13 august results

Posts in category Value Pickr

Sandeep Kamath Portfolio | Momentum Investing (30-07-2024)

Ok so my portfolio ran into some pre-budget turbulence but such has been the bull run that by the time its time to take any action ( its Friday for me ), the recovery is already set in place. So no surprise that the portfolio stays as it is.

One lesson that I learnt though – Raymond ( part of my portfolio ) had a de-merger that meant that Raymond started trading ex-Lifestyle. Now have no clue when the Lifestyle business will get listed so till that time, I will need to stay put with Raymond not quite knowing if the momentum has reversed or not. Lesson learnt is to exit a stock that has been set for a demerger.

Portfolio start date → Jan 23, 2024

Total returns → 49.6%

Techknowgreen Solutions – Microcap in need of the hour business (30-07-2024)

Any recording available of this roadshow?

Mutual Fund Portfolio Review- Suggestions (30-07-2024)

Oh! I think I missed talking about ETFs

I was actively monitoring ETFs that day.

While the market was down 7-8%, the respective ETF was hardly down 2-3 % (With poor liquidity)

ETFs are not tracked properly in India and posses tracking error.

ETFs are big avoid for me for such days.

I agree “In my opinion, for such long time horizons, the NAV allotment on specific days (T+1, T+2) becomes less significant.”

But what is harm in investing lumpsum amount, with 10% less NAV(Market almost recovered 5% next day( T+1 )

Strides Pharma/OneSource – The Last Stand Will Create Wealth? (30-07-2024)

Back of the envelop calc: cmap 9465 for sale 4209 having pe 90 and evebitda 17.3

Onesource erstwhile stelis contributes 45% revenue.

Strides : FY25 E, Growth rate 12-15%

(4209 +15%) * 55% (deducting onesource revenue) * 20% (Ebitda) = 532, at EVEBITDA 17.3 comes 9203 cr.

Onesource : FY25 E

Guided EBITDA $65 mn i.e., 546 cr equating with peers EVEBITDA ratio of 20 comes 10920.

Gross : 20123

Even just the Guided EBITDA of 1000cr with evebitda 17 comes to 17000 cr. The hidden value of Onesource is the rationale behind the demerger.

Nuvama Wealth Management: Proxy to Affluent India (30-07-2024)

Thanks @investor12321 for helping me out with detail explanation. Now it really makes sense to me. Really appreciate efforts!

SRM Contractors Limited – A niche Infra player (30-07-2024)

This is a big risk IMO. All the road projects in J&K hilly areas have a bad history of delays and cost overruns. Earlier also, projects here have taken a huge toll on financial health of the EPC contractors like Gammon, HCC and Afcons (SP Group). The Chenani Banihal section of the National Highway has been under construction for 15 years now. It was originally stated for completing in 2015 as far as I recall. The company needs to diversify into easier projects in the plains.

PS: I belong to the area

Technocraft industries (30-07-2024)

Why sudden buying interest in this company?

Almost 20% up in 2 days- Any institutional buying.

Not that am complaining- Invested and biased😀

KPIT – CASE (connected, autonomous, shared, electric) – Focused Automotive Play (30-07-2024)

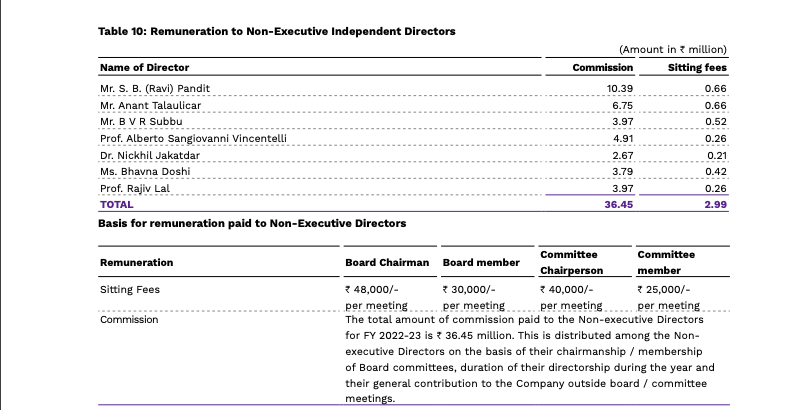

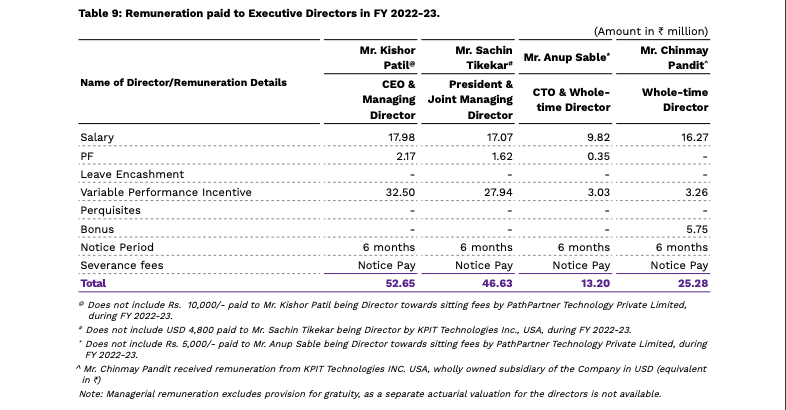

Are these considered a decent renumeration to the CEO and directors?