Very good results

Very good results

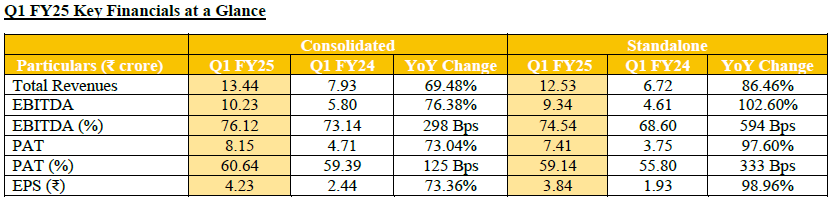

Sir @Rajesh_Singh did you check Kamat Hotels Q1 result? Is it on expected line?

Did anyone check the Q1FY25 result? Is it on expected lines?

Good update, wealth management is a decadal theme sir . Have a query , since you played last camphor cycle , currently looks like same thing happening. Gum terpene price is constant rise. What’s your take on this sir.

Hello ValuePickr Community,

I’m excited to introduce you to Screener Specter , a Chrome extension I’ve been working on. As a fellow investment enthusiast, I wanted to create a tool that could enhance our experience on Screener.in by providing additional insights and real-time data without the hassle of manual exports or spreadsheets.

What Screener Specter Does:

How It Can Be Useful:

I’m reaching out to this knowledgeable community for feedback and suggestions. Your insights could help improve Screener Specter and make it even more valuable for all of us. If you encounter any issues or have ideas for new features, please let me know. I’m eager to learn and grow with your help.

Looking forward to your thoughts and feedback!

In my opinion, Banks shifting towards spend based lounge access may not have significant impact on lounge pax number’s, as most of the people are maintaining multiple cards and now frequent flyers spend pattern will be across all cards to gain lounge acess in all cards. Irregular travellers will limit the spends to 1 card to gain access through that card only. Pax number may be stangant for few quarters and growth in number will be there after 3-4 quarters.

Margin improvement only possible immediately if they win any international deals

I have made the changes you pointed out. Thank you for the input.

Thanks for the AGM insights. Highly appreciated

Anything on holding concall. They didnt held it in the previous quarter as well

Shilchar AGM was conducted today. Key takeaways:

→ Demand and outlook continue to be strong both in India and exports. Current order book is 480 cr. Little delay in commissioning of new capacity mainly due to monsoons.

→ Will start utilizing new capacity mostly in H2 and expect 100% utilization in H2 itself. FY25 revenues expected to be 550 cr+ and expecting ~750 cr type of revenues in FY26.

→ Plan to manufacture transformers in same range as now since it’s a stronghold for the co. No plans to cater to higher kVA range.

→ Domestic & export demand both continue to be strong. Have successfully entered the EU market and like all markets it will take 1-1.5 years for significant revs to accrue. Expect this to be a strong market though can’t guide what percentage of revenue will come from here. Have already received first order. Mostly catering to the renewable sector in EU.

→ Though mgt didn’t answer it directly they seemed to suggest current profitability will sustain.

→ Call on next round of capex will be taken in Nov-Dec this CY(if I caught this correctly)

Q1 nos came few hrs post AGM. Probably for the first time Q1 revenues were same as Q4. This clearly underlines the strength in demand. If not for lack of capacity,revenues could’ve been higher than Q4 as well. Profitability continues to be strong and I sensed higher confidence on the same in the concluded AGM vs earlier years.

Disc.: Invested. Views are biased.

Thank you for your insight. I’m invested in wabag also.

In this case, can higher mcap to sales of EMS be justified by its higher OPM? Because of higher OPM, the PE of both the companies is around 30.

Also doesn’t Wabags 80% orderbook comprise of government orders, so that risk is similar?

All that said, Wabag indeed has better revenue visibility because of it’s much larger orderbook. But there have been some execution issues.