A lot of folks have written to ask if they should send in the stock pitches. By default, please do share stock pitches.

Posts in category Value Pickr

Arman Financial Services Ltd (02-08-2024)

Thank you Vinay ji. The promotor holding have gone down substantially to me that is a bit of more of the problem. the promotors have voted with their money. It might have gone down a little bit but long term is much more important. The valuation are undemanding so I am guessing even a less of growth would be okay if promotors are still committed Any thoughts about that? Regards

Sai Silks (Kalamandir) – only listed player in the organized saree market (02-08-2024)

May 2024 Concall Notes

Management Views on Business

- Management optimistic about company’s growth and strategic focus

- Company aims to open additional store capacity of close to 90,000 square feet mainly in Tamil Nadu

- Belief in selling experiences and expanding retail footprint in ethnic retail market in India, particularly in Tamil Nadu

- Focus on improving cash flow conversions by reducing liabilities and negotiating better cash discounts in markets

Financial Performance:

- Revenue for Q4 FY’24 was INR 359.6 crores, compared to INR 323 crores in the previous year.

- Gross margin improved to 40.97% from 39.77%.

- PAT for the quarter stood at 28.73, a growth of 41.95% compared to the previous year.

- Full year PAT was 100.87, a growth of 3.36% compared to the previous year.

- Inventory write-off around 1% annually.

- Planning to declare inventory write-off as a separate line item.

- Store closures not mentioned.

- Revenue contribution: Varamahalakshmi (42%), KLM (38%), Kalamandir (16%), Mandir (4%).

- Store level margins: Varamahalakshmi (33-34%), KLM (24-25%).

Operational Highlights:

- Added three new stores in Q4, totaling 22,750 square feet of retail area.

- Upgraded one store from Kalamandir format to Varamahalakshmi format.

- Planning to open additional store capacity of around 90,000 square feet in the current financial year.

- Active customer base stands at 6.5 million with a focus on expanding in Tamil Nadu.

- Completed integration of Salesforce with the ERP system for digital marketing campaigns.

Cash Flow Management:

- Negative operating cash flow in the current year due to a focus on improving the balance sheet by reducing liabilities.

- Reduction in creditors’ levels to improve margins in the coming years.

- Utilizing IPO funds for investing activities in the current and next year.

Expansion and Growth Strategies

- Opening 13 Varamahalakshmi stores this year with larger store sizes in cash-rich centers

- Targeting positive Same Store Sales Growth (SSSG) of 2-3% and improving EBITDA margin

- Expansion into Tamil Nadu market with Varamahalakshmi stores

- Majority of customers purchasing for weddings, with a younger generation increasing in Indian census data

Marketing and Sales Strategies

- Increasing digital platform usage for marketing, including influencer collaborations on social media and e-commerce

- Doubling digital ad spends while reducing offline spends on newspapers and television

- Store inaugurations blend offline and online marketing efforts with influencers, celebrities, and social media content creation

Inventory and Operations

- High inventory levels due to industry’s requirement for high throughput

- Efficiencies in inventory management pursued through sarees and cluster inventory management

- Expectation of improved inventory turnaround in the coming quarters

SSG Growth

- SSG growth for the last quarter was 3%, with a target to maintain this level.

- SSG for the full year of FY ’24 was -6%.

Customer Behavior

- Repeat purchase is tracked over a trailing 12-month period using a unique phone number for each customer.

- Customer profiling is done to understand purchase behavior and preferences.

- Customers often purchase sarees in groups for various events, not just weddings.

Product Mix:

- 70% revenue from sarees.

- Pure silk sarees contribute over 25%.

- Other products include women’s lehengas, kurta, kurtis, men’s occasion wear, kids occasion wear, and accessories.

- Men and kids wear contribute around 15-18% of revenue.

Future Outlook:

- Optimistic about the company’s growth potential.

- Strategic store expansion to capture market share.

- Focus on improving inventory management and reducing costs.

- Utilizing technology for targeted marketing and customer engagement.

- Confident in the long-term relevance of saree wearing, especially in South India for weddings and occasions.

- Prepared to adapt the product mix and marketing strategies as the market evolves, including a focus on digital platforms and influencer marketing.

Companies with 20%+ growth guidance for next few years (02-08-2024)

(post deleted by author)

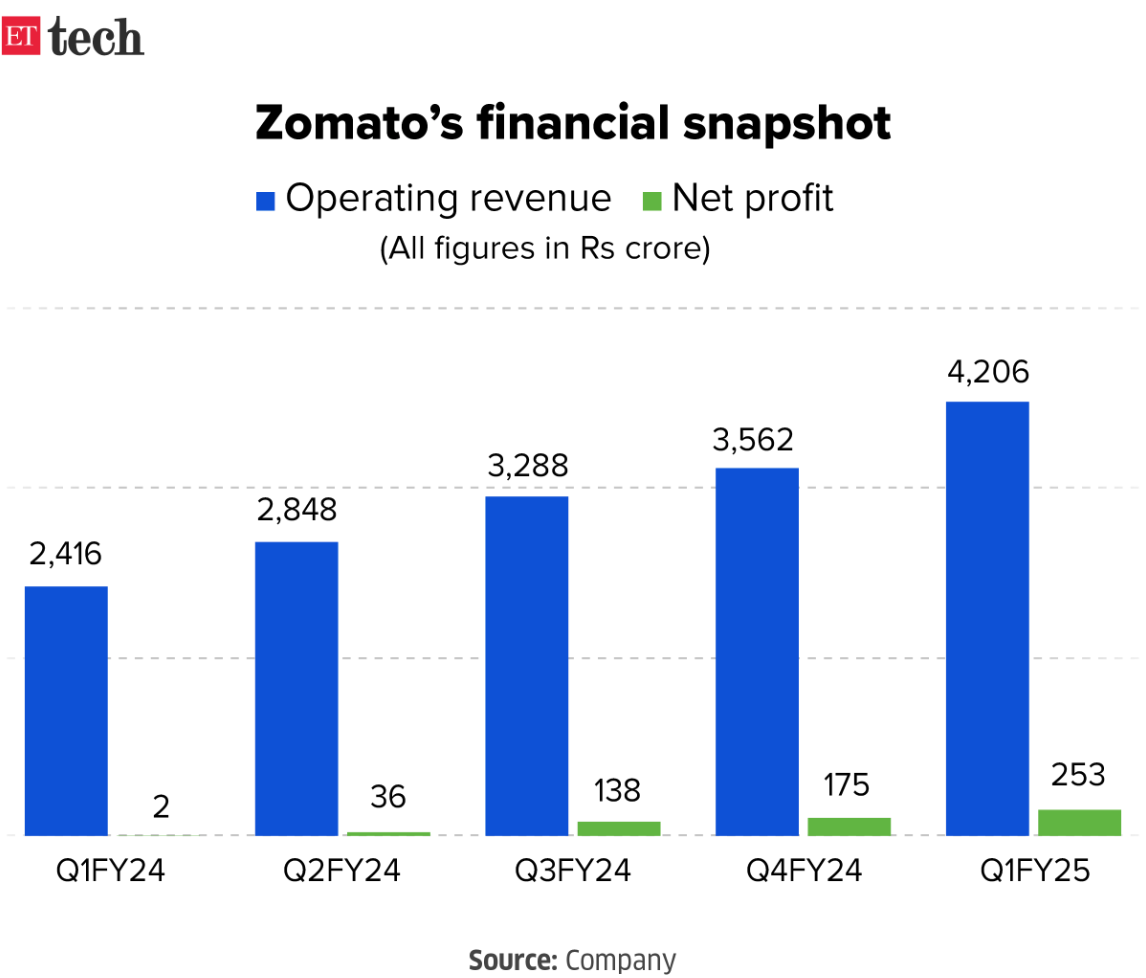

Zomato – Should you order? (02-08-2024)

If their EBIDTA is 3500-4500 (3600 is what I am getting based on the numbers I shared above) Cr then the current 2-year forward PE comes between 52-67.

Do you think that’s justified?

Trent — A value unlocking story from the house of TATA (02-08-2024)

Is the above generated using AI?

Spandana Sphoorty Financial Limited – An Efficient Player (02-08-2024)

How does the community think about Q1 results? Largely, MF companies are a bit struggling with elevated credit costs after a very good run. Not sure whether its a short term blip or may take sometime to stabilize. Any views?

Indiabulls Housing – A compounder from here? (02-08-2024)

No impact. Prudent exercise by management to create confidence in Foreign investors on repayment assurance.

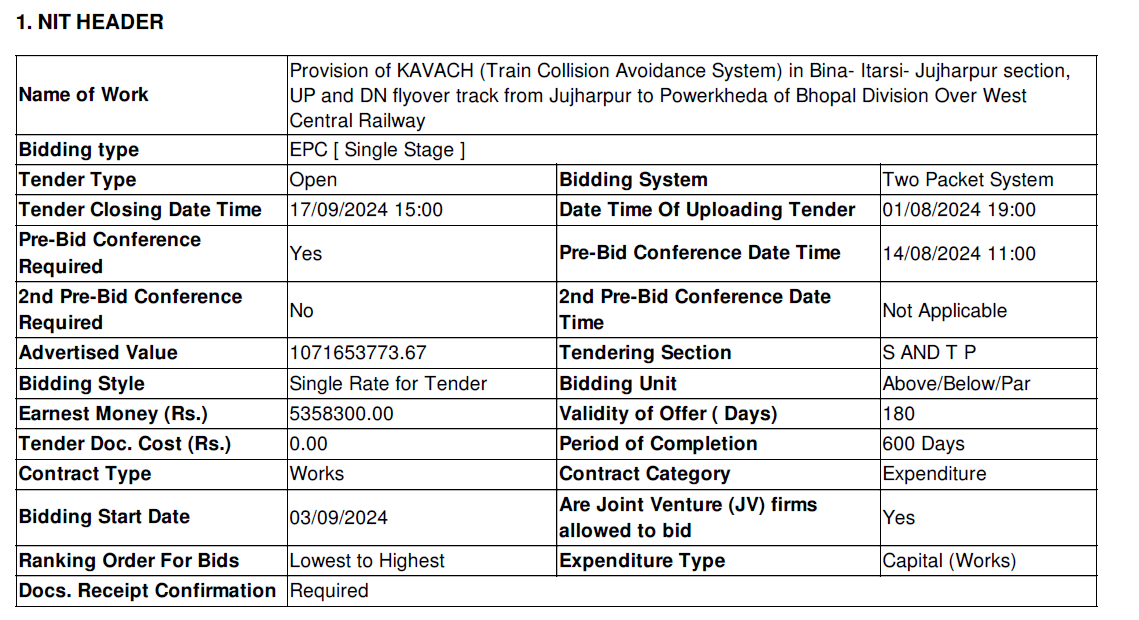

HBL Power: Signs of change (02-08-2024)

One more tender is out, 3rd one so far