| Equity Portfolio | ||||

|---|---|---|---|---|

| NAME OF COMPANY | CMP 07-08-2024 | Allocation | UNREALISED GAIN | |

| AVG INVST PRICE | ||||

| SRG Housing Finance | 204.28 | 382.25 | 30.6% | 87.1% |

| Punjab Chemicals | 772.45 | 1,237.00 | 20.4% | 60.1% |

| Mitsu | 149.87 | 143.05 | 3.1% | -4.6% |

| Innova Captab | 499.09 | 621.85 | 7.9% | 24.6% |

| IRM Energy | 537.21 | 449.20 | 5.4% | -16.4% |

| Prevest Denpro | 377.47 | 617.00 | 4.7% | 63.5% |

| Prime Fresh | 200.29 | 199.00 | 10.4% | -0.6% |

| India Pesticides | 216.50 | 208.00 | 9.2% | -3.9% |

| Transpek | 1,750.76 | 1,717.00 | 8.3% | |

| CASH | – | 0.0% | 0.0% |

Posts in category Value Pickr

Kalpesh’s Portfolio (07-08-2024)

Stylam- Decent Fundamentals with Cheap Valuation (07-08-2024)

EBITDA margins contracting from peak of 20% and stagnant revenues. A worrying sign for profits and stock performance

Shivalik Bimetal Controls Ltd (SBCL) (07-08-2024)

Promoters really pumped up expectations with a long term guidance and then did a block deal in Q2FY24 and sold down stake.

A cautionary tale for everyone, “Dont trust the promoters when they spin stories especially when they want to sell their own stake”

Adani Wilmar Limited (AWL) – Essential kitchen commodities (07-08-2024)

Adani Wilmar Q1 FY25 Analysis: Key takeaways!!

Adani Wilmar reported strong Q1 FY25 results with 12% year-on-year volume growth and significant improvement in profitability. The company’s edible oil segment performed exceptionally well, crossing 1 million tonnes in quarterly volumes for the first time. The food and FMCG segment continued its impressive growth trajectory, with revenues reaching ₹1,500 crore. Management expects this momentum to continue, targeting 30-40% year-on-year growth for the next three years in the food segment.

Strategic Initiatives:

- Expanding rural distribution: Targeting 50,000 rural towns by March 2025, up from current 30,000.

- Premiumization: Launching premium products like “Pehli Dhaar” first press mustard oil and expanding the “Expert” range of functional oils.

- B2B focus: Developing specialized flour products for industrial customers.

- Capacity expansion: New integrated food park in Gohana to boost rice processing capabilities.

- Strengthening HoReCa channel: Expanded to 48 towns, targeting 100+ large towns.

Trends and Themes:

- Stable edible oil prices benefiting branded players

- Increasing demand for premium and functional food products

- Growing importance of alternative distribution channels (e-commerce, quick commerce)

- Rising rural consumption

Industry Tailwinds:

- Expected good monsoon boosting rural demand

- Government initiatives to increase rural productivity and employment

- Upcoming festive and wedding seasons driving consumption

Industry Headwinds:

- Intense competition from regional players in food segment

- Potential volatility in commodity prices

- Currency fluctuations in international markets (e.g., Bangladesh)

Analyst Concerns and Management Response:

- Concern: Lower profitability in food segment

Response: Intentional investment in distribution and marketing to drive growth - Concern: Bangladesh operations losses

Response: Situation improving with stabilizing currency and new government policies

Competitive Landscape:

- Edible Oils: Adani Wilmar maintaining market leadership with 19% share

- Wheat Flour: Gaining market share, now at 5.9%

- Rice: Facing strong competition from established players, currently at 8% market share

Guidance and Outlook:

Management expects to maintain the current performance levels, anticipating strong demand during the festive season. They aim to close FY25 with 1.25 million tonnes in the food and FMCG basket.

Capital Allocation Strategy:

- Investing in distribution infrastructure and marketing for food segment

- Expanding processing capacities (e.g., Gohana plant)

- Exploring opportunities in value-added segments like oleochemicals and castor derivatives

Opportunities & Risks:

Opportunities:

- Expansion in premium product categories

- Growing export markets for branded products

- Potential for market share gains in fragmented food segments

Risks:

- Commodity price volatility

- Increased competition from local and regional players

- Regulatory changes affecting edible oil imports or pricing

Regulatory Environment:

- Government restrictions on white rice exports impacting the rice business

- Potential changes in import duties on edible oils

Customer Sentiment:

Management noted steady and improving demand for branded and food products. Rural markets show signs of recovery, with expectations of stronger growth from October onwards.

Top 3 Takeaways:

- Strong performance in edible oils segment with 12% volume growth and market share gains

- Continued rapid expansion of food and FMCG business, growing at 30%+ year-on-year

- Strategic focus on distribution expansion, premiumization, and value-added products to drive future growth

Shivalik Bimetal Controls Ltd (SBCL) (07-08-2024)

The CFO says, “Despite a 5.18% decrease in total income to ₹107.22 Crore, our strategic focus on volume growth yielded an 8.58% increase in product volumes, underscoring the resilient demand for our products.”

This is a dumb statement! It’s like saying “I made less money, but on the other hand I am proud I sold more quantity”. Well, as even a fourth grader will tell you, if you reduce prices you will sell more! It is not “…underscoring resilient demand for our products”.

An decrease in Income of 5.18% against a volume growth of 8.58% means a price drop of 12.7% per unit volume, in an inflationary environment.

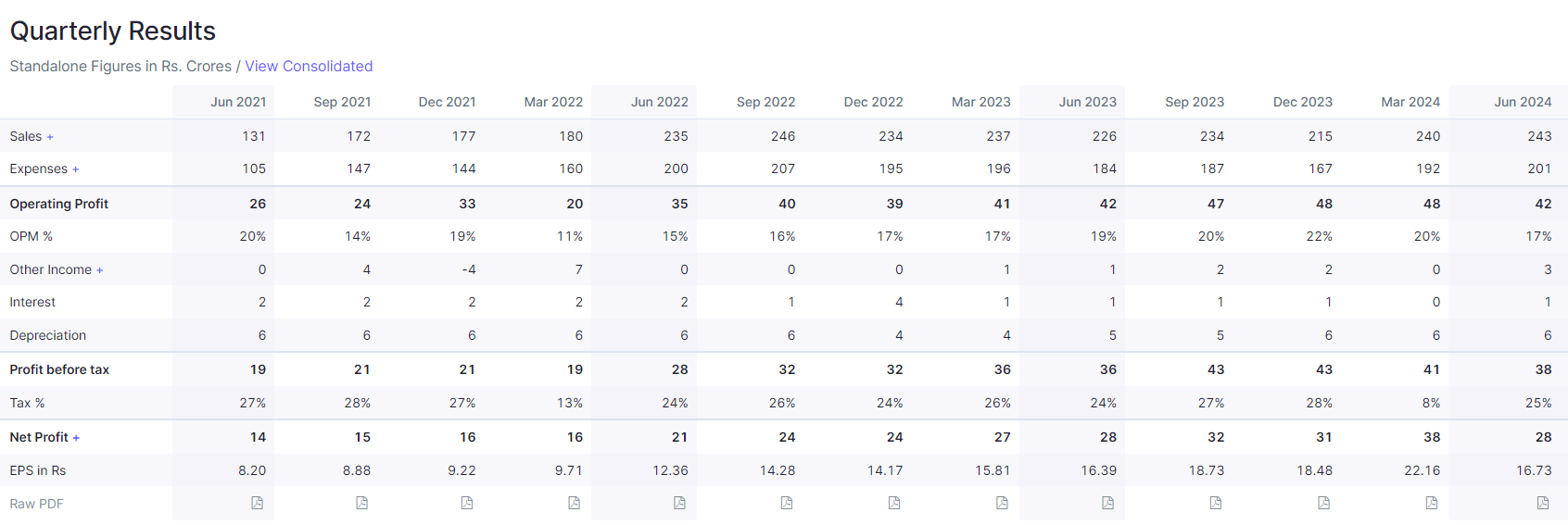

Action construction equipment ltd (07-08-2024)

Action Construction Equipment Q1 FY25 Analysis: Key takeaways!!

Action Construction Equipment (ACE) demonstrated strong performance in Q1 FY25, achieving its best-ever Q1 results despite the impact of general elections. The company reported a 12.82% year-on-year revenue growth to INR734 crores, with EBITDA margin expanding by 212 basis points to 17.11%. This resilient performance indicates a positive outlook for the company, supported by government infrastructure spending and growing demand across segments.

Strategic Initiatives:

-

Joint Venture with Kato Works: ACE has reached an in-principle agreement with Japanese manufacturer Kato Works to establish a 50-50 joint venture in India. This partnership aims to produce medium and large-sized cranes, including truck cranes, crawler cranes, and rough terrain cranes, for both domestic and export markets.

-

Expansion into Higher Tonnage Cranes: The company is focusing on expanding its product range to include higher tonnage cranes, addressing the growing demand for larger capacity equipment in infrastructure and construction projects.

-

Electric Crane Development: ACE has developed electric cranes and is awaiting government approvals for commercialization, positioning itself for the transition to cleaner energy solutions in the construction equipment sector.

Trends and Themes:

-

Shift towards higher tonnage cranes: The market is gradually moving from 15-ton to 20-25 ton cranes, with expectations of 30-35 ton cranes becoming more popular in the coming years.

-

Increasing adoption of new generation cranes: The market share of new generation cranes has grown from 5-10% to about 35% in recent years, indicating a shift towards more advanced and safer equipment.

-

Growing demand for tower cranes: The tower crane market is booming, particularly in the real estate sector, with ACE expecting a 20-30% increase in tower crane production this year.

Industry Tailwinds:

-

Government infrastructure push: The central government’s continued focus on infrastructure development, with a capex budget of INR11.11 lakh crores, is driving demand for construction equipment.

-

Pre-buying ahead of emission norms change: The upcoming transition from BS IV to BS V emission norms is expected to drive pre-buying in Q3, potentially boosting sales.

-

Revival of private capex: Increasing private sector investment in infrastructure and construction projects is creating additional demand for cranes and construction equipment.

Industry Headwinds:

-

Seasonal slowdown due to monsoons: The construction equipment industry typically experiences a slowdown during the monsoon season, affecting short-term demand.

-

Intense competition in certain segments: The presence of Chinese players in the truck crane and crawler crane segments has intensified competition and pricing pressure.

Analyst Concerns and Management Response:

Concern: Impact of elections and monsoons on Q1 performance.

Response: Management highlighted that despite these challenges, the company achieved its best-ever Q1 performance and expects momentum to improve post-August 15th.

Concern: Margins in the agri division.

Response: Management expects demand to improve with the advancement of monsoons, better liquidity, and consumer credit availability.

Competitive Landscape:

ACE maintains a strong position in the pick and carry crane segment and is a leader in tower cranes. The joint venture with Kato Works is expected to strengthen its position in the higher tonnage crane market, where Chinese players currently dominate.

Guidance and Outlook:

The company has reiterated its guidance of 15-20% growth on a consolidated basis with sustained margins for FY25. Management expressed optimism about potentially revising these projections upward by the end of Q2 or early Q3.

Capital Allocation Strategy:

ACE has acquired 82 acres of land for capacity expansion, with plans to start development on 22 acres as early as Q4 FY25. This indicates a focus on organic growth and capacity enhancement to meet increasing demand.

Opportunities & Risks:

Opportunities:

- Growing infrastructure investment in India

- Expansion into higher tonnage cranes through the Kato Works joint venture

- Potential for increased exports leveraging the Kato network

Riskemphasized texts:

- Dependence on government infrastructure spending

- Cyclicality in the construction and real estate sectors

- Intense competition in certain product segments

Regulatory Environment:

The transition to BS V emission norms for construction equipment is a key regulatory change that could impact the industry. ACE is positioning itself to benefit from pre-buying ahead of this transition.

Customer Sentiment:

Management indicated strong interest from major construction companies in their new products, particularly in electric cranes and multi-activity cranes (NX series).

Top 3 Takeaways:

- ACE’s strategic joint venture with Kato Works positions it for growth in the higher tonnage crane segment and potential export opportunities.

- The company’s focus on new generation cranes and innovative products like electric cranes and multi-activity cranes demonstrates its commitment to technological advancement.

- Strong government infrastructure spending and the revival of private capex provide a favorable demand environment for ACE’s products in the medium to long term.

MAS Financial Services – High RoEs, Decent Growth (07-08-2024)

Company has been performing so well but why is the stock not moving upwards?

Would you consider MAS to be extremely undervalued too?

Shilpa Medicare -Racing away on the Oncology API highway! (07-08-2024)

Sucessfully completed the Phase 1 clinical trials for rHA (Recombinant human albumin)

69b044ba-abc8-4379-866f-a82693d60056.pdf (625.8 KB)

Nitin Spinner – textile yarn story (07-08-2024)

Bangladesh Crisis Impact on Nitin Spinners:

Nitin Spinners has about 60% recevenue contribution from Exports market (About 1800 cr) and out of that 60% it exports about 20% yarn to Bangladesh (about 360 Cr) which comes out to be around 12% of sales figure (of about 3k cr) which might be impacted severely due to Bangladesh crisis. If the Management clarifies how much of business is impacted that will make more sense. Let us share here if there are management comments on the topic in any public forum. Thanks