Yeh, I saw that, has anyone written to the investor relations for getting the link?

Posts in category Value Pickr

India Pesticides Ltd (05-08-2024)

Has management specified any number that they are expecting coming from plant of hamirpur in FY26?

Or percentage contribution vs total sales for FY26 for plant of Hamirpur ?

SG Mart- Can it successfully create a marketplace? (05-08-2024)

the link is not a hyperlink (not clickable)…

India Pesticides Ltd (05-08-2024)

Taking the guidance at the face value .

Let’s say they post 15-20% of growth in FY-25.

With margins of around 18-20% post Q3.

And around 13% in first two quarters.

They can safely post eps of around 10 INR for full FY.

I’m trying to understand what must be the multiples street would be comfortable with a stock like IPL.

Obviously that will change company to company.

But would the street be comfortable with the stock trading at 30 PE multiples?

NPST – Technology Provider for UPI Tech (05-08-2024)

Exactly but given they’ve mentioned that they’re processing almost 6% transactions and it is a volume game, I think it’ll have a noticeable impact.

SG Mart- Can it successfully create a marketplace? (05-08-2024)

Has anyone got the link to register for the concall?

Rajesh’s portfolio (05-08-2024)

There is no sun retail in my portfolio so cant comment , you may be talking about Sonalis consumer , its quarterly update, preferential and bigger goals ahead are game changer can study that.

NPST – Technology Provider for UPI Tech (05-08-2024)

Yeah, for the UPI switch it’s per transaction revenue for NPST, and the same for any kind of switch (transaction processing engines under TSP). Switch cost is usually very low (in paisa per transaction) but if you look at the overall level it will become huge and no of transactions is a lot. I am also not sure about the revenue share investor deck does not give details on this.

Dixon Technologies (05-08-2024)

Dixon Technologies Q1 FY25 Analysis: Key takeaways!!

Dixon Technologies has started FY25 on a strong note, with 101% YoY revenue growth to INR 6,588 crores in Q1. The company is well-positioned to capitalize on India’s consumption growth and the “Make in India” initiative. Management expects aggressive growth to continue, driven primarily by the mobile and IT hardware segments.

Strategic Initiatives:

- Expanding mobile manufacturing capacity to 55-60 million units annually, including the Ismartu acquisition.

- Backward integration in components, especially display modules and mechanical parts.

- Entering IT hardware manufacturing with plans for a new facility in Chennai.

- Expanding into industrial and automotive electronics.

- Developing ODM capabilities in smart TVs and refrigerators.

Trends and Themes:

- Shift towards local manufacturing of electronics in India.

- Growing demand for smartphones and IT hardware.

- Increasing focus on exports, especially in the mobile segment.

- Development of the component ecosystem in India.

Industry Tailwinds:

- Government support through PLI schemes for electronics manufacturing.

- Global companies looking to diversify manufacturing beyond China.

- Growing domestic demand for electronics products.

- Push for exports from India in electronics sector.

Industry Headwinds:

- Slow growth in TV and mobile phone volumes in the Indian market.

- Pricing pressures in certain segments like lighting.

- Global supply chain disruptions (e.g., Red Sea crisis affecting freight costs).

Analyst Concerns and Management Response:

-

Concern: Sustainability of growth post PLI scheme expiry.

Response: Management expects government to introduce new schemes focusing on value addition and component manufacturing. -

Concern: Margin pressure in mobile manufacturing.

Response: Company focusing on backward integration and component manufacturing to improve margins. -

Concern: Competition in contract manufacturing space.

Response: Dixon differentiating through scale, customer relationships, and expanding into new product categories.

Competitive Landscape:

Dixon is positioning itself as a leader in electronics manufacturing in India, competing with other EMS players. The company is differentiating through scale, diverse product portfolio, and backward integration initiatives.

Guidance and Outlook:

No specific guidance was provided, but management indicated expectations for “extremely aggressive” growth. The mobile segment is expected to reach 45-50 million units annually in the next couple of years.

Capital Allocation Strategy:

The company plans to invest INR 500-600 crores in capex for FY25, focusing on capacity expansion and backward integration initiatives.

Opportunities & Risks:

Opportunities:

- Expansion into IT hardware manufacturing.

- Component ecosystem development.

- Export opportunities, especially in mobile phones.

Risks:

- Dependence on government policies and incentives.

- Intense competition in certain segments.

- Global economic uncertainties affecting demand.

Regulatory Environment:

The regulatory environment remains supportive with PLI schemes. Management expects new schemes focusing on component manufacturing to be introduced in the next 9-12 months.

Customer Sentiment:

Strong customer demand reported across segments, especially in mobile phones and IT hardware. The company is expanding relationships with global brands like Motorola, Xiaomi, and Lenovo.

Top 3 Takeaways:

- Aggressive growth in mobile manufacturing with expansion plans to reach 55-60 million units capacity.

- Strategic focus on backward integration and component ecosystem development to improve margins and create competitive moats.

- Entry into IT hardware manufacturing with potential to become a significant growth driver in the coming years.

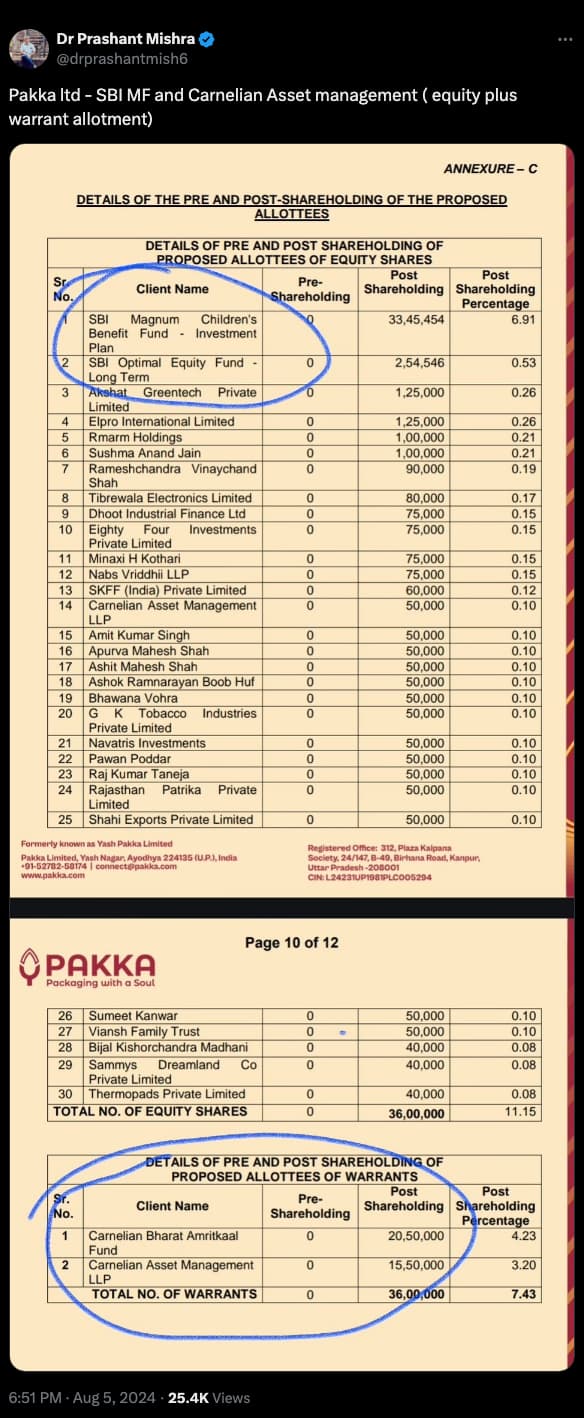

Yash Pakka – (Previously Yash Paper) – Rising from ash (05-08-2024)

I’m just sharing this update from Twitter.

https://x.com/drprashantmish6/status/1820450083235606877

I hope this helps.

Not Invested.

dr.vikas