Posts in category Value Pickr

Sumitomo Chemicals ~ After Excel Crop Care Acquisition (05-08-2024)

Some more random thoughts on Sumitomo:

-

Sumitomo posted strong Q1 results as revenue growth accelerated to 16 %. Operating profits doubled after 5 consecutive quarters of decline. Gross margins, OPM and PAT margins were all at their highest in recent years.

-

Last year, the industry went through a very difficult time and Sumitomo was no exception. But with improved working capital, CFO came in almost at a Rs.800 crore and the cash balance has now swelled to Rs.1500 crore by the end of Q1.

-

At the AGM, the MD said FY23-24 had turbulence kind of which he has never seen in his long career. But now prices are by and large stable, at least they are not falling.

-

The sector seems to have come out of its downcycle and is on the path to recovery as is evident from the results of other domestic focused Ag-Chem companies as well. Monsoon has been benevolent so far, which augurs well for the year ahead.

-

Capacity utilization was lower last year but now stands at 80 to 85 % for technical products and 60 to 65 % for formulation plants. Since business is seasonal, formulation plants are designed for peak seasons and have larger capacities.

-

More than 40 % of the business comes from insecticides and 20 % + from Herbicides. Animal Nutrition was 10 % of revenues last year and will remain in the 7 to 10 % range in the long term, says the management.

-

It has launched 9 new products in the last 18 months. However, the full benefit of this could not be derived last year and these will be ramped up in the current year.

-

Dahej plant will hit full capacity utilization this year while Tarapur will also be set in motion.

-

Currently about 1/3rd of the RM supplies come from China. This will most likely remain as it is and unlikely to reduce any further. Within China, the company is well diversified across regions.

-

The sales target for FY25 is Rs.4000 crore.

-

Biologicals – Sumitomo also has biological products in its portfolio where it distributes products manufactured by Valent Bio-Sciences, an USA based affiliate, in the domestic market.

-

Currently all products are sourced from Valent and there are no plans to manufacture them in India. Presently, this is about 10 % of the business. However, the company wants to expand this significantly as Valent is a global leader in this. In India no one is doing R & D (and therefore manufacturing) in this field, which will give Sumitomo an edge.

-

For the coming year, the company plans to focus on ramping up recently launched products and on introduction of new products which are in the pipeline.

-

The immediate focus is to ramp up volumes from the two newly built plants. In parallel, it is working on medium to long term expansion of the manufacturing capabilities.

-

It has acquired a 50-acre freehold land parcel at Dahej and applied for environmental clearance for the upcoming Dahej site with comprehensive long-term view-point.

-

Glyphosate – The case drags on in court. My feeling is the issue has been consigned to cold storage and the government doesn’t seem keen to push it.

-

R & D – The Company introduced breakthrough technology for oomycetes disease control – Derecho which is a proprietary active ingredient of the parent company and an innovative advance liquid formulation of copper. It has plans to introduce three new patented products in India during the financial year 2024-25. The India R & D team is focussed on producing off-patent products for domestic use and global export. The company has 25+ patents granted across various geographies but their focus is on leveraging SCC Japan’s cutting-edge chemistries and create novel processes and combinations rather than new molecule discovery. The latter task is mainly done by the Japanese parent, who has its own extensive R & D, as well as collaborative agreements with other global majors such Monsanto – Bayer, BASF, DuPont (Corteva Agriscience) etc. Sumitomo Japan has the third highest number of issued patents in the world, after Bayer and BASF. Some of the new products developed by the parent – singly or in collaboration with others – in recent years include Indiflin, Oxazosulfyl, Pyridaclometyl, Pavecto, Rapidicil, Mandestrobin, and Accede. Considerable consolidation has happened in the industry globally in recent years, which works to the advantage of larger incumbents. As an industry size, ag-chem is smaller than Pharma, with lower revenues and lower R & D budgets. Future growth in the industry will come from biorationals, which is growing faster than traditional products.

-

Barrix – SCIL acquired 85 % stake in Barrix this year. It offers environment-friendly innovative pheromone traps, chromatic sheets, bio-stimulants, and plant nutrients suited for multiple crops. SCIL has infused about another Rs.20 crores in Barrix presently which is enough for 2-3 years at least. In fact, it is expected that Barrix may turn cash positive this year itself, hence no further funding will be required. Barrix products are going global as SCIL is in discussion with its affiliates for the same. Group executives from Japan and USA have visited Barrix facilities in India.

-

Drones – The Company has obtained drone application registrations for some products and endeavours to add more products for drone application. The first drone used in India was with a SCIL product for which the company collaborated with government officials for a long period. The products used in drone application are mostly the same, no new products specifically for drone-based application are required to be developed. However, they do not plan to have any drone-based service or start a new vertical. Management says drones will become a commodity soon.

-

Electronic Chemicals – This is the big thing IF it comes through, and possibly the main thing why the stock shot up more than a hundred rupees in a short span of time last month. The management says they have connected with I.T. Chemicals team of Tokyo, given them data basis which they will decide whether to come to India.

(Disc.: Holding)

Forensics and the art of triangulation (05-08-2024)

Thank you aadhar. Please track race eco as well.

Deep Industries (DIL) (05-08-2024)

(post deleted by author)

Burger King ~ Whopper of an Opportunity (05-08-2024)

Right now the number of BK cafes are around 351 and are doing ADS of 14K-15K which is 12 – 12.5% of BK store and most of them have been opened in the last 2 years. I feel the overall contribution from BK cafe is still less. Bulk of this SSG has come from BK store only.

Also gross margins in cafe is in north of +70-75% and management claims to double the ADS from the current 14-15K to 30K. Till now the execution of the management is good.

Journey and Portfolio of a goal-based NEEV investor (05-08-2024)

I agree. Hence, I track this QoQ and subsequent management narrative around the same.

My primary bet on TITAN is its staying power in a tough competitive environment (like it has done in the past), thus elongating its terminal value in decades to come.

Also, it goes with my investment philosophy of BUY, HOLD $ TRACK ![]()

Forensics and the art of triangulation (05-08-2024)

Hello,

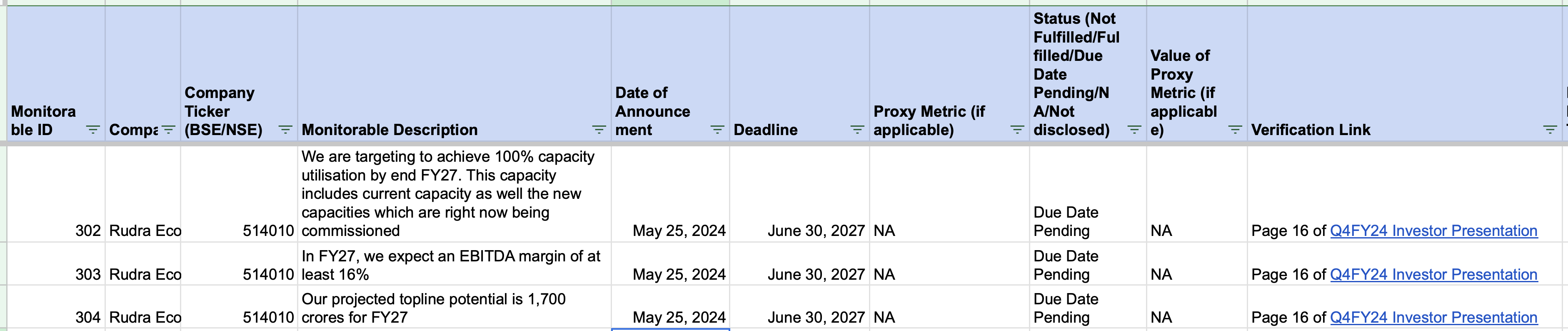

In the below tracker, I have started tracking important company goals for Rudra Ecovation. These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

- Company Ticker: For identifying the company

- Monitorable Description: Description of the goal or metric being tracked

- Date of Announcement: When the monitorable was announced

- Deadline: Target date for achieving the monitorable

- Status: Current progress (e.g., Not Fulfilled, Pending)

- Verification Link: A link to see where I got the information about the goal.

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables-8.xlsx (137.2 KB)

cc @bpraveen02

Cera SanitaryWare Ltd (05-08-2024)

The company intends to buyback up to 1.08 lakh equity shares of the company or 0.83% of the total paid up equity share capital for a total sum of ₹130 crore. Record date for the buyback has been fixed as August 16, 2024.

Price for the buyback has been fixed at ₹12,000 per share