Open Offer was closed last week – Post Offer Document link

Now new mgmt just has to take care of the business, and hopefully share some updates with investors on future plans.

Open Offer was closed last week – Post Offer Document link

Now new mgmt just has to take care of the business, and hopefully share some updates with investors on future plans.

Thank you for summarized concall.

I am new to this counter so please pardon if i have some wrong understanding.

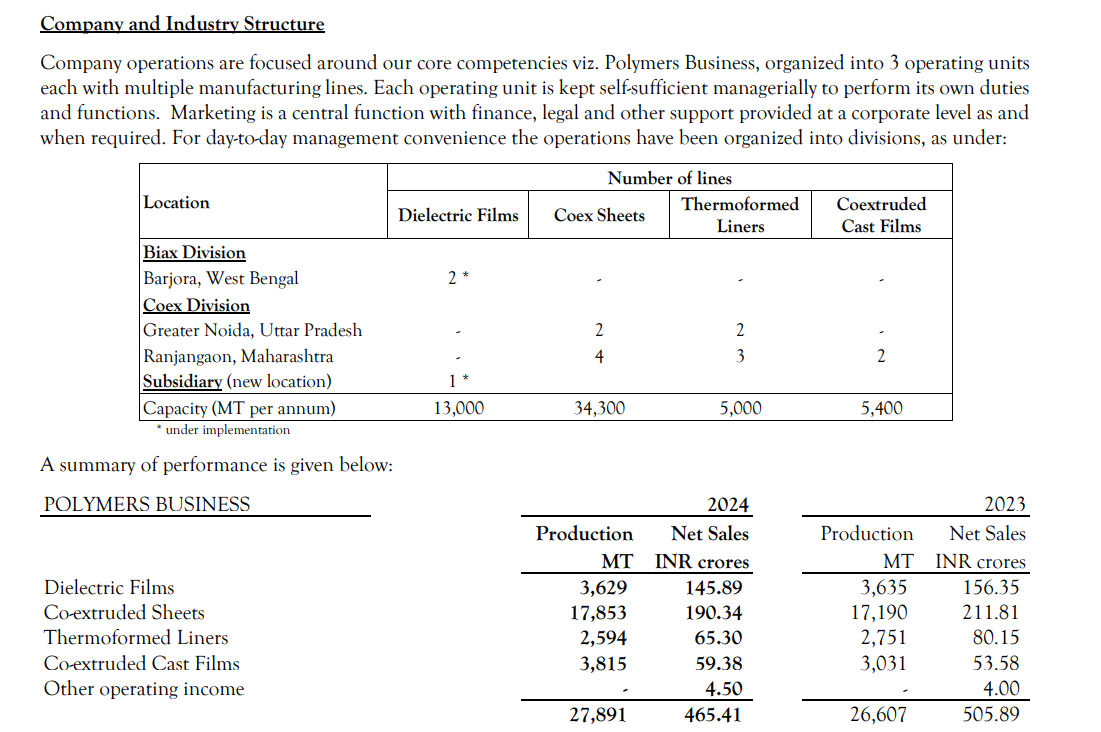

As management mentioned in concall they are working at full capacity in Dielectric films and they have done turnover of Rs.145 with this capacity. Now company’s capacity of Dielectric film will triple from this levels so we can expect revenue from the same in the rang of Rs.450-500 crs??

as all other segment is working almost at half of the capacity what kind of Turnover we can expect from CoEx division?

Thank you

Prashant

any new update regarding the take over ?

The contrast between the tremendous growth shown by potential clients like Inox, and the damp results and even more damp outlook given by Sanghvi could not be more ironical!**

While results have been good, not sure how to read the future.

Non-lounge services needs to grow which are supposedly high margins.

With banks shifting to spend based, a good number of “free” seekers having multiple cards most likely will go away. Counter argument can be with growing income and spending power, there are many who will still spend and use the benefits.

Moreover its low margin and there is rumor/news ? about Adani might venturing into this given they have few airports here

Dis: Wait and watch for now

Godrej Properties has expanded its land bank with the acquisition of a 90-acre plot in Khalapur, Maharashtra. The company plans to develop approximately 1.7 million square feet of residential plotted development on this land.

Ps: Inox is not a client of sanghvi.

MPS is clearly struggling with its margins. The OPM for Q4’24 had fallen to about 29%. This has further fallen to 23% in Q1’25, the lowest for many qtrs. I think it makes sense to switch from this one at current levels.

Aditya Birla Money has been growing aggressively for the last many quarters & looks good to continue on this journey going forward. Perhaps the leverage in the Co. maybe a touch high, but it should be kept in mind that is a subsidiary of Aditya Birla Capital Ltd., which has a market cap in excess of 55,000 crs & surely knows a thing or two about risk mgt.!! I see this as a multi year hold. There are huge tailwinds in the financial services sector/ wealth mgt./ funding aggressive equity investors- a tribe, which is growing by the day.

Few new members in Raymond Lifestyle board

https://raymondlifestyle.com/uploads/Composition%20of%20Board%20of%20Directors.pdf