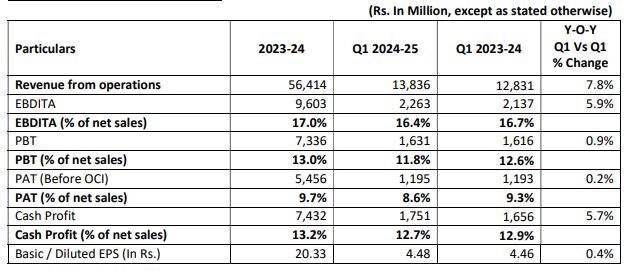

Astral reported flat Q1FY25 numbers

Slight increase in revenue but the slight dip in EBITA margin led to flattish PAT.

Astral reported flat Q1FY25 numbers

Slight increase in revenue but the slight dip in EBITA margin led to flattish PAT.

An investor should always be an optimist but the analyst in you, must always be skeptical about things. My advice will be to study the business environment of the said scrips and check whether these companies are operationally capable to operate in this business environment.

Self research and judgement is priceless.

Thank you so much for your kind words. Good luck.

Very good result, revenue & EPS up (yoy) for the quarter 40% & 36% respectively.

I’m no expert but here is my understanding.

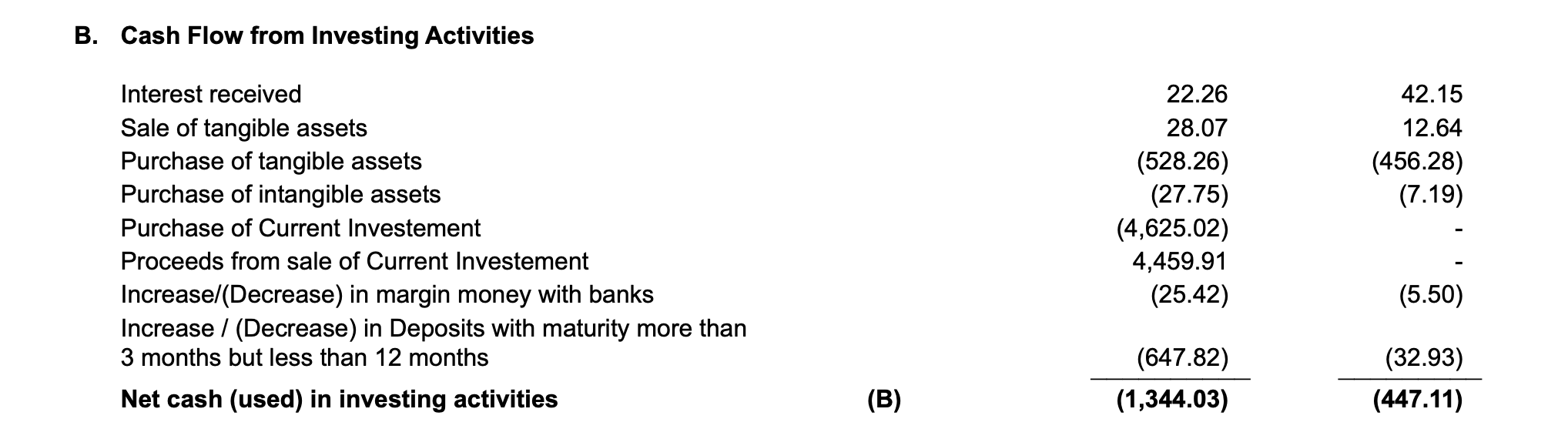

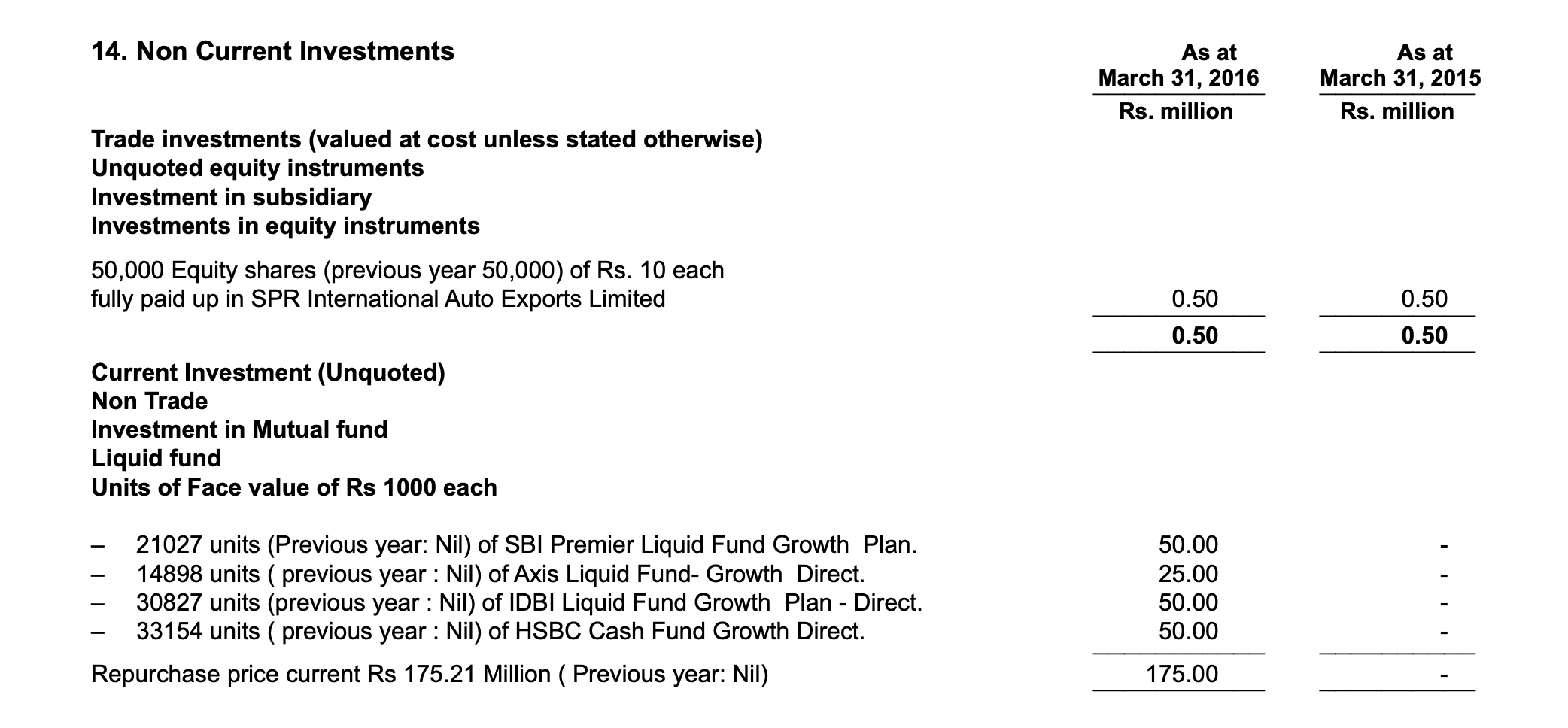

We can see that the company purchased investment worth 463 Cr and sold investments worth 446 Cr within the same financial year. So I think these are short term investments.

These are labeled as current investments in the cash flow statement.

We notice while reading the Notes to the financial statements in the Annual Report, the details of the current investments are provided but the amount of investments purchased/sold does not match the amount in the cash flow statement.

If we calculate investments purchased – investments sold, 463-446 = 17 Cr, it roughly matches the 175 Million amount mentioned in the notes. So here, they are probably reporting only the investments held at the end of financial year after all the buy/sell transactions and not the details of all the investments bought and sold during the year.

So, most probably they bought/sold lot of mutual fund units throughout the year which is reflected in the cash flow statement.

On the question about why they are doing it, they are probably just parking the working capital/ reserves in liquid funds till they find a use for it like paying bills, suppliers etc.

Abbott India – Messiah for the sloppy stock pickers

Pharma is very interesting sector where I believe the acceptance of “I am not a good stock picker” has helped me to generate above average returns.

Amongst all pharma companies, I believe Abbott India is the simplest business to understand especially for some one which focusses on 3-5 years earnings growth. Mid teen EPS growth with 100% ROIC, ever growing free cash flows year after year along with some certainty on the capital allocation make it more desirable portfolio candidate for me compared to capital intensive / lumpy CDMO businesses

The problem comes when I try to look beyond 5 years, disassociate myself from earnings growth and try to find “what” makes Abbott India’s franchise so strong to crunch cash conversion cycle from 44 days 10 years back to -25 days now. Failure to understand building blocks of the franchise make it difficult for me to assess its durability in future

Seems like 1000 cr topline by Fy25 is already baked in the price. Can anyone share what’s the guidance beyond FY25. They should reach near 1000 cr this year more or less.

Would it make sense if we extrapolate Q1-24 results with above generalized % ?

Q1-24 results:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/3b48c58f-3ad0-4bbc-ba5a-9e1c1695b508.pdf

10-12% growth of dining corelate with 13% growth rate of dominos. I have seen dominos open new stores in many places in my tier 3 city. One outlet just got opened near my house at 400m distance and that is not some shopping mall or airport or railway station, its just a regular market place. La Pinoz is not good so I don’t track that. Even new shopping malls are opening which will have atleast 1 dominos outlet.

And food delivery is growing at 20% bcz market potential is not yet tapped and market potential is 3000Cr as of 2024 after which growth will come down to 10-12%.

And regarding ecommerce I don’t have much interest in that. I see it only as a threat to zomato, better to get rid of it asap. Or at least separate it so that it doesn’t affect zomato.

An article on slump in Disney theme park revenue offset by Inside Out sequel and Disney+ streaming service revenue.

This is a very unidirectional view. You should look at the industry growth. Based on the estimates “Dining Out” growth is expected to be 10-12% for the next 5-6 years (just google it and you will find any articles). While these companies (dominos, CCD) have not grown look at the number of restaurants and cafes around you, the shear number of restaurants has grown so they have taken growth from these companies (look at the growth of cafes, growth of La Pinooz pizza to name a few). Food delivery growing at 20% is easily possible for the next 5 years (this is also what management has told).

Also, the calculations include only food delivery profits. I believe Quick Commerce is going to be a bigger market than Food Delivery (I spend more on instamart and blinkit than food delivery). You should bake that in your calculations.

Disc: Invested and Biased.