Check quarterly/annual P&L statement directly.

Posts in category Value Pickr

KPIT – CASE (connected, autonomous, shared, electric) – Focused Automotive Play (31-07-2024)

Let’s find out…

Salary Plus incentives for top 3 people

(Fig in Cr and truncated)

KPIT: 6.6 (CEO), 6, 4.5

LTTS: 15.4 (CEO), 6.3, 10.3

Persistence: 3.8. 12.7 (CEO), 2

Vasa Denticity aka Dentalkart – The Indian Amazon of Dental supplies ?! (31-07-2024)

This seems like an interesting company to analyze. High returns with limited capital. They’ve also paid off their debts last year.

Hope to hear more from management about expansion plans in terms of capital expenditure in the future.

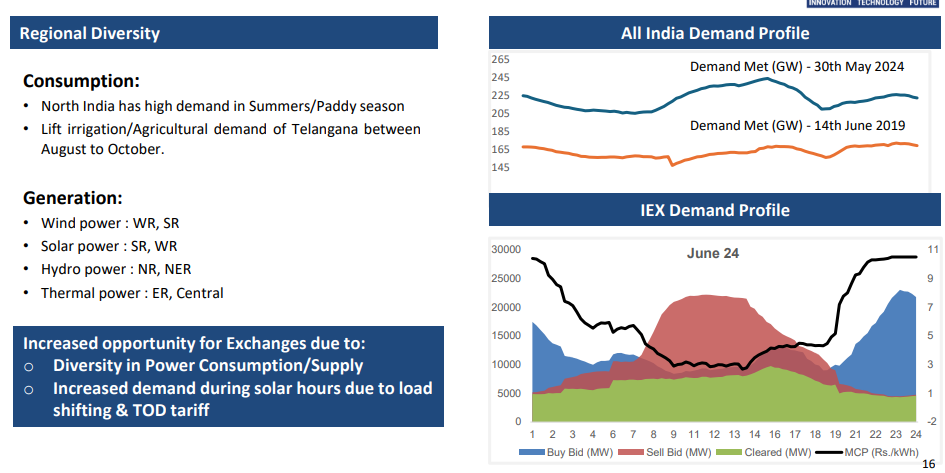

Indian Energy Exchange (IEX) (31-07-2024)

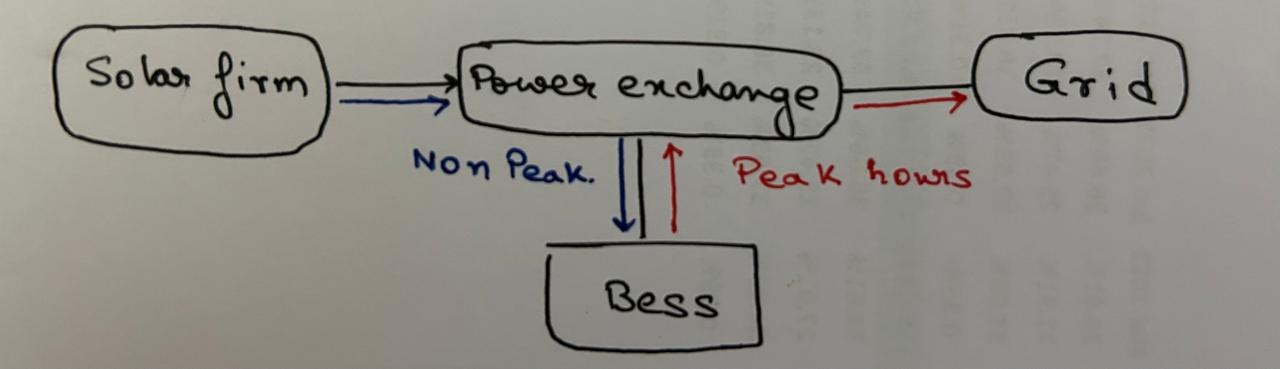

One interesting data that was given in the IEX call was on the role of exchanges in the energy transition and BESS (Battery Energy Storage Systems) and the power price arbitrage that will take place as Solar grows from 7% to say 20% of the overall energy mix.

Focusing on the solar power arbitrage , your non peak power cost is 3 rupees and your peak power in evening and early morning is 7 rupees. So a 7 rupee arbitrage for BESS ands with BESS prices are down to 3 rupee per unit from 10 rupee last year.

Source : IEX presentation

This is very good for both BESS players and Exchanges. A merchant solar farm can generate power in non peak hours for 2.5-3 INR and store the energy in a BESS via the exchange. They can Retrieve the same power in peak hours ( Early morning and Late evenings ) for 10-11 INR . However in this process they pay the exchange double.

Another data point on the BESS is how the prices have fallen making it attractive compared to coal based plants ( quick setup < 2 years, Lower cost, Green and less capital cost ) .

FY23 BESS battery setup cost was around 10 lakh per megawatt per month, now it has come down to 3 – 3.5 lakhs per megawatt per month ( and I feel it will come down further due to technological innovation which will expend life of the battery and newer chemistries ) . This brings the storage cost from 10 rupees per kWh to 3-5 rupees per kWh. Hence total cost of generation becomes 5-6 INR / kWh. This is cheaper than coal plant.

Disclaimer ; Invested and Biased.

Screener.in: The destination for Intelligent Screening & Reporting in India (31-07-2024)

Hi @Prdnt_investor,

Thanks for sharing your insights. I will share the same with our technical team for consideration. You can also track the Investors that you follow on this page: Register – Screener

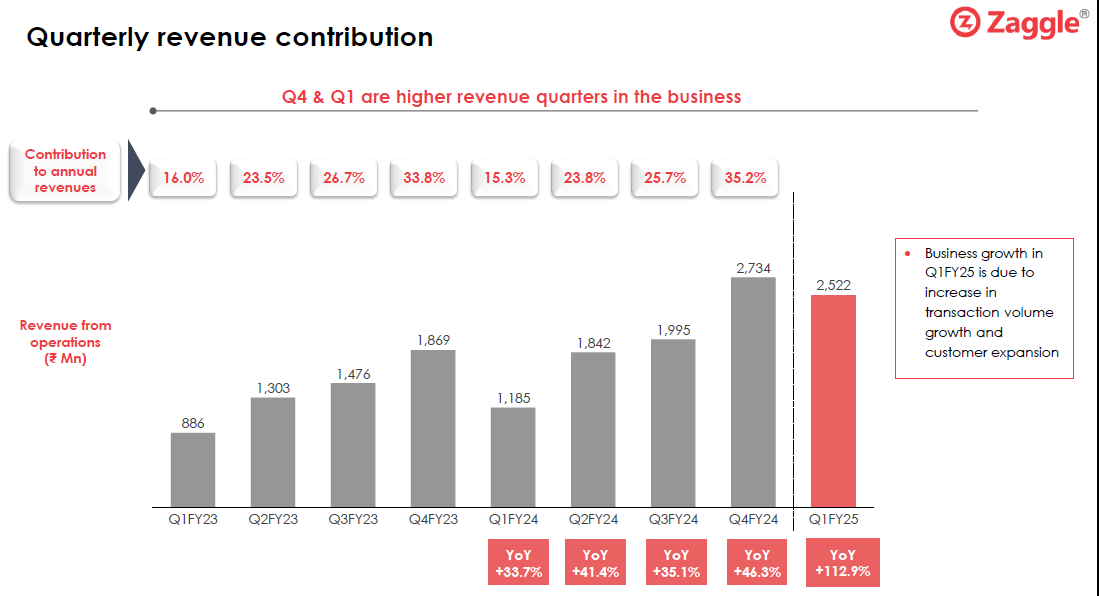

Zaggle_A platform to address pain points for enterprises (31-07-2024)

Great beginning for FY 25. Company guided to double FY 24 revenue in 2 years but looking at current run rate, expect this to happen much earlier…

Disclosure – invested for last 6 months

Shriram Pistons & Rings Ltd (31-07-2024)

Unfortunately I could not join the concall, however there are some important pointers to note in this business

-

SPR is the sole supplier for Pistons for the CNG bike Freedom 125. Though we can debate if the CNG bikes would work or not, it shows the technological advantage SPR has over competition. They have also mentioned that other OEMs are reaching out for similar technology. They will gain market share as this blending transition continues to take place.

-

SPR has an in-house facility for testing engines. This is crucial when considering the variety of fuel options in the mobility space, including Petrol, Diesel, CNG, EV, Ethanol Blending, Flex fuels, and Hydrogen (or ammonia). OEMs’ R&D budgets would be stretched thin trying to compete in multiple categories, so they would procure systems from Tier 1 suppliers. This ongoing transition is set to benefit SPR greatly. This is also why their EMFi electric motor business is interesting and can be a cross-sell product.

If gas as a percentage of our energy mix goes up, we will see more such products coming up.

- They produce the motors and motor controllers from the ground up, providing all performance characteristics to the OEM. Imagine SPR being involved in the co-development of a powertrain: given the engine specifications, they could easily add a few slides on how to make the powertrain hybrid or EV with minimal design changes and provide simulation results. ( I know I would have done that ) . This approach allows them to make an impact at the design stage of a powertrain, thereby increasing their integration and relevance.

As ethanol blending increases engines will go through significant wear and team. A very interesting video on the impact of ethanol blending in our older vehicles. This is also an opportunity for SPR.

Fundamentally the valuation is not demanding. Technically it has been consolidating for some time. Lets see if it breaks out.

Disclaimer: 6% of my PF, added during the June 4th Crash. I am heavily biased towards this business and the product.

Walchand Peoplefirst Ltd Dale Carnegie master franchisee (31-07-2024)

June 2024 quarter results have been declared. They have reported a loss after tax of Rs.21.74 lakhs vs Rs.31.58 lakhs profit after tax last year in June 2023 quarter.

JSW ENERGY — channel breakout (31-07-2024)

why is material and employee cost is less in jsw energy

Adani Power: Beyond ‘Adani’ (31-07-2024)

why is material and employee cost is so less in adani power