Flat result QOQ given stress in the Microfinance not a bad result

Posts in category Value Pickr

ASM Technologies – Engineering innovation (11-08-2024)

Hey Guys, Q1-June-2024 Results are out for ASM Tech.

Please share insights ![]()

Schneider Electric Infrastructure: A global company with advantage of a industry tailwind: (11-08-2024)

Annual Report 2024 Highlights:

2024 overview and future roadmap:

Schneider Electric Infrastructure Limited (SEIL) experienced significant growth during the financial year 2023-2024. The company reported a revenue of ₹2,206.7 crore, marking a 24.2% increase from the previous year. This growth was driven by the rising demand for intelligent and energy-efficient solutions across various industries. Additionally, SEIL’s focus on cost optimization and operational efficiencies led to a 69.5% improvement in operating EBITDA, which increased from ₹179.9 crore in 2022-2023 to ₹305.0 crore in 2023-2024.

Looking ahead to 2024, SEIL is optimistic about its future prospects. The company’s outlook is buoyed by several factors, including the increasing demand for sustainable and energy-efficient solutions. SEIL is particularly focused on expanding its presence in the renewable energy sector, especially in solar and wind power, where it offers various integration solutions. Another area of growth is the digitalization of energy management and automation. SEIL is leveraging its expertise in IoT, analytics, and cloud computing to develop innovative solutions that optimize energy usage, reduce costs, and increase efficiency.

With these strategic focuses and a strong foundation built on innovation, SEIL is well-positioned to lead the industry towards a more sustainable future.

Plans for 2025 and beyond:

Schneider Electric Infrastructure Limited (SEIL) has outlined several strategic initiatives and future plans for the coming years, emphasizing innovation, sustainability, and digitalization. Here are the key components of their future plans:

1. Expansion in Renewable Energy:

- SEIL plans to significantly increase its presence in the renewable energy sector. This includes focusing on solar and wind energy solutions, where the company offers various integration and management solutions. The aim is to support the global shift towards cleaner energy sources and capitalize on the growing demand for renewable energy.

2. Digitalization of Energy Management:

- The company is prioritizing the digitalization of energy management and automation solutions. Leveraging its expertise in IoT (Internet of Things), analytics, and cloud computing, SEIL is developing innovative solutions designed to optimize energy usage, enhance efficiency, and reduce operational costs. This digital transformation is expected to be a critical growth driver, helping industries manage energy more intelligently and sustainably.

3. Sustainability Initiatives:

- Sustainability remains at the core of SEIL’s strategy. The company is committed to promoting energy-efficient solutions that reduce environmental impact. SEIL plans to integrate more sustainable practices across its operations and continue offering products and services that help customers achieve their sustainability goals.

4. Expansion of Product and Service Offerings:

- SEIL aims to expand its portfolio of products and services to meet the evolving needs of its customers. This includes introducing new technologies and solutions in the areas of energy distribution, automation, and smart grids. By expanding its offerings, SEIL hopes to capture a larger market share and address the growing demand for advanced energy management solutions.

5. Global Market Penetration:

- The company plans to strengthen its presence in international markets by leveraging its global network and expertise. This includes entering new markets and expanding in regions where the demand for energy-efficient and sustainable solutions is increasing.

6. Focus on Innovation:

- Innovation is a key focus area for SEIL. The company is investing in research and development (R&D) to stay ahead of industry trends and bring cutting-edge solutions to the market. SEIL’s future plans involve continuous innovation to address the challenges of energy management and sustainability in the modern world.

These plans reflect SEIL’s commitment to leading the industry through innovation, sustainability, and digital transformation, positioning the company for long-term growth and success.

Disclosure: Invested.

360 One WAM Ltd (Erstwhile IIFL Wealth) (11-08-2024)

360One name has come in the Hindenburg latest report about SEBI on the negative side. Any caution around it?

Simple Investing (11-08-2024)

I have just about started looking into it.

The concern is the limited areas it plays in and the lack of management will. The main question is whether this is constrained by the parent. Almost minimal information is one more drawback here.

Will likely put it in too hard to analyse pile and move on.

Smallcap momentum portfolio (11-08-2024)

360One has come up in the Hindenburg latest report about sebi on a negative side. Any caution with respect to it?

The Anti-Portfolio (11-08-2024)

@HarshVijay thanks! Exactly a month ago I collected all the money required for the property deal, by selling beta drugs and rest.

Yes, its promising but personally speaking my timing was wrong, had miscalculated my math, which I wanted to correct now. Think am too lazy for SME dealing, typically my trades are once every 2 months on average and I run my orders in few minutes, liquidity can be disruptive to prices ![]()

EMS Limited – Tapping in the growth in the water management space (11-08-2024)

Initiating a second thread on EMS Limited, because the previous one here is locked.

EMS Limited is a multi-disciplinary EPC company, headquartered in Delhi that specializes in providing turnkey services in water and wastewater collection, treatment and disposal. EMS provides complete, single-source services from engineering and design to construction and installation of water, wastewater and domestic waste treatment facilities. – Screener.in

Financials –

Note:

- Current P/E is higher than the historical P/E (~24) of the stock. This can mainly be attributed to the increased national budget allocation towards water supply and waste management projects.

- Low on debt.

- Decent ROE.

Profit and Loss –

Note:

-

Consistent top-line and bottom-line growth.

- Top-line growth from the past 2 financial years has been around 48%. Bottom-line has grown around 39% in the same time period.

- The TTM top-line growth is around 43%.

- In the February 2024 con-call, the management has guided towards a growth of 35-40% in the current FY.

-

OPMs are decreasing with scale. Still significantly higher than competitors, ION Exchange and VA Tech who have averaged around 10-13% OPM.

Promoters –

Couldn’t find anything interesting about the promoters Mr. Ramveer Singh and Mr. Ashish Tomar other than what is mentioned on the company website, here.

Business Overview –

The operations of the company can be broken down into the following broad categories.

-

Sewage Networks

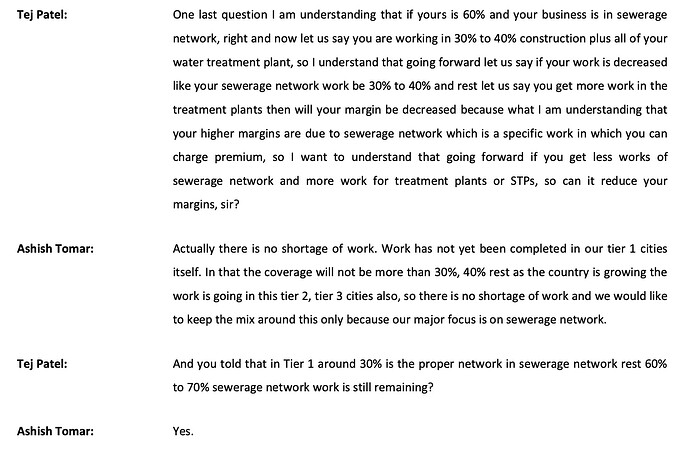

- 60-70% of the order book.

- Commands higher margins. This is the main reason behind the higher margins enjoyed by EMS limited compared to its peers.

- Promoters say, since there is a lot of work to do in this sector, they’ll maintain this share of sewage work in the order book and thus continue enjoying the higher OPMs.

-

STP and other construction.

- 30-40% of the order book.

-

O&M is currently 10% of annual revenue but according to the promoters this should increase with time.

According to ICRA, by the end of January 2024, the pending order book of the company stands at ~2093cr, which is to be completed in the next 2-3 years.

Recently the company was awarded two more orders,

- First from UP Jal Nigam, an STP project worth 119cr, where EMS would have a 26% share in a JV.

- Second from Uttarakhand Power Corporation. An infrastructure project to reduce energy loss during power distribution. EMS has a 95% in the project.

The company’s main revenue comes from north India, mainly from Rajasthan, Uttarakhand, Uttar Pradesh and Bihar. The company is also bidding in MP, Jharkhand and West Bengal. They have also shared the intent to expand to other states, but haven’t given anything concrete yet.

The company directly deals with the government and does not do any subcontracting for the work. Only labour is sourced from contracting. The equipment is sourced via rentals and thus company capex is very low.

Company’s projects are usually funded by the central government or agencies like, Asian Development Bank, World Bank, etc. So the company doesn’t generally face any payment or funding related issues.

The company has announced acquiring Brijbihari Pulp and Paper Pvt Ltd. It is not clear how this acquisition fits into the competencies of the company.

Key Risks –

-

Business relies on government spending and thus is susceptible to policy changes.

-

The company is a little defensive about project choices and wants to ensure higher margins. Increase in competition might hamper the order wins and margins of the company. As of now, the company is awarded only 12% of the orders it bids for.

-

Troubles with the law

- The company was recently investigated for GST irregularities.

- The company was black-listed by two government agencies for the death of 5 labourers due to lack of adequate safety equipment (only read it here).

- Another unrelated black-listing order was quashed by the Bihar High Court.

Disclosure – Invested from lower levels.

The Anti-Portfolio (11-08-2024)

Thanks @MarketYogi leverage is a big no! I started investing with the great small cap carnage of 2018 seeing a 40% drawdown and stayed invested in 2020 crash seeing a total 70% drawdown!!

Markets can remain irrational longer than you think. Yes, 2020 was a V shaped recovery and macros are vastly different now than in 2018 but history can repeat!!

As you see I am too lazy and not agile enough to buy and sell fast enough to mitigate risky situations. Currently market has favoured me, that’s all. Not too keen on increasing the risk factor here ![]()