@Shahrajk and @sameernics The joke is noted ![]() The practical reason is to manage career progression.

The practical reason is to manage career progression.

Posts in category Value Pickr

Hiring l Investment Associate l 12-18L l 1-3yr exp l Bangalore (30-07-2024)

Indian Energy Exchange (IEX) (30-07-2024)

Few other interesting points in the call apart from those stated above:

- Growth of exchange is 2.7 times growth of power market in India.

- Market penetration of exchanges increases significantly after renewable share in overall energy mix crosses 20% (This has happened in India).

- Discom losses have come down below 15%. Many discoms have seen their credit ratings improve.

- TAM upto 11 Months to be allowed on exchange. This will add another 40 BU to market size of exchange.

- Generators are now required to offer unrequisitioned power on exchange.

- Battery energy storage system(BESS) costs have reduced drastically. Charging (Non-Peak) and Discharging (Peak Hours) of BESS can be done through Exchanges.

Disc: Invested

Titagarh Rail Systems – Is this train finally moving? (30-07-2024)

Q1 FY25 Highlights (Consolidated, YoY)

- Revenue down 0.9% to Rs 903 crore versus Rs 911 crore

- Ebitda down 4% to Rs 102 crore versus Rs 106 crore

- Ebitda margin narrows to 11.3% versus 11.6%

- Net profit up 8.4% to Rs 67 crore versus Rs 62 crore

Revenue growth was primarily led by the company’s larger segment i.e. freight rail systems, which recorded 12.9% growth to Rs 842.19 crore. However, the passenger rail systems segment declined 63.04% to Rs 60.86 crore.

Zaggle_A platform to address pain points for enterprises (30-07-2024)

Numbers are inline with guidance. This year PAT should be 80-90 cr.

Q1 is seasonally weak. A decent start to Fy25

Jindal Stainless (Hisar) (30-07-2024)

FY25 Q1 results released

- Net revenue (9,585 Cr): QoQ: 1%, YoY: -4%

- EBITDA (1,004Cr): QoQ: 21%, YoY: -10%

- PAT (578 Cr): QoQ: 21%, YoY: -13%

- Sales volume 5% up YoY, 1% up QoQ (Composition: 10% exports, 90% domestic)

- FII holdings increased to 22.49% from 20.83% QoQ

Commentary:

- stagnant growth in the US and EU markets, the export volumes of the company have remained flat on a QoQ level

- ongoing Red Sea issue extended transit times and freight cost from India to the western markets, and paucity of containers further affected exports

- company sources most of its raw materials from nearby shores and domestic suppliers, the company was largely able to mitigate cost and time risks arising from the crisis

- Cheap imports from China and Vietnam continue to pose threat to the domestic industry

Other points:

- During the quarter, with an investment of approximately Rs 715 crore, the company entered a JV to develop and operate a stainless steel melt shop in Indonesia with an annual production capacity of 1.2 million tonne per annum

- The company also set aside around Rs 1,900 crore and Rs 1,450 crore for the expansion of its downstream lines and upgradation of infrastructural facilities respectively, in Jajpur, Odisha

- During the period, the company completed total acquisition of Chromeni Steels Private Limited (CSPL), which owns a 0.6 MTPA cold rolling mill located in Mundra, Gujarat, for over Rs 1,600 crore, comprising payment towards equity transfer and payment of shareholders’ debt

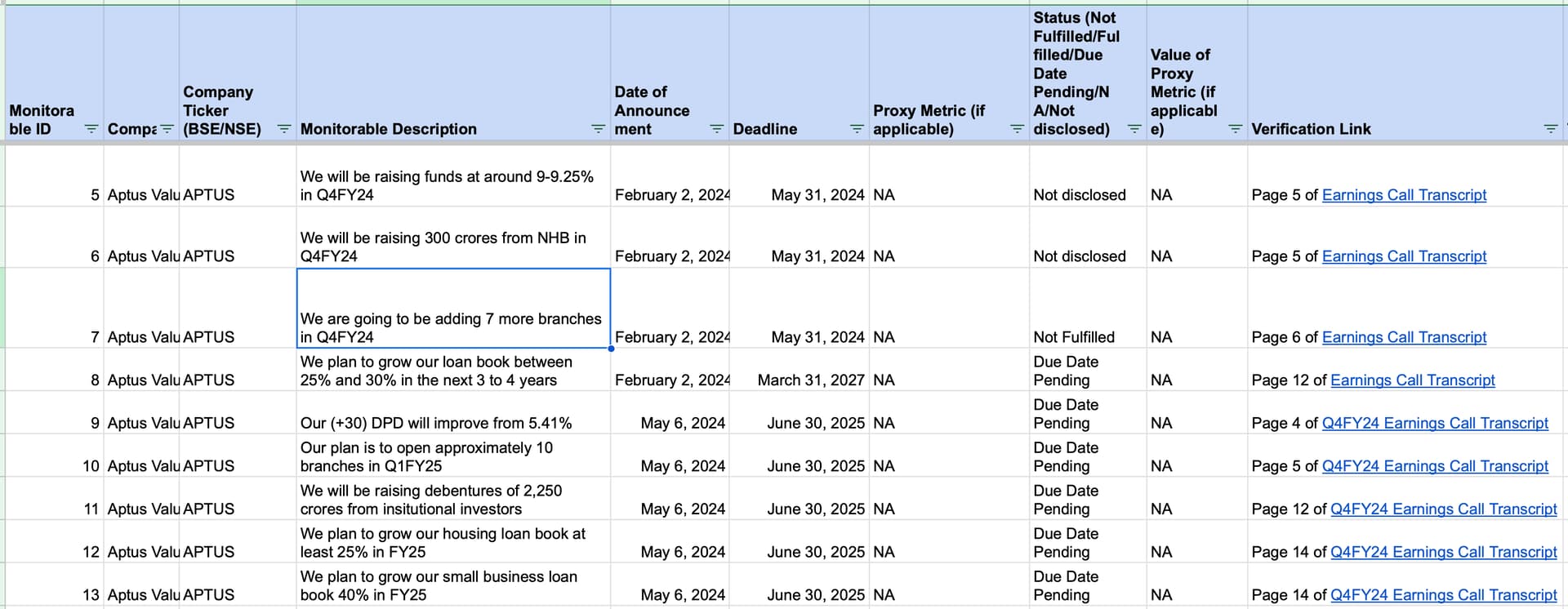

Aptus Value Housing : Is valuation justified or just another HFC? (30-07-2024)

Hello,

In the below tracker, I have started tracking important company goals for Aptus. These goals are referred to as ‘monitorables’ in the tracker.I will update this document regularly to reflect the current status of these goals.

Here’s a snapshot of what the tracker includes:

- Company Ticker: For identifying the company

- Monitorable Description: Description of the goal or metric being tracked

- Date of Announcement: When the monitorable was announced

- Deadline: Target date for achieving the monitorable

- Status: Current progress (e.g., Not Fulfilled, Pending)

- Verification Link: A link to see where I got the information about the goal.

I hope this information makes it easier to observe how well companies are progressing towards their stated goals.

Screenshot of the tracker below:

Full tracker attached below:

Tracking Company Monitorables-2.xlsx (134.7 KB)

Post Script: DM if you want me to track the monitorables for any specific company.

Wonderla Holidays (30-07-2024)

Hello Folks,

I have exited the stock recently and would want to share brief update here:

-

Firstly, Did not particularly like Q4FY24 results. The growth was flat v/s Q4FY23, but most importantly there was severe footfall degrowth, flat revenue was only due to very good ARPU increase. So, with recent hirings at top level and additional ESOP cost, EBITDA took a hit.

-

Management in past 3-4 quarters have been stating that these are the best margins and best footfalls we have achieved. While they have confirmed further footfall growth, but they also said EBITDA% would drop a bit as these are at very high levels. Basic screening shows that footfalls were at highest in FY24 and Margins were at highest in FY23. So, there is no element of further upside surprise?

-

Thirdly, the valuations were not cheap (As per my understanding). And earnings growth forecast has been reduced by the fact that they were at peak. So, it did not particularly gave me comfort to hold for longer.

-

And because of all the above + good entry point of 200-220, i have kept a momentum based approach to exit stock if it falls and ride as it kept rising. Also, possibly starting of Odisha Park meant more stress in near term as costs will be front loaded. Hence, had kept tight stop and exited the stock when it hit my SL levels in June when actual NDA results came out.

-

Q1FY25, kind of continued the negative footfalls. Banglore taking a -25% hit on footfalls and other parks too. Ex-odisha the results are -11% in revenue and -22.5% in EBITDA. And things will also not turn immediately given that Odisha park will also need to stabalize to contribute significantly to PAT.

-

By the time Odisha Park starts contributing, we have Chennai Parks cost front loaded when it starts. Obviously, there will be surprise in form of new park announcement, but fundamentally things will look dull for FY25 atleast.

Hence, a combination of above was reason I exited the stock. However note that, the reason for my exit was that I had entered low and wanted to protect gains in case if market corrects a bit. And my choice of not going through temporary dull period (my expectation of FY25).

These are just my views which could go wrong, hope it helps!

Regards,

Mukul Jain

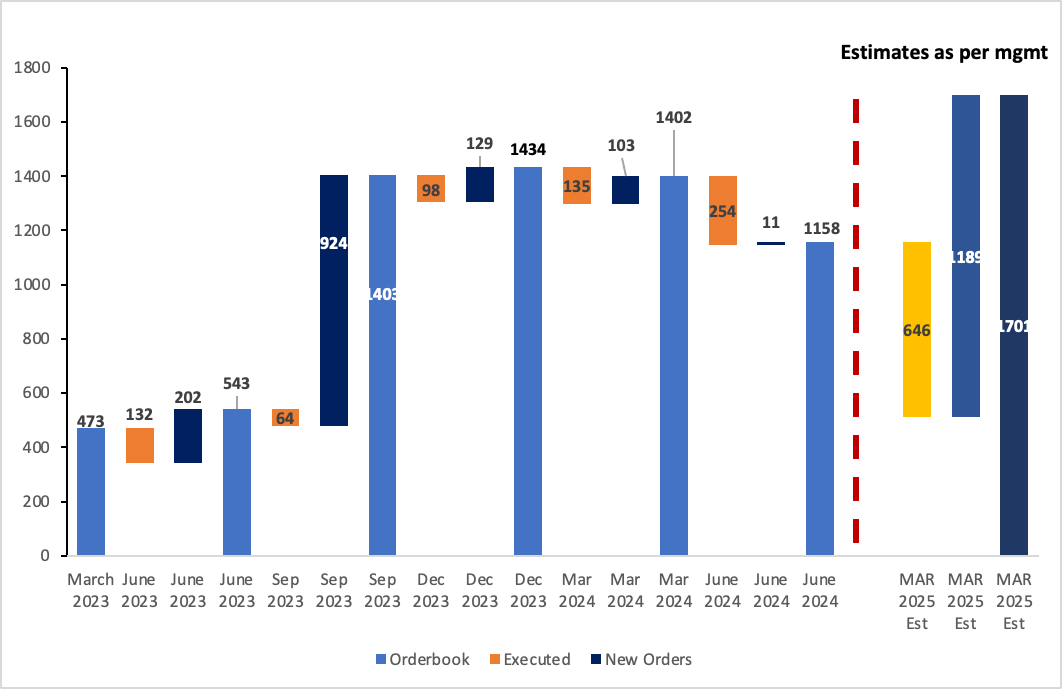

Zen technologies – A micro cap in the defense space! (30-07-2024)

Updated Orderbook trajectory as per management guidance (This is including AMC)

Nuvama Wealth Management: Proxy to Affluent India (30-07-2024)

This is not borrowing in the traditional sense where a company would borrow to buy PP&E and put up a plant.

The debt you are referring to is essentially financing the margin trading/loan against securities business of the Cap Markets/WM business which you can see appears on the asset side of the balance sheet.

Most of the debt is market-linked – so you are essentially earning a spread by lending out at slightly higher than you are borrowing. And it is collateralized.

It is a source of income, but not the primary business – it serves to complement the core Cap Markets/WM business.

Jenburkt Pharma – Analysis Report (30-07-2024)

I attended AGM of Jenburkt Pharma. Missed around first 15 minutes of discussion. Find enclosed key points from Management reply to shareholder’s queries/question. Please note that there could be communication error at my side.

Key points:

Revenue:

Domestic sales Rs 121 Cr, Exports, Rs 20 Cr. Domestic market registered 10% growth in FY24,

In domestic market Top 6 state for company are as under: Karnataka Rs 34 Cr, Maharashtra Rs 25 Cr, Gujarat Rs 10 Cr, UP Rs 9 Cr, MP Rs 7 Cr and TN Rs 5 Cr.

The management also provided details of top 5 products. However, I could not capture the name of brands. Top Brand is Nervejin group which account for Rs 58 Cr, 2 largest brand sales Rs 17 Cr, 3-4 largest brand sales was Rs 13 Cr each. Nervejin group also have multiple products which aggregate to Rs 50 Cr+. The company expects that Powergesic and Zixa has potential to reach more than Rs 50 Cr over medium term.

In FY24, Domestic market growth was mainly driven by Price increase and volume growth. One new product syrup was launched only in March 2024, which has limited impact on FY24 sales, although has improved performance during FY25.

The company would focus on core segment in acute market. While it has aspirations to move in Chronic market, current product portfolio and marketing strength does not make entering in Chronic segment a winning proposition.

The company does not have any exclusive tie up with Hospital as margin are very lower in such arrangement. One key aspect highlighted by management is they would continue to remain bottom line focus.

Also, when asked specifically about slow down domestic growth rate from Double digit during FY13-FY19 to less than inflation during FY24/19, management indicate that they are aware about slow growth. However, recent initiative like Wellness division focus, increased new product launch and revival in export market, they expect growth rate to reach again in double digit in medium term. However, they would not lose their focus on long term profitability.

Wellness division

Company has launched new product family under brand name Zixa under Jenburkt wellness division.

Total sale from wellness division was Rs 0.4 Cr with expense of Rs 2.53 Cr. However, management is optimistic about prospect of wellness division. They also intend to increase OTC product which has insignificant share (0.3% of revenue) in revenue. Wellness product is available in 1990 retail store as on 31 March 2024. Since then, coverage is has increased significantly. The company continue to market wellness division products in Indian Football league and Various marathon in India.

Exports

Exports declined by 21% during FY24. Sri Lanka is largest export market with Sales of Rs 6.9 Cr followed Beirut (not sure About the name) at Rs 6.1 Cr during FY24. Difficult economic condition and higher regulatory approval time were the main reasons for decline in exports sales. While management is confident to get back on growth track in long term, in medium term export market would continue to face challenge.

Higher receivable in export market was mainly due to increased shipping time and higher regulatory approval time. However, most of sales in export market is covered under ECGC group which reduces default risk for the company.

Disclosure: Jenburkt Pharma is among my core holding (1.6% of equity portfolio). I have not done any trade in last 30 days. I may increase/reduce/exit from my investment without informing forum. My view may be positively biased due to my holding. I am not SEBI registered advisor. I am not suggesting any investment action.