Please remove the quantity instead you can show percentage allocation.

Posts in category Value Pickr

Pratik’s Portfolio (12-08-2024)

Welcome to ValuePickr! It’s great to have you here. Your portfolio has a diverse mix of stocks, and it’s clear you’re investing with a long-term perspective, which is a solid approach. I’m curious about the specific reasons behind your choice of companies. What sets them apart from their competitors? Could you share more about the nature of their businesses and the growth opportunities you see in them? Looking forward to your insights and wishing you success on your investment journey!

Tips Industries Limited – Ready to RACE ahead! (12-08-2024)

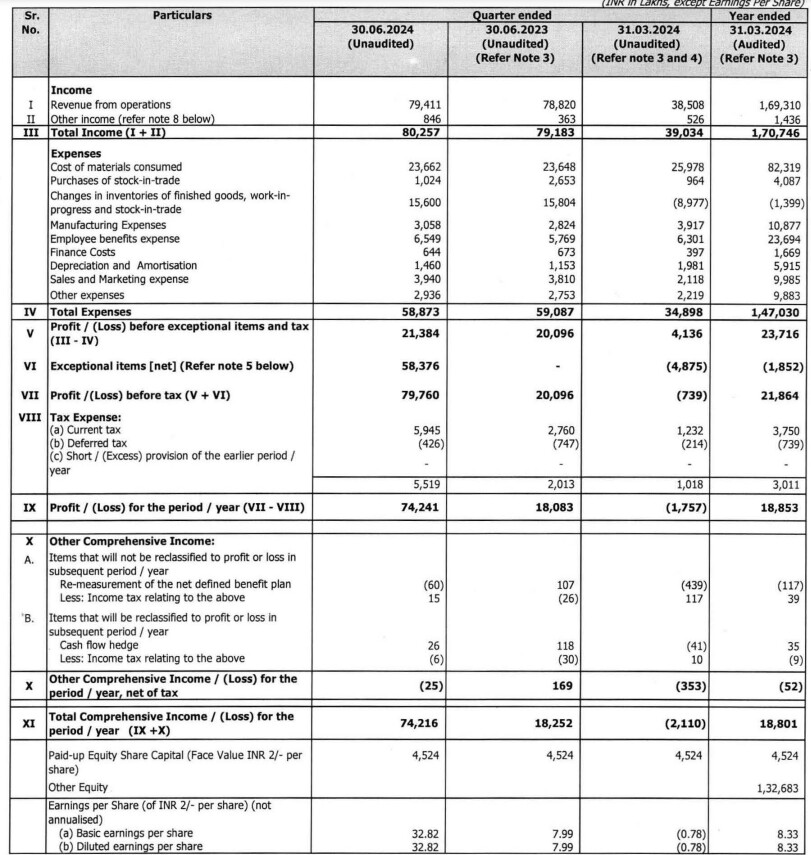

What’s the reason for the recent run up?

Kindly share your views

Sanghvi Movers (12-08-2024)

1188.92: Apr24-july24

Dabur: “Chawyanprash” with characteristic of “Real” “honey”, improving quality with age (12-08-2024)

The company seem to be doing everything right but still topline doesn’t seem to grow much. Last 2-4 years, Tata have grown foods/Sampann business tremendously, Marico has grown foods/Saffola business decently, Godrej has done fairly well in shaping their innovation product line ups etc. but Dabur doesnt seem to have developed any key category at an eye catching growth rate to understand next growth levers of the company. It seems to be pretty happy with the categories and product lines it already has – something like an HUL and happy with the slow & steady growth with no new big triggers…again correct me if wrong…

Lastly any insights into NEWU – the retail venture of dabur in the high growth beauty products segment. They never speak about this part then why they have ventured into it is not clear. What is growth/profit outlook and long term targets for this retail venture?

Disc: Invested since long as part of core portfolio hence critical & biased. Not a buy/sell recommendation. Post only for learning purposes.

Navneet Publications – a good com in education sector (12-08-2024)

Earnings are out.

Exceptional earnings due to:

Journey of a Small Cap investor! (12-08-2024)

Thank you so much Sir for this insightful thread. Looking forward to learn more from your knowledge through this community.

Balkrishna Industries (12-08-2024)

Q1FY25 Concall Summary

Business Updates

- The demand trends were healthy during the quarter but the growth in the quarter is also due to the lower base in the same quarter last year

- The environment in USA should remain tepid due to recessionary heawinds but the company should achieve minor volume growth in USA in FY25

- The tyre deliveries to European Union should confirm to new guidelines on deforestation on source of natural rubber from 31st December 2024

- The advanced carbon black project with capacity of 30000 MT is progressing as per schedule and the moulds plant is also progressing as per schedule

- The company will spends Rs 1300 crores in Bhuj to add capacity for OTR tyres of 35000 MT and this capex will be executed in phases

Participants

Nomura

Nuvama Wealth

Anand Rathi Institutional Equities

Equirus Securities

Ambit Capital

Incred Equities

Kotak Mahindra AMC

QnA

- The freight costs was lesser as the rates had been negotiated early but in the coming quarters the price of freight and RM both will be higher

- As of now there has not been any price hike and going forward demand seems weak so will wait before taking a decision on price hike

- The end user demand seems weak due to the various macro economic and geo political challenges persisting in the current environment

- The capex for FY25 will be between Rs 600-700 crores

- The channel inventories are also higher because of ongoing crisis in Red Sea due to which distributors have stocked up higher

- The acceptance for the 48 inch plus tires which are used in mining segment has been good and hence the new capex is primarily in the mining segment tires for radial tires

- The market share shall be maintained

- The sourcing of rubber should be from land where all local laws are being followed and has also not led to any deforestation since 2020

- The cost of rubber that is ethically sourced is costlier by around $300/MT and exports to European Union need to adhere to this sourcing

Pratik’s Portfolio (12-08-2024)

Zensar Technologies – (Qty- 182 Avg. 715.53)

Coforge – (Qty- 20 Avg- 5925.35)

ITD Cem – (Qty-18 Avg- 522.09)

HDFC Bank – (Qty- 7 Avg- 1418.65)

SBIN – (Qty- 7 Avg- 639.20)

SONABLW – (Qty- 8 Avg- 636.95)

Jio Financials- (Qty- 10 Avg- 307.75)

GPPL- (Qty- 10 Avg- 199.90)

Nippon IT Bees – (Qty- 135 Avg- 36.99)

GTL Ind – (Qty- 125 Avg- 219)

Hello Everyone, I am new to Value Pickr. I see interesting opinions and Portfolios here and that made me feel that i should ask for a review on my portfolio as well.

I do not have any fixed source of income as of now. The money i have invested is my savings. Whenever i get an opportunity, i try to invest whatever i can. All the investments i’ve made so far are with the intention to hold them for a long term.

Looking forward to learning from expertise that you all carry.

Samhi Hotels – Turnaround with Tailwinds (12-08-2024)

Samhi Hotels Q1FY25 Concall Summary.

Financial Performance

Revenue: SAMHI Hotels reported an asset income of INR 251 crores, marking a 31% year-on-year growth. This growth was driven by strong same-store growth and the addition of the ACIC portfolio.

Profitability: The asset EBITDA was INR 95 crores, showing a 32% increase year-on-year. The consolidated EBITDA stood at INR 89 crores, an 88% growth compared to the previous year. The reported PAT (Profit After Tax) was INR 4 crores.

Margins: The asset EBITDA margin was 37.7%, slightly diluted by the ACIC portfolio, which had a margin of 35%. The consolidated margin reached 34.6%.

Operational Metrics

RevPAR (Revenue Per Available Room): The same-store assets experienced a 13% year-on-year RevPAR growth, indicating robust demand in core markets such as Bangalore, Hyderabad, Delhi NCR, and Pune.

Occupancy: The company did not provide specific occupancy rates, but the focus on RevPAR growth suggests a strong occupancy performance.

Strategic Initiatives

New Locations and Expansion: SAMHI Hotels is actively expanding its inventory with plans to open 165 new rooms in Kolkata and Bangalore between September and November 2024. Additional projects include adding 22 apartments in Hyatt Regency Pune and 54 rooms at Sheraton Hyderabad.

Renovation and Rebranding: The company is renovating and rebranding several properties, including converting the Caspia Pro in Greater Noida to a Holiday Inn Express, and two ACIC portfolio assets in Pune and Jaipur to Marriott brands. These initiatives aim to enhance the average rate profile and EBITDA potential of these assets.

Future Outlook and Guidance

Growth Prospects: The management expressed confidence in both near-term and long-term growth, driven by macroeconomic factors such as the expansion of commercial office space and the aviation market in India. The company aims for a 10% to 15% inventory CAGR over the coming years.

Earnings Guidance: SAMHI Hotels expects significant EBITDA growth from renovation and rebranding activities, with a potential 25% increase in EBITDA based on FY24 numbers. The management anticipates high single-digit to low double-digit RevPAR growth in the upcoming quarters.

Management Tone

The management’s tone during the conference call was optimistic and confident. They highlighted strong market demand, strategic expansion plans, and operational efficiencies as key drivers for future growth. The focus on renovation and rebranding, along with disciplined capital allocation, underscores their commitment to enhancing shareholder value and maintaining a strong financial position