saw this on linkedin. Good to see basilic hiring , inspite of adding 300 employees in one of us acquisiton. looks like they are posied for growth.

Disc- Invested

saw this on linkedin. Good to see basilic hiring , inspite of adding 300 employees in one of us acquisiton. looks like they are posied for growth.

Disc- Invested

Thanks Dharmesh for sharing it. Out of curiosity, what are the factors that you think would help BFS double there revenue in next 2 years?

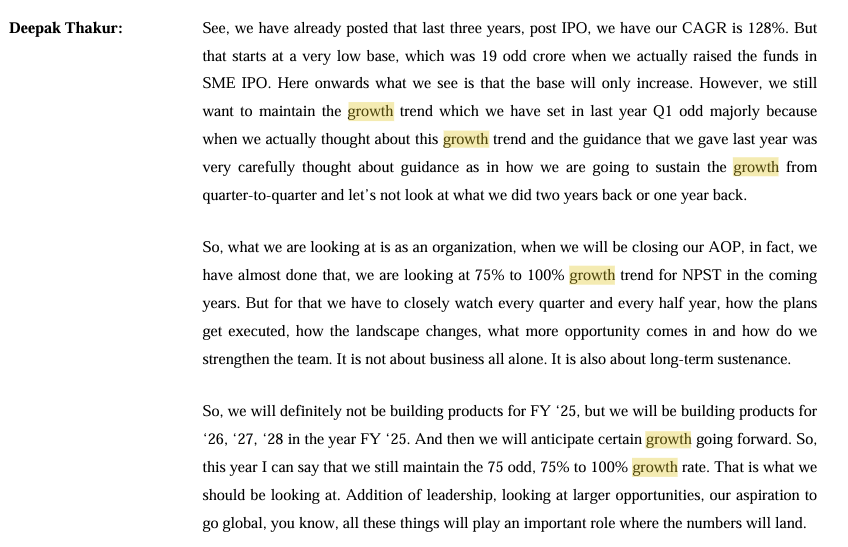

Guidance given post FY24 below. Had guided for 75-100% growth for FY25

Comment post 1QFY25 results

1QFY25 revenue growth was 145% YoY and > 200% YoY on profits

Q1FY25 results and concall highlights –

Have 5 brands in excess of 100cr and 12 brands in 50-100cr range.

Eris is now top 20 companies in the market. Have gained 9 ranks since IPO.

Market growth of 8.1% and we grew at 12.7% in Q1.

Gross margin at 86% up 300bps, Ebitda margin for Q1 at 39% up 189bps on YoY for base business.

Guidance for FY25 – revenue growth of 12-14% and margin of 37% for the base business

Biocon Nephro and Onco business acquired in Nov – Q1 revenue growth of 16%, Gross margin up from 50% to 65%, Ebitda margin up from 19% to 39%. Guidance for the year – 125cr revenue which is a 25% growth and 36% margin.

Biocon Injectable business – Gross margin at 40%. Expect a 10% improvement in margin going forward. Expect a growth of 28% to 480cr.

Swiss Parenterals – Guidance of 330cr Sales and 115cr ebitda a growth of 13-14% in sales and 30% in ebitda. Started manufacturing key Biocon Critical Care products and Eris products. Have done multiple regulatory inspections and qualifications. Have filed multiple products. Geared up for future growth.

New acquisition of biosimilar fill finish lab of Biocon for 105cr. This will reduce time to market by 24 months. Key stepping stone for Biotek business. They have capacity for liquid vials and we will add cartridges and pre-filled syringes. This facility will make us GLP-1 ready. Will help improve margins for our insulin business of 1000bps.

Overall expect Sales of 2600cr with Ebitda margin of 36% for branded business and consol revenue of 3000cr with Swiss parental with margin of 35%.

Debt should reach 2500cr by end of FY25 and 2000cr by end of FY26.

MR strength at 3700+. 560 reps added through Biocon acquisitions.

Disclosure: invested.

Been tracking this company for quite long, been in and out and currently having a tacking position. I still could not figure out the business model of this co.

In the last 2 years, from Q1FY23 to Q1F25 – it has won 105 deals, and went live on 109, with 18 of them at least over 50Cr per deal. That is atleast 900 Cr of new revenue, which should have shown up somewhere?

If we take all the 62 of the destiny deals won in the last 8 qtrs, that should add up to atleast 2300 – 2500 Cr of incremental revenue. At the same time, when we look at the license lined revenues, it has only gone up from 281 Cr in Q1FY23 to 312 Cr in Q1FY25.

Even if we discount the loss of GEM project, doesn’t seem like all these new deal wins are actually translating into the platform or license revenues or AMCs. The AMC was 81 Cr in Q1FY23 and just 121Cr now. The GEM deal was mostly platform deal, as the platform revenues have gone down substantially, from 144Cr in Q2FY24 to 66Cr in Q1FY25.

On an avg, 50% of revenues are license linked, so what’s the remaining revenues? This ratio of license linked vs. others has remained mostly constant for the last 8 qtrs. The SG&A expenses are almost half of the license linked revenues in the last 8 qtrs. The Software Dev expense is mostly constant for the last 8 qtrs.

The investment thesis was that as they sell more of these deals, recurring revenues will increase, cost will remain constant and profits will zoom. Doesn’t look like anything like that is happening. Management guidance for FY25 is 15%-20%, which seems like more of the same. From the numbers, it seems like they need to keep selling these deals just keep the lights on. Would appreciate your thoughts. Thanks.

That is, when it was Kintech Renewables. FY23-24 will be the first annual report as SG Mart

Then I have missed it, to be honest.

I’m not that particular for these developments every Qtr for Invit & REITS. Thank you for highlighting this.

But I’ll still hold same view for 3-4 qtrs or if mgmt gives clear sign, payout will be difficult. It could be trigger in fact for promoter to then sell assets.

INDIGRID has already uploaded investors ppt and also completed the investors call.

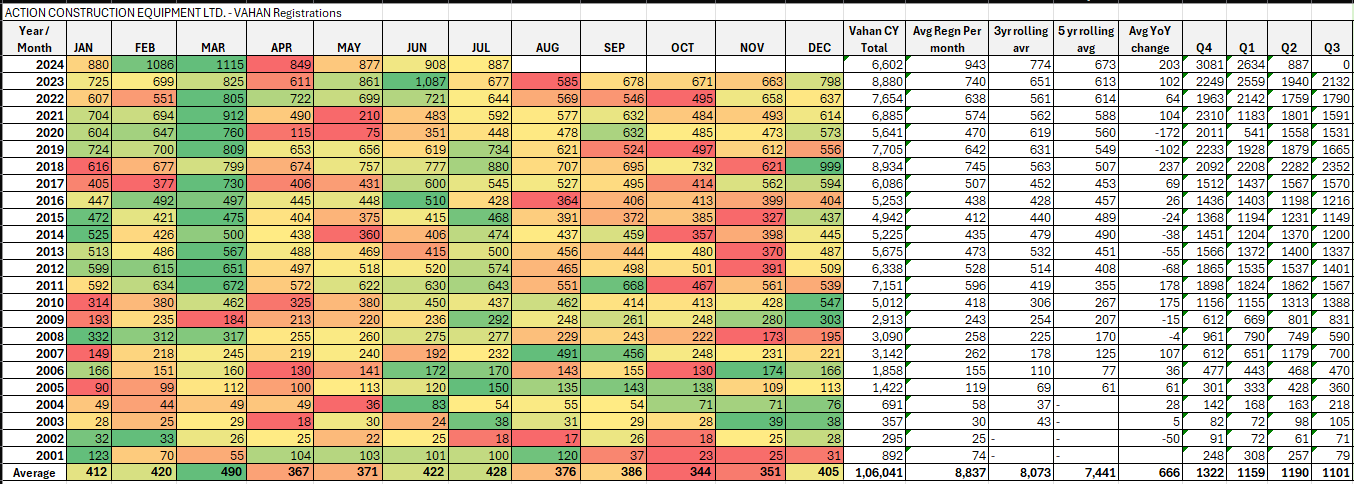

July End VAHAN Regn Numbers for ACE –