What has led to almost doubling of share price in the last 2 months?

Posts in category Value Pickr

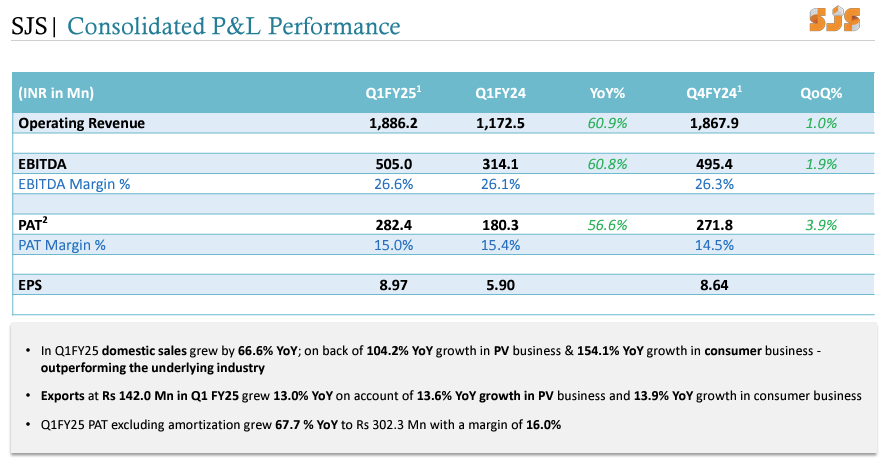

SJS Enterprises Ltd (01-08-2024)

Superb results

Conservatively extrapolating 1QFY25 to FY25 implies EPS of Rs 36/share implying share trades at 23.6x FY25E

Disclosure: Invested

Zomato – Should you order? (01-08-2024)

Any thoughts on the results?

The story is going Zomato’s way, they are able to show the growth and EBITDA growth and the bull market is rewarding them for it. I am starting to worry about the valuation, it is at a PE of 384.

I did some basic maths and here is the summary:

| Revenue | |||||

|---|---|---|---|---|---|

| Zomato | Blink it | Going out | B2B | ||

| 2024 | ₹32,224 | ₹12,469 | ₹3,225 | ₹3,172 | ₹51,090 |

| 2025 | ₹38,669 | ₹19,950 | ₹6,450 | ₹6,344 | ₹71,413 |

| 2025 | ₹46,403 | ₹31,921 | ₹12,900 | ₹12,688 | ₹103,911 |

| Adjusted EBITDA | |||||

| Zomato | Blink it | Going out | B2B | ||

| 2024 | 3.30% | -1% | 0% | -4% | |

| 2025 | 3.70% | 1% | 1% | 0% | |

| 2025 | 4% | 3% | 2% | 4% | |

| Profit at EBIDTA level | |||||

| Zomato | Blink it | Going out | B2B | Total | |

| 2024 | ₹1,063 | -₹125 | ₹0 | -₹127 | ₹812 |

| 2025 | ₹1,431 | ₹200 | ₹65 | ₹0 | ₹1,695 |

| 2025 | ₹1,856 | ₹958 | ₹258 | ₹508 | ₹3,579 |

Assumptions

- Food delivery grows at 20%, Blink it at 60%, Going out at 100% and B2B at 100%

- All Adjusted EBITDA are assumptions

Now even if PBT (Profit at EBIDTA) grows the above assumptions and 2 year forward PE is around 80. I am trying to get my head around if this is correct and if yes is the valuation is justified.

Dic: Invested and Biased.

Trent — A value unlocking story from the house of TATA (01-08-2024)

The forward P/E ratio is calculated using the formula:

Forward P E=Current Share Price/Projected EPS

I have only Projected the EPS. Mr. market will give price according to market sentiments. I think valuations are within 2-year forwards. When valuations exceed 2-year forwards and start approaching 3-year forwards, I will find myself uncomfortable and perhaps sell. A lower forward P/E ratio may indicate a stock is undervalued relative to its future earnings potential. For Trent Forward P/E are Year 1: 103.93,Year 2: 73.66,Year 3: 52.63,Year 4: 37.56,Year 5: 26.87. It is overvalued at 1 year Forward PE of approx. 104. but I think it OK at 2 Year forward PE of approx. 74. I need to track Quarter to Quarter results and EPS, If they are better than projected then I am OK, but if I see a decline in EPS the will take a call accordingly.

Ranvir’s Portfolio (01-08-2024)

Mankind Pharma –

Q1 concall and results highlights –

Revenues – 2893 vs 2579 cr, up 12 pc

Gross profit – 2081 vs 1759 cr, up 18 pc

Gross margins @ 72 vs 68.3 pc, up 370 Bps

EBITDA – 686 vs 655 cr, up 4 pc ( margins @ 23.5 vs 25.5 pc ). Adjusted for one time M&A related cost, EBITDA would have been 728 cr, margins would have been 25 pc

PAT – 543 vs 494 cr, up 9 pc

Cash on books @ 3750 cr

Domestic sales grew by 9 pc ( growth in domestic business impacted by delayed onset of anti – infective season )

Export sales grew by 62 pc !!!

Domestic : Export sales ratio @ 91 : 9

Chronic : Acute sales ratio @ 39 : 61

Company’s domestic Mkt share share @ 6.1 pc ( second largest after Sun Pharma )

In Q1, Company Acquired Bharat Serums and Vaccines for 13,630 cr. This translates to 22-23 times FY 25 EBITDA that BSV is expected to clock. To be funded by cash on books, debt and Equity ( if required ). Transaction expected to close in 3-4 months

Some brands where BSV enjoys 100 pc Mkt share in India are –

Rhoclone ( Injection – prevents formation of antibodies after a person with Rh-Negetive blood is given a transfusion with Rh-positive blood ) – FY 24 sales @ 180 cr

Thymogam ( immunosuppressant injection )- FY 24 sales @ 32 cr

ASVS ( anti Venom Injection ) – FY 24 sales @ 41 cr

Other dominant brands where BSV is no 1 / 2 in domestic mkt are –

Hucog ( infertility treatment – injectable )- FY 24 sales @ 63 cr

Humog ( supports ovulation – injectable ) – FY 24 sales @ 55 cr

Luprodex ( used in treatment of prostate cancer – injectable ) – FY 24 sales @ 37 cr

Foligraf ( infertility treatment – injectable ) – FY 24 sales @ 35 cr

BSV ltd reported sales of 1723 cr with 28 pc EBITDA margins for FY 24

Company in-licensed Symbicort ( inhaler – for Asthma ) from Astra Zeneca and launched in Q1. Seeing good traction

Also in-licensed Inclisiran ( lipid lowering – injectable ) from Novartis in Q1

Company’s OTC business reported flattish sales @ 206 vs 208 cr. Their popular OTC brands include – GasOFast, PregaNews, ManForce, AcneStar, Unwanted 72, HealthOK

Company’s EBITDA margins in their OTC / Consumer Healthcare business are @ 20 pc

After the acquisition of BSV ltd, company shall emerge as the No 1 player in the Gynae therapeutic segment

Capex for Q1 @ 125 cr

For FY 25, company is guiding for EBITDA margins for 25-26 pc

Company’s EBITDA margins in Q1 did not rise despite the sharp rise in gross margins as the company launched a number of new products in Q1 and there were higher marketing spends in Q1 to support them. These spends should moderate going forward

Company believes that BSV’s business is under – levered and Mankind’s distribution can help improve growth and margins of BSV’s business

The difference in gross margins of Chronic vs Acute business are > 10 pc ( similar figures were given by Alkem Labs in their Q4 or Q3 concall LY … quoting from memory )

Company’s In-Licensed brands give them a foot in door when it comes to high end Hospitals / Clinics / Doctors. These deals do enhance the company’s reputation in a big way + these In-Licensed products are limited competition products

Company believes, it can sustain 70 pc kind of gross margins in the medium term

There will be merger related costs that ll come up in Q2 as well

Company may raise around 3000 cr via equity route to fund the BSV ltd acquisition. At current valuations ( that Mankind trades, I think it makes sense to raise equity )

Confident of accelerating the BSV Ltd’s growth rates to much higher levels due to speciality + complex to make + monopoly products ( under patent ) – that BSV offers

Disc: holding, should do well over medium term ( IMHO ), biased, not SEBI registered, not a buy / sell recommendation

Vasa Denticity aka Dentalkart – The Indian Amazon of Dental supplies ?! (01-08-2024)

Thanks for the scuttlebutt. I will keep it in mind. But this is one reason I have a diversified portfolio of 20 stocks.

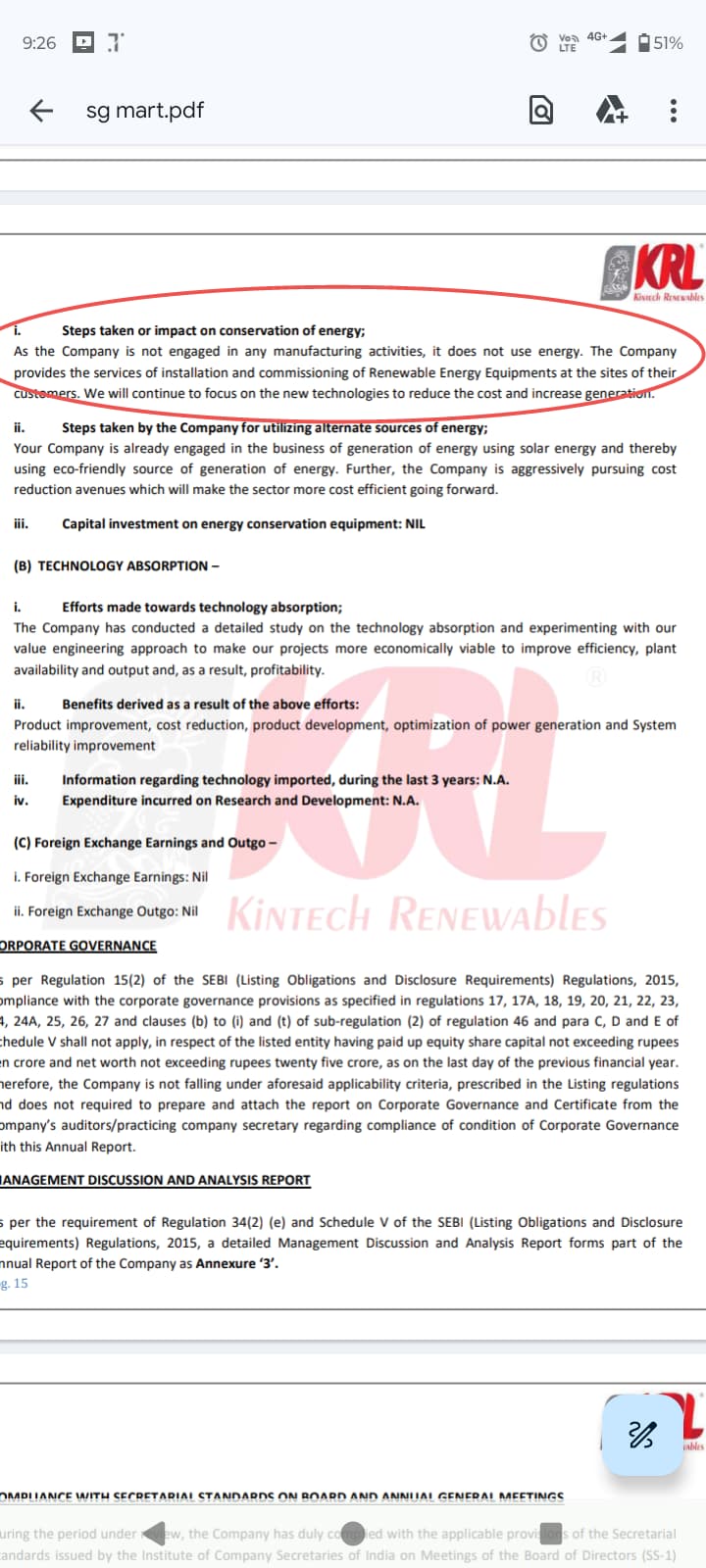

SG Mart- Can it successfully create a marketplace? (01-08-2024)

Is sg mart still operate the business of renewable energy? I found this in there annual report.

Clean Science and Technology Limited (CSTL) – A clean and green future ahead (01-08-2024)

went through concall audio, couple of points to discuss.

- more clarify given on capex in horizon – 30 cr capex for pharma product that will be in market by Q3. 150 Cr for performance segment where novel process is used to make product. product has already competitors but capacity will be 15% of global that is 350 cr and last one is again 150 cr capex but not much product details given but there are already producers of it.

on HALS, basket of all products – after 3 months from now, we should have 150 tons per month. growth was slow as it was single or double product but now we have 5 which helps to convince customer. for this year they said they aspire 2000 tons and from there in 3 years should touch 6000 tons while thier capacity is 10500 tons.

existing products are somehow maintaining volume or registering minor growth. we need to discuss how long clean science will be able to sustain this items, does anyone have more info on Vinti and jhow much it will impact and when?

can anyone throw light about one point in concall where it was told they can accommodate 1000cr capex out of which 300/400 cr worth project is going on (3 capex we talked). from where this capex is coming? This may be addressed but if anyone can throw light please

I feel it will take time but rewards will be also better. I feel small portion of the future HALS growth is already priced in but the moment they start hitting 150-180 tons per month, we should see numbers going upwards which will suddenly trigger price upward. what people think here?

our all bet is on HALS and 2-3 more products coming in but at same time we need to relook at existing set of products and how long this can be sustained or grown.

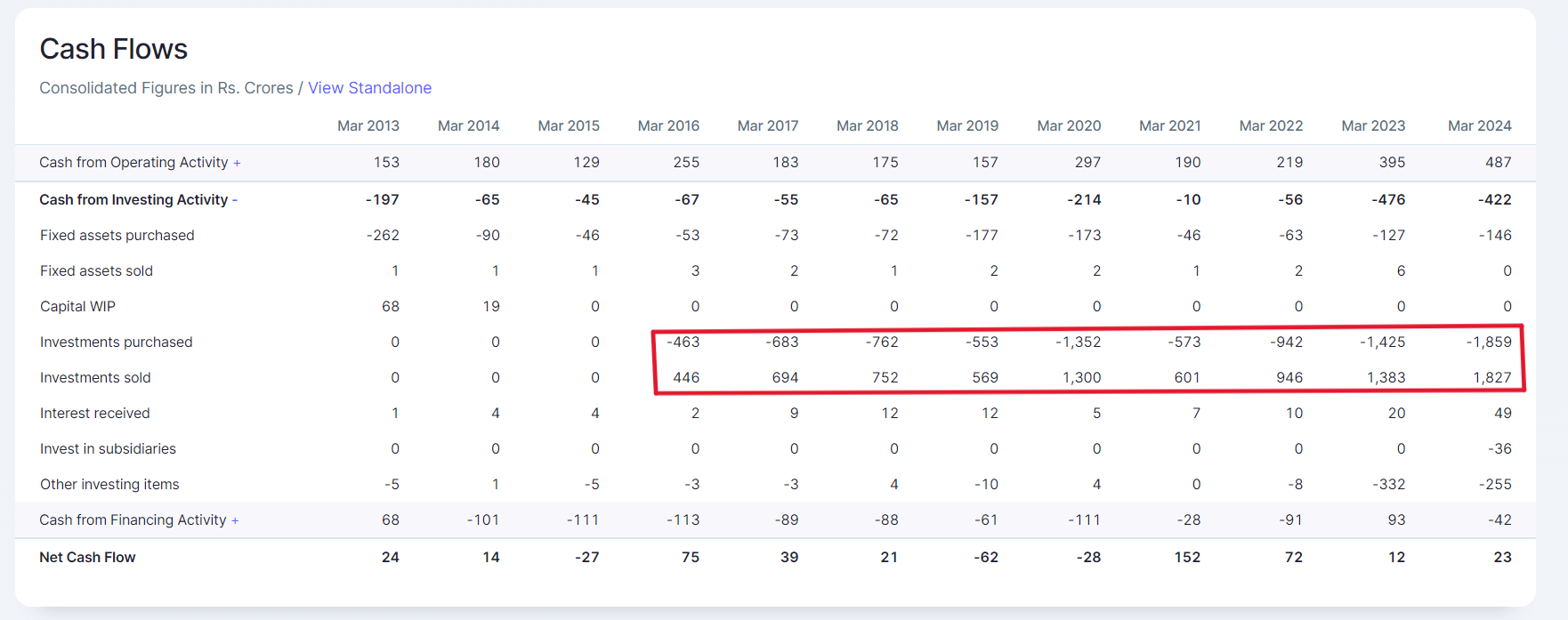

Shriram Pistons & Rings Ltd (01-08-2024)

I have a question regarding SPRL’s cash flow statement. Why company engage a substantial amount in “Investment” and they have been doing it constantly since 2016? And also where this amount of 446 cr came suddenly in 2016. I have tried to find it out in AR but couldn’t able to find any.

Maybe it is a very naive question to ask but I am trying to learn equity analysis and am very new in this field. It would be very helpful for me if anyone could explain this to me.

Vasa Denticity aka Dentalkart – The Indian Amazon of Dental supplies ?! (01-08-2024)

Sir

Talked to one of their distributors. He said these guys are selling virtually at no margins. An mnc has barred its distributors to give material to the company because they are undercutting on a hot selling product to be in limelight.