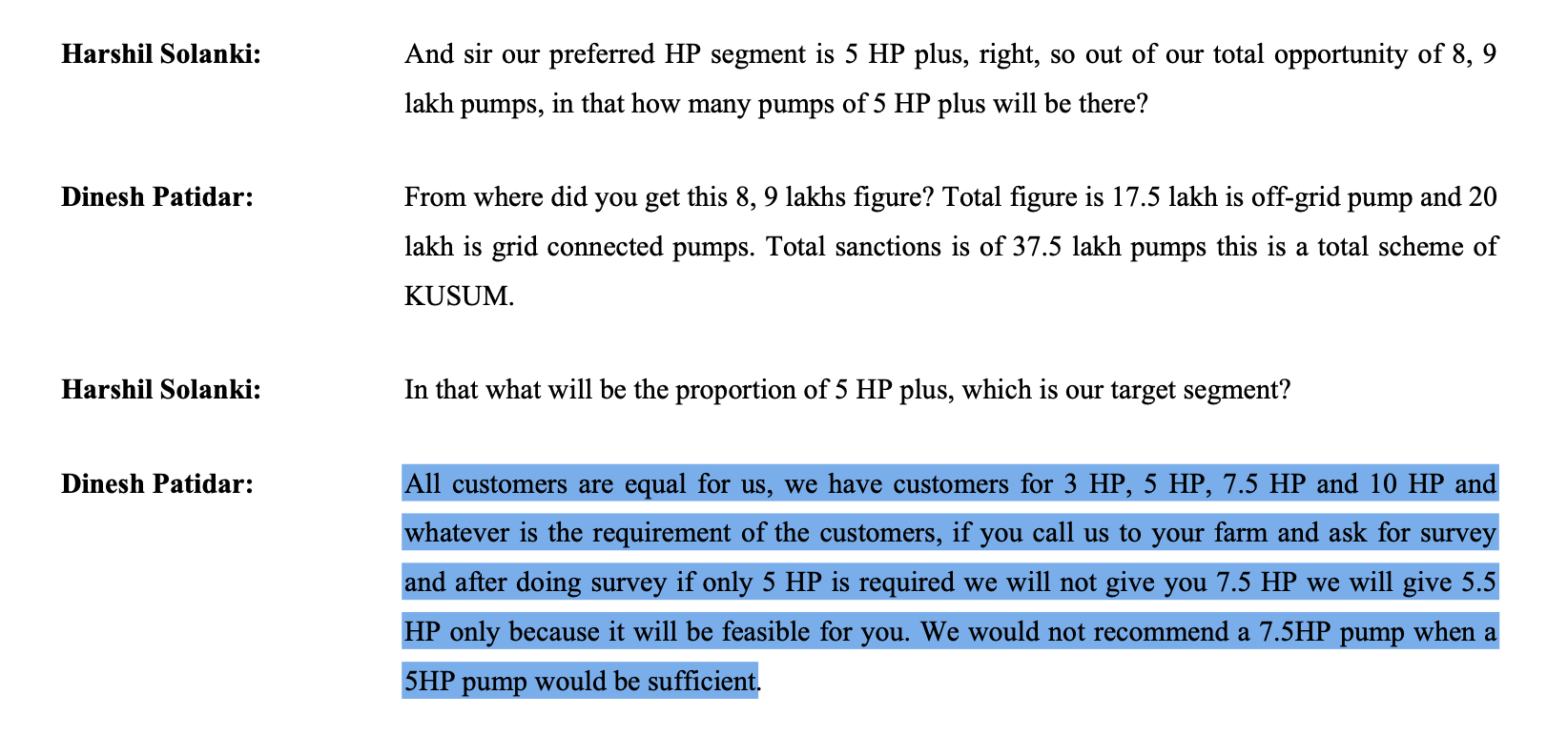

and as per the management commentary, what is the need for the farmer, given his area of irrigation, etc. they provide a valid rated pump:

Hope this helps.

Link: National Portal for PM-KUSUM (mnre.gov.in)

Btw – in the leanest quarter, distillery segment is delivering an EBIT of 25% or an EBITDA of around (26/27%). Make your own conclusions. The EBIT in Q4 was 30%+. As revenue for distillery segment goes up, overall blended margins would also inch closer to that of distillery segment.

The management of this company keep their financial data as it is.No window dressing, no inflated sales nothing. Business model of the company is good. I will keep holding my stake in it

I think lower margin guidance which is less than previous year, in the concall

What happened today? Why this rout? Stock is almost 13% down in early trades.

Not sure if the stocks would flow in market in October. The capex (which is the warehouse primarily & copper still pots etc that they’ve bought) is commissioned in October, which means the barrels are kept in the warehouse.

They then take around 1 year (not sure on this? but not 3 years for sure since Indri is NAS and takes less time to mature) to mature.

You add the time to shipment etc… so on and so forth.