Good numbers YoY during Election Year, Monsoon Season. Expect better peformance in coming qtrs. Awaiting concall for tomorrow. Might get update on KATO WORKS:

Posts in category Value Pickr

Companies with 20%+ growth guidance for next few years (31-07-2024)

Growth has been good and company is mainting healthy balance sheet. but they have not given future giudance or there long term targets. can put small amount and track story and gradually increase investment.

P.s. just googled and saw reviews. mostly given 1 star by most users. overpriced and not up to the mark service.

Tata Consumer Products Limited (TATACONSUM) (31-07-2024)

- Yes you can apply for 50 and even more.

- Yes you will surely get 5.

- Not possible.

The right entitlement that will be invoked or sold by other shareholders will be distributed among other shareholders who apply for more shares.

Fredun Pharmaceuticals – A good microcap with great potential? (31-07-2024)

Where is this clipping from? I am looking for quarterly reports and concalls from the company.

Fredun Pharmaceuticals – A good microcap with great potential? (31-07-2024)

I recently started tracking Fredun after it showed up in one of my screeners.

What bothers me the most is the lack of disclosures in terms of quarterly reports or earning concalls. I checked the company’s investor relations but found only outdated material. Latest one available is > 1 year old.

How is this forum tracking the company?

Pls guide.

Thanks

Aurum Proptech (Majesco) (31-07-2024)

Could you please explain your calculation of this arbitrage? Also, on screener current market cap to sales is showing 2.1. However, the TTM sales ia at 235cr and market cap is at 1015cr. If someone could help me out with this?

IDFC First Bank Limited (31-07-2024)

I don’t think it’s an act of attacking the guy after a quarter or two of bad performance. I can assure you that I have been very patient. However, this is definitely a case of ‘the straw that broke the camel’s back.’ Maybe your “back” is stronger than mine (just joking). For me, the last straw was the FY27 cost-to-income ratio at 65%.

You may think I’m obsessed with the cost-to-income ratio from my first post. Let me explain. To set the groundwork, bear with me as I give a brief explanation of how a bank works. (Most of you might already know this, but let me explain again to highlight its importance.)

For simplicity, I’m assuming a capital adequacy ratio (CAR) of 10%. (In reality, CAR is around 12%.) Assume I start a bank with Rs 10 as my capital (by issuing 10 shares of Rs 1 each). With the assumed CAR, I can only take Rs 100 as deposits. According to RBI rules, because the CAR is 10%, I cannot accept more than Rs 100 in deposits, even if someone is willing to give me more. This is because if a bank’s capital is Rs 10, it can only take on business risks proportional to Rs 10. This acts as a limit on the loan book and deposits. Naturally, since I have deposits of Rs 100, my loan book will also be Rs 100.

Now, if my bank generates Rs 2.5 as profit after a year of operations (an ROE of 25% because our bank made Rs 2.5 profit on the initial Rs 10 it started with), my capital becomes Rs 12.5. So, in the second year, I can take Rs 125 in deposits, and my loan book will increase to Rs 125.

Conversely, if my bank only makes Rs 1 on Rs 10 (an ROE of 10%), to increase the loan book to Rs 125 for the next year, it has to raise an additional Rs 1.5 from somewhere else (because the bank has Rs 10 initial capital and Rs 1 profit, totaling Rs 11). By issuing Rs 1.5 in new shares, the equity is diluted by 15% (there will now be 11.5 shares instead of 10). In effect, the market capitalization of the bank increases by 15%. If this happens over five years, the original shareholding is diluted by about 50%. This is a significant number.

I’ve seen comments from people wanting Bajaj Finance-like growth. I’m afraid that’s not possible because Bajaj Finance has an ROE of 22-25%. Why? It has a net interest margin (NIM) of around 9% and a cost-to-income ratio of 35-40%. The business builds itself, and there isn’t much need for dilution. That’s when real value creation happens for existing shareholders.

I would recommend everyone read HDFC Bank’s annual reports from 1996 to 2005. You’ll understand what growth means. Even though they had to build new branches, start new business lines, and attract deposits, they had good ROE and grew their book with minimal dilution. That’s when value creation happens for the shareholder.

Now, finally, to explain why I’m so disappointed with IDFC First.

By Q1 FY25, all the issues from the IDFC Bank days are resolved. Their bad loan book is written off, high-cost borrowings are repaid, and most branches have been operational for 2-3 years. The current loan book is entirely created by V Vaidyanathan and his team, with no legacy IDFC issues remaining. There’s good momentum in deposits, and the brand is established.

The bank is now in a position similar to my example of starting a bank with Rs 10 capital. Everything needed has been built over the last five years. So, my assessment now is focused solely on the future, not on what happened since 2018. I will credit them for reaching this stage, but my analysis is only about the future.

If, after three more years, the cost-to-income ratio still remains at 65%, the ROE will likely still be around 10-13%. Now, please calculate the dilution for three years with the bank growing deposits at 25 %.

This is just unacceptable in my view. If IDFC First cannot generate a good ROE from FY25 onwards, shareholders cannot expect good returns. I hope my explanation clarifies why I’m so concerned about the ROE not improving substantially until FY27, which is three years from now.

This is in no way a comment about what tech they are using or how the customers feel about the bank. It is just an investor point of view.

Disclosure: I had a good investment in IDFC Ltd until Q1 FY25. I made good money too. I genuinely wanted them to succeed. Please don’t misunderstand me as being overly negative. I’m just sharing what I’ve learned.

Black Box Ltd. – Riding the data center wave (31-07-2024)

Black Box Ltd, formerly known as AGC Networks, is a global IT services company providing digital solutions and services. It specializes in networking, data centers, cybersecurity, unified communications, and enterprise applications. With a strong presence in multiple countries, Black Box Ltd serves a diverse range of industries, including finance, healthcare, government, and education. The company focuses on delivering innovative technology solutions to help organizations optimize their IT infrastructure and improve operational efficiency.

| Narration | Mar-15 | Mar-16 | Mar-17 | Mar-18 | Mar-19 | Mar-20 | Mar-21 | Mar-22 | Mar-23 | Mar-24 | Trailing | Best Case | Worst Case |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 890.89 | 881.38 | 779.63 | 733.45 | 1,852.74 | 4,993.92 | 4,674.02 | 5,370.17 | 6,287.56 | 6,281.58 | 6,281.58 | 6,281.58 | 6,281.58 |

| Expenses | 866.72 | 875.63 | 747.30 | 700.15 | 1,806.21 | 4,665.51 | 4,309.54 | 5,112.40 | 6,014.39 | 5,855.38 | 5,856.70 | 6,281.58 | 6,281.58 |

| Operating Profit | 24.17 | 5.75 | 32.33 | 33.30 | 46.53 | 328.41 | 364.48 | 257.77 | 273.17 | 426.20 | 424.88 | – | – |

| Other Income | 37.87 | 7.08 | 13.07 | 18.90 | -66.69 | -177.98 | -75.02 | 0.41 | -24.96 | -14.22 | -12.90 | – | – |

| Depreciation | 18.44 | 8.50 | 6.56 | 8.17 | 14.65 | 91.69 | 95.56 | 98.60 | 107.48 | 114.34 | 114.34 | 114.34 | 114.34 |

| Interest | 25.92 | 26.68 | 26.19 | 24.96 | 44.54 | 131.72 | 97.91 | 73.60 | 111.28 | 141.25 | 141.25 | 141.25 | 141.25 |

| Profit before tax | 17.68 | -22.35 | 12.65 | 19.07 | -79.35 | -72.98 | 95.99 | 85.98 | 29.45 | 156.39 | 156.39 | -255.59 | -255.59 |

| Tax | 2.91 | 12.24 | 2.32 | 4.14 | -0.58 | 6.98 | 17.90 | 13.26 | 5.75 | 18.72 | 18.72 | 12% | 12% |

| Net profit | 14.77 | -34.59 | 10.33 | 14.93 | -78.77 | -79.96 | 78.09 | 72.72 | 23.70 | 137.67 | 137.67 | -225.00 | -225.00 |

| EPS | 1.04 | -2.43 | 0.73 | 1.05 | -5.30 | -5.38 | 4.80 | 4.43 | 1.41 | 8.19 | 8.19 | -13.39 | -13.39 |

| Price to earning | 17.61 | -5.37 | 25.43 | 19.12 | -4.26 | -8.43 | 53.76 | 34.03 | 66.13 | 27.47 | 62.26 | – | – |

| Price | 18.28 | 13.06 | 18.46 | 20.06 | 22.58 | 45.35 | 258.18 | 150.80 | 93.35 | 225.10 | 510.00 | – | – |

| RATIOS: | |||||||||||||

| Dividend Payout | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | |||

| OPM | 2.71% | 0.65% | 4.15% | 4.54% | 2.51% | 6.58% | 7.80% | 4.80% | 4.34% | 6.78% | 6.76% | ||

| Source – Screener |

Black Box Ltd can benefit significantly from the growing data center theme in several ways:

- Increased Demand for Networking Solutions: As data centers expand, there is a growing need for robust networking solutions to ensure efficient data transfer and connectivity, a core offering of Black Box Ltd.

- Cybersecurity Services: With more data centers, the need for advanced cybersecurity measures increases. Black Box Ltd can provide essential cybersecurity services to protect these data centers from threats.

- Data Center Infrastructure Management: The company can offer infrastructure management services, including installation, maintenance, and optimization of data center equipment, ensuring smooth operations for clients.

- Unified Communications: Data centers require reliable communication systems. Black Box Ltd can provide unified communication solutions to enhance collaboration and operational efficiency within data centers.

- Enterprise Applications: With the rise of data centers, there is a higher demand for enterprise applications that manage and analyze data effectively. Black Box Ltd can leverage its expertise in this area to offer tailored solutions to data center operators.

Investing in Black Box Ltd comes with certain risks:

- Market Competition: The IT services sector is highly competitive, with many players offering similar solutions, which can pressure pricing and margins.

- Technology Obsolescence: Rapid technological advancements require continuous innovation and adaptation, posing a risk if the company fails to keep up.

- Economic Sensitivity: The company’s performance can be affected by global economic conditions, impacting client spending on IT services.

- Cybersecurity Threats: As a provider of cybersecurity solutions, any breach or security incident can damage the company’s reputation and client trust.

- Dependence on Key Clients: A significant portion of revenue from a few large clients can lead to financial instability if any major client terminates their contract.

Black Box Expands Footprint In India | Sanjeev Verma Explains | ET Now

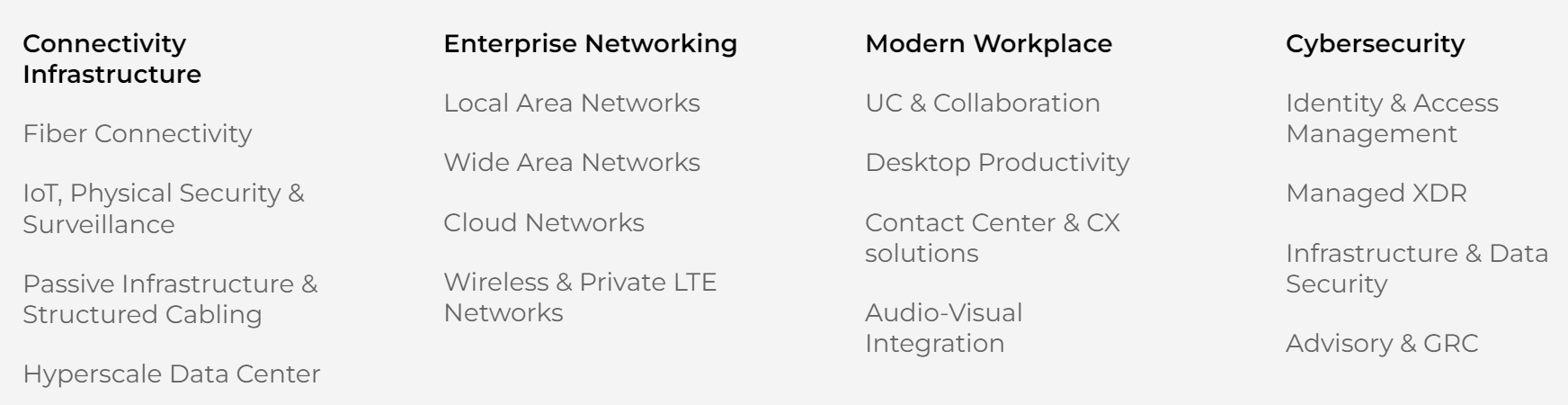

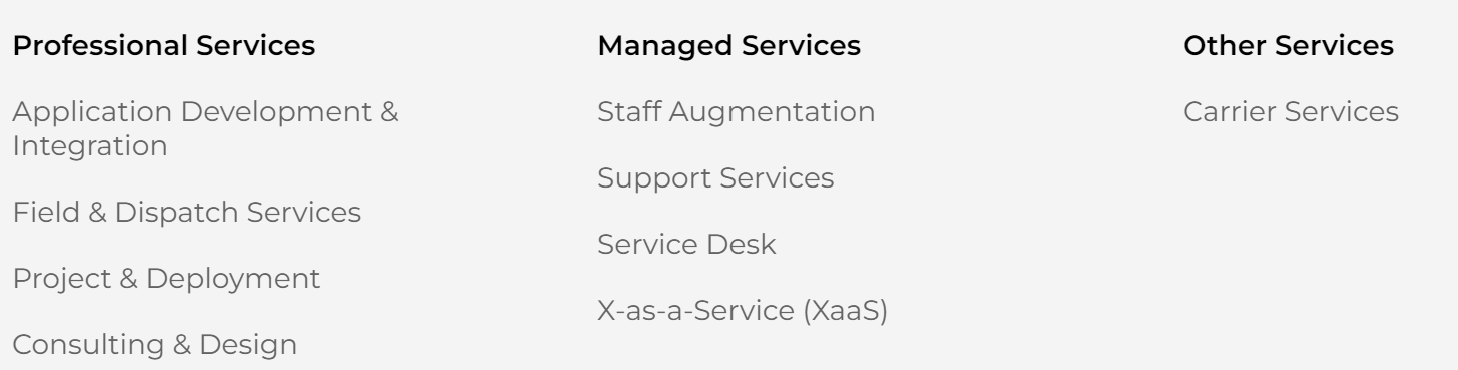

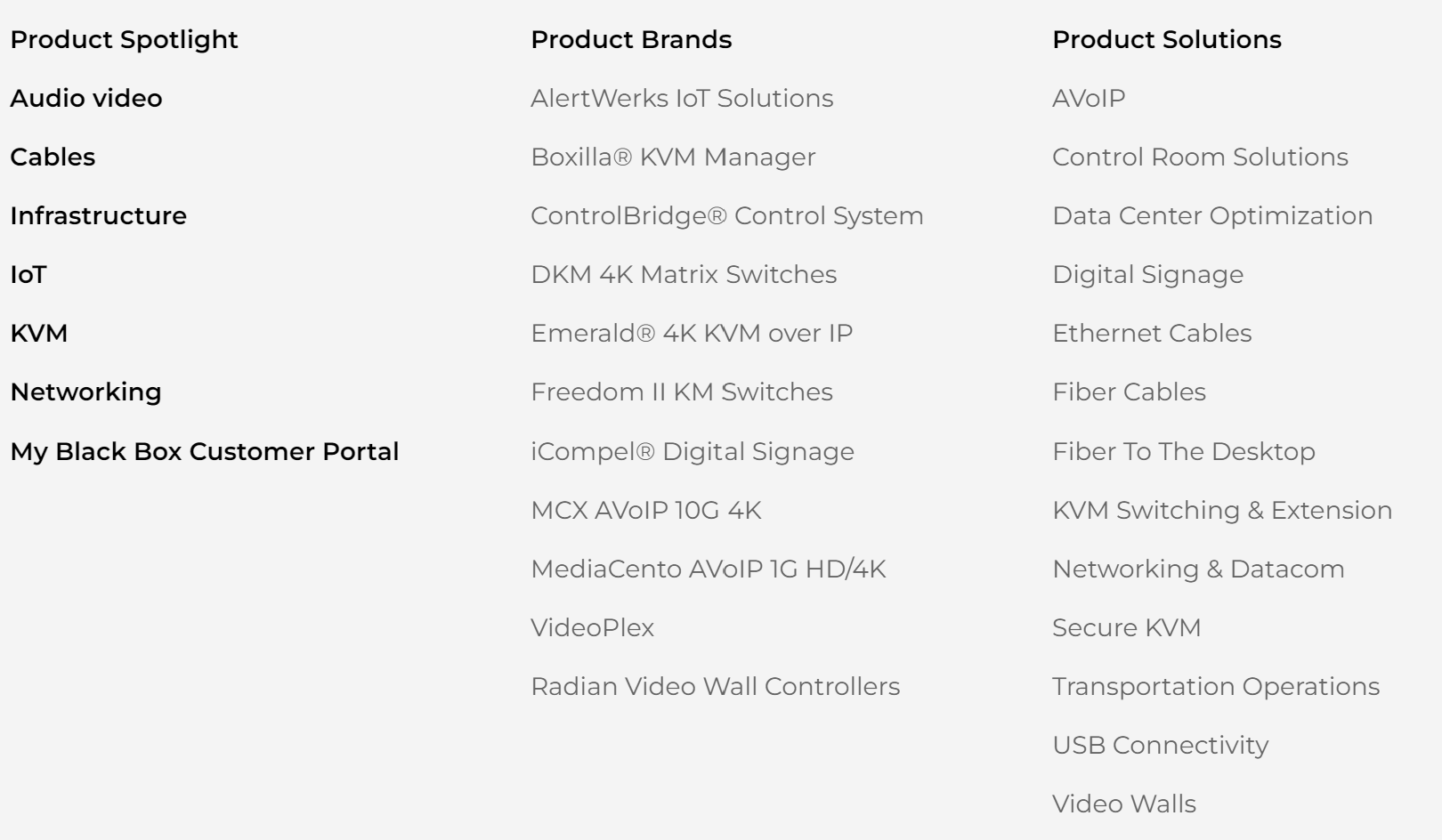

Solutions, Services and Products offered by the company –

Disc. – Invested