In the forward PE calculation, it seems that you have assumed same price of 5835? correct me if i am wrong. Is that based on your experience with other stocks ? Do you mean this price will stay there even if there is a consistent growth till PE comes to down to certain level?

Posts in category Value Pickr

Vasa Denticity aka Dentalkart – The Indian Amazon of Dental supplies ?! (01-08-2024)

They have the first mover’s advantage. Right now the dental supply industry is very unorganized.

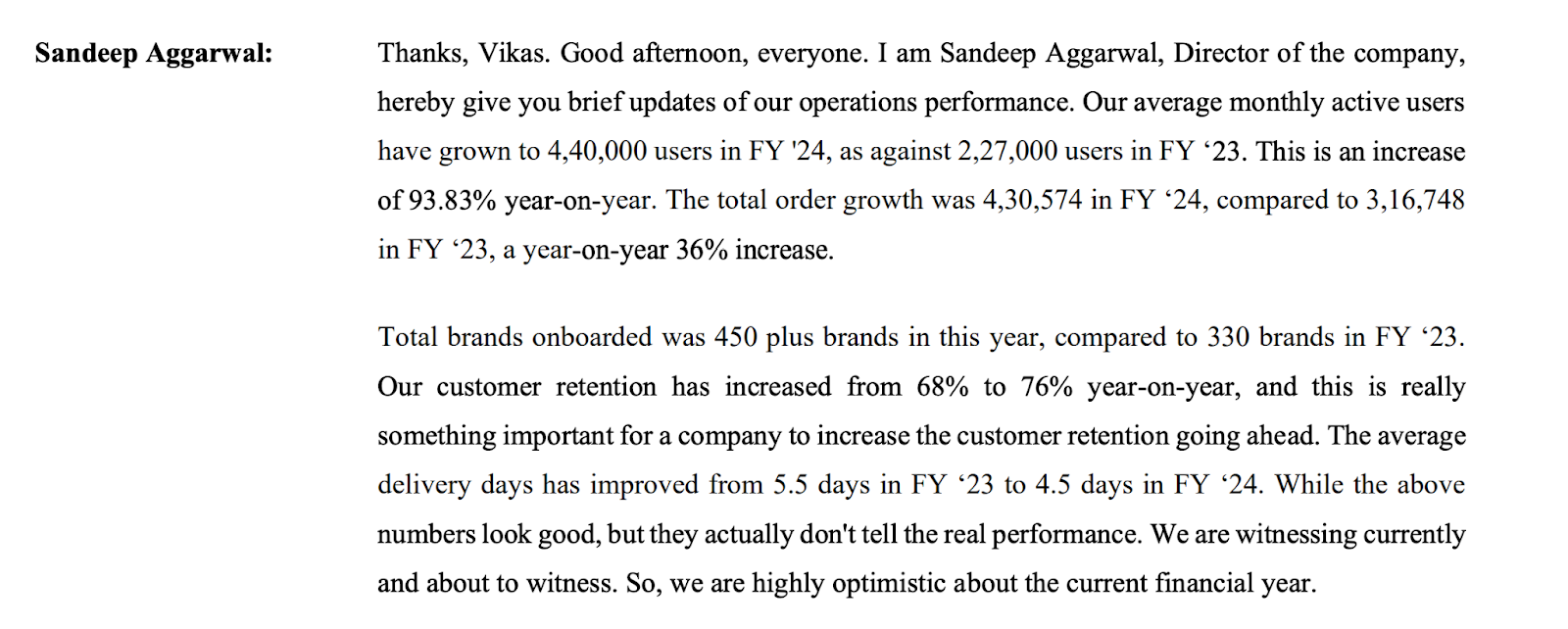

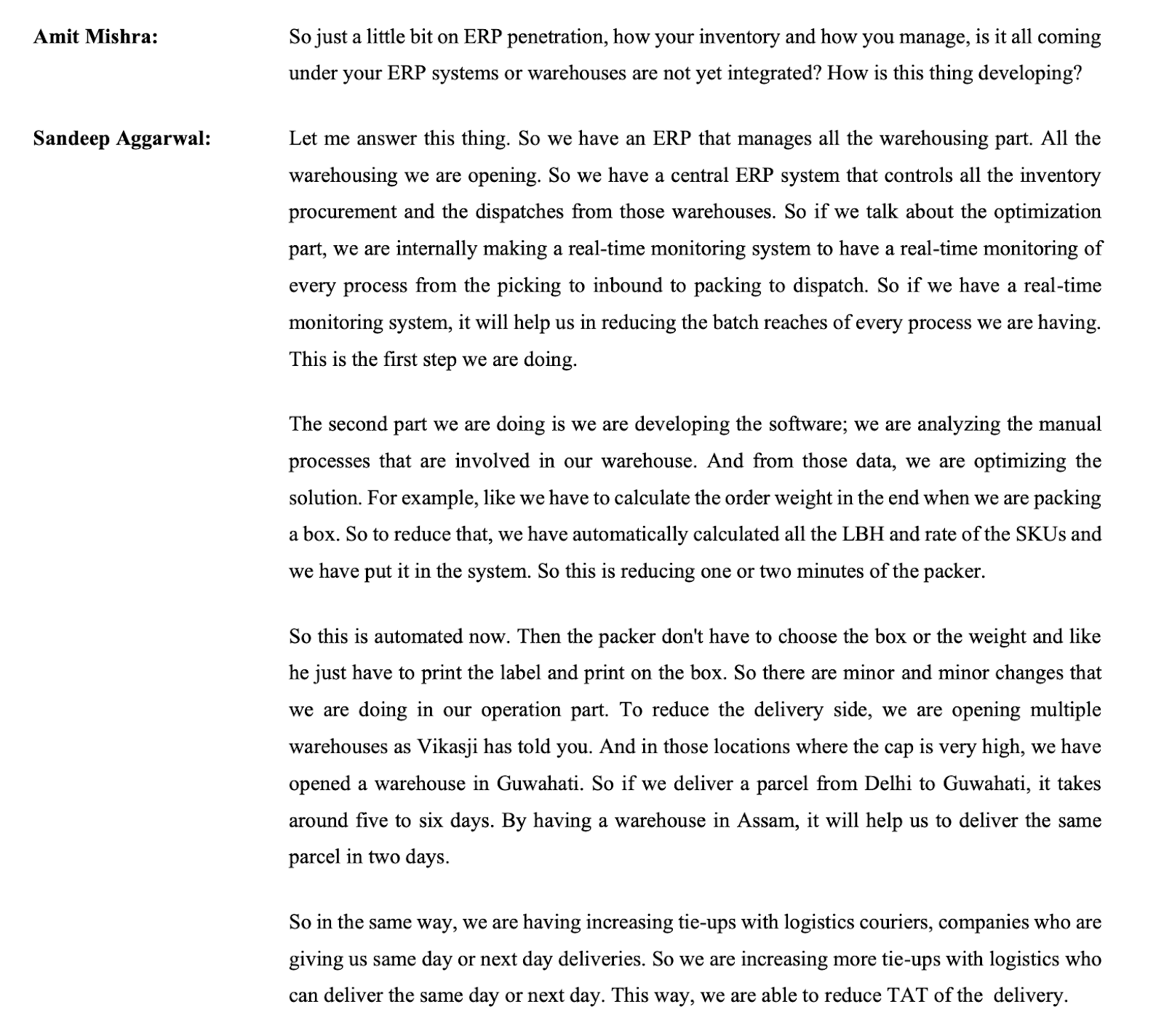

Please go through their concall transcript to get more clarity. I am attaching few snapshots from their concalls below.

For new players to enter, compete and capture the market is not going to be easy.

It has already become kind of Amazon / Flipkart of dental supplies in India. Yes. Some big player can enter. But the market size is not that much massive and very niche segment. The amount of cash the new entrant has to burn will be humongous.

Again personal opinion.

Aditya Birla Capital – A complete Financial Inclusion (01-08-2024)

Results are down q on q, it seems it is a consistent theme in this quarter among all lenders, those who were growing aggressively are all down q on q, does this happen in every election quarter or MSME loans go down in monsoon or something else? Does anyone has any idea?

Vasa Denticity aka Dentalkart – The Indian Amazon of Dental supplies ?! (01-08-2024)

The company does not have any moat I suppose. They sell dental products, which is a standardized. Of course they have first mover advantage, and they are getting decent numbers too. But certainly this ROE will attract more competition as the business is easy… You have to sell a few hundred standardized products on an e-commerce site.

Lately I saw their cash flow statement which is alarming. Even receivables have gone up substantially… Looks like they are pushing sales.

Need to examine this aspect.

Bull therapy 101-thread for technical analysis with the fundamentals (01-08-2024)

Vesuvius India Ltd:

Technicals:

Weekly chart: Ongoing continuation pattern (symmetrical triangular) above 50DEMA after a sharp upmove of ~75% (2400 Points) in ~1months time. Post consolidation, my understanding from the technical setup is that the price will rally upwards for another 2400 points atleast.

Fundamental factors why the price is likely to go up:

- Starting 2022 (assumption), announced a 500 Cr. capex plan over next 3~5 Yrs.

- 100Cr. for expansion [Phase IV expansion completed of the Kolkata plant (Completed: Dec 2022) & Phase I expansion completed of the Visakhapatnam precast plant ( Completed: March 2023)]

- ~70Cr. Purchase of 22 acres at Parwada (Visakhapatnam) for building an industrial complex named Visakha [Completed: June 2022]

- ~90Cr. for Construction of the Basic Monolithics and Mould Flux (import substitute) plants commenced at the Visakha Industrial Complex [Commissioned: Jun 2024 —–> Started: March 2023]

- ~90Cr. Construction of the AlSi Monolithic plant commenced at Visakha Industrial Complex [expected commissioning in Q4FY24—–> Started: Nov 2023]

- 17-Apr-2024: Increased the capex outlay to ~1000Cr. Netting the amount mentioned under point 1, yet to hear additional plans for the rest of the amount (650Cr.) Current Fixed Assets alongwith the CWIP is ~500Cr. .

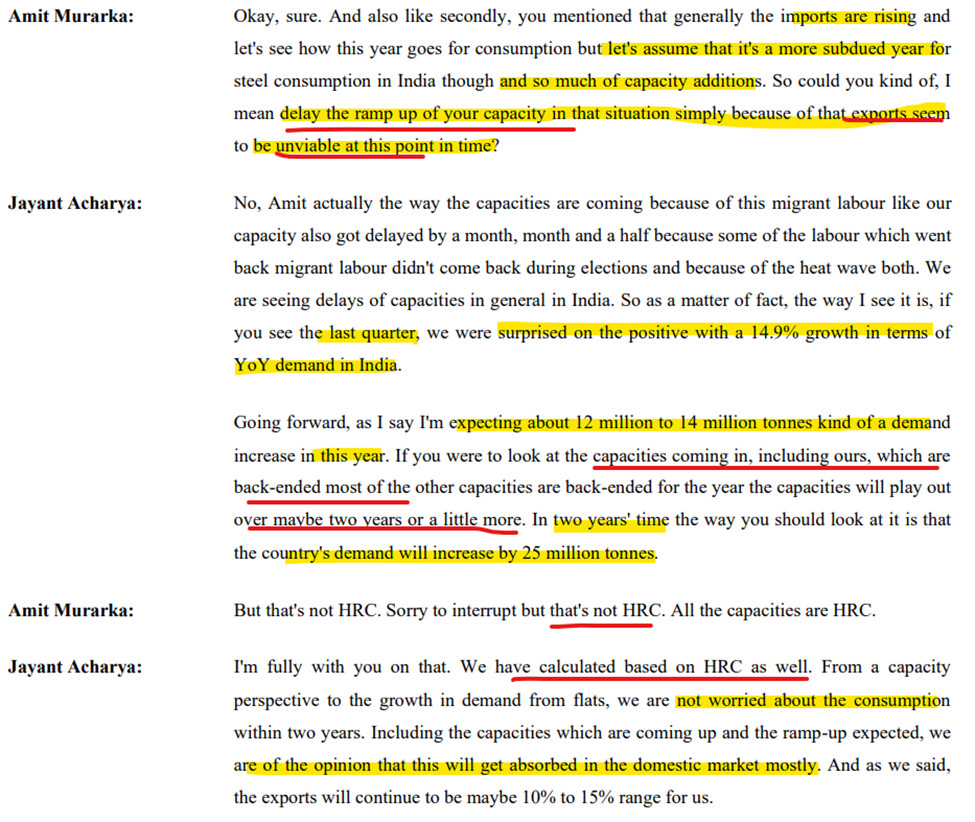

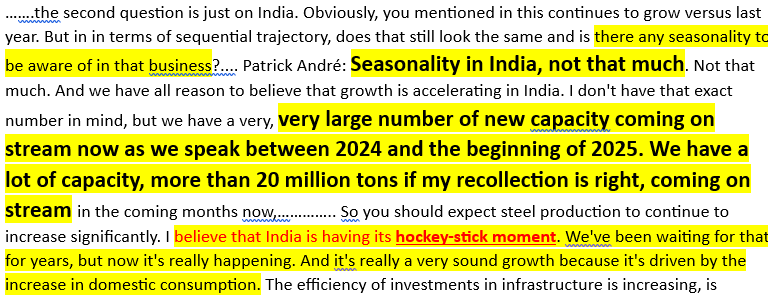

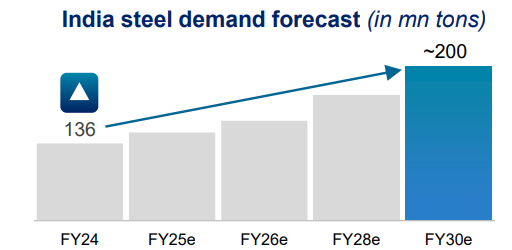

- Business mainy caters to dometic demans, particularly 3 major customers (Major Risk). Slowdown in Steel Industry will impact the business. As of now, both the major listed steel players (Tata Steel and JSW steel) sound bullish on the outlook of their business and doing capex to further increse their capacities.

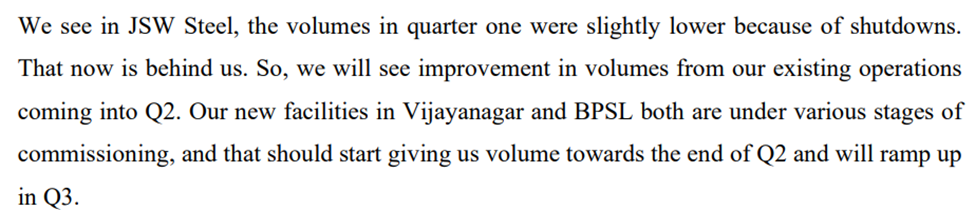

JSW Steel Q1FY25 Transcript snippet (Link):

Parent Vesuvius Analyst meet Commentary (15-May-2024: Link):

Tata Steel Q1FY25 presentation snippets(Link):

Key Point1:

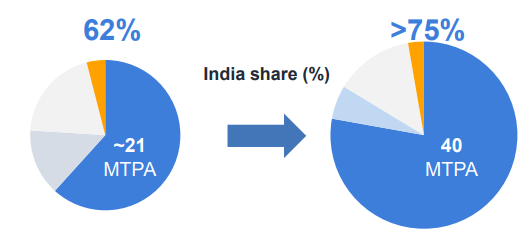

Key Point2: Tata Steel is scaling up (from 21MTPA to 40MTPA by 2030) in India to capitalise on growth opportunity.

Key Point3:

Disc: Added to the existing position in the last 30 days. Shared for learning purpose from the like minded folks. I am novice and not an investment advisor. Please do your due diligence.

Bull therapy 101-thread for technical analysis with the fundamentals (01-08-2024)

Vesuvius India Ltd:

Technicals:

Weekly chart: Ongoing continuation pattern (symmetrical triangular) above 50DEMA after a sharp upmove of ~75% (2400 Points) in ~1months time. Post consolidation, my understanding from the technical setup is that the price will rally upwards for another 2400 points atleast.

Fundamental factors why the price is likely to go up:

- Starting 2022 (assumption), announced a 500 Cr. capex plan over next 3~5 Yrs.

- 100Cr. for expansion [Phase IV expansion completed of the Kolkata plant (Completed: Dec 2022) & Phase I expansion completed of the Visakhapatnam precast plant ( Completed: March 2023)]

- ~70Cr. Purchase of 22 acres at Parwada (Visakhapatnam) for building an industrial complex named Visakha [Completed: June 2022]

- ~90Cr. for Construction of the Basic Monolithics and Mould Flux (import substitute) plants commenced at the Visakha Industrial Complex [Commissioned: Jun 2024 —–> Started: March 2023]

- ~90Cr. Construction of the AlSi Monolithic plant commenced at Visakha Industrial Complex [expected commissioning in Q4FY24—–> Started: Nov 2023]

- 17-Apr-2024: Increased the capex outlay to ~1000Cr. Netting the amount mentioned under point 1, yet to hear additional plans for the rest of the amount (650Cr.) Current Fixed Assets alongwith the CWIP is ~500Cr. .

- Business mainy caters to dometic demans, particularly 3 major customers (Major Risk). Slowdown in Steel Industry will impact the business. As of now, both the major listed steel players (Tata Steel and JSW steel) sound bullish on the outlook of their business and doing capex to further increse their capacities.

JSW Steel Q1FY25 Transcript snippet (Link):

Parent Vesuvius Analyst meet Commentary (15-May-2024: Link):

Tata Steel Q1FY25 presentation snippets(Link):

Key Point1:

Key Point2: Tata Steel is scaling up (from 21MTPA to 40MTPA by 2030) in India to capitalise on growth opportunity.

Key Point3:

Disc: Added to the existing position in the last 30 days. Shared for learning purpose from the like minded folks. I am novice and not an investment advisor. Please do your due diligence.

Vasa Denticity aka Dentalkart – The Indian Amazon of Dental supplies ?! (01-08-2024)

What is the economic Moat in this company? Can it maintain it’s ROE levels with new players entering this space with significant capital

Matrimony.com Ltd – Lot of opportunity to grow (01-08-2024)

Can’t seem to figure why the sudden 15-20% upmove in the last week or so . Volumes have been good also . Seems someone is accumulating the stock .

Punjab Chemicals & Crop Protection Limited (PCCPL) A Clear Runway Ahead! (01-08-2024)

Can see a good uptick in Sales and an even better PAT performance QoQ. Inventory expense also seems to be have come down by a big margin this quarter. Would be interesting to hear management commentary (or even from @harsh.beria93 ![]() ) about industry headwinds, china dumping and export prospects.

) about industry headwinds, china dumping and export prospects.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/0b49aba1-fdbb-449f-9987-3594f4c23726.pdf

Red Tape Ltd. – The next fashion giant? (01-08-2024)

Thanks for this.

Were you able to get any insights about per store economics, specially the franchise owned stores, and about RedTape’s commissions?