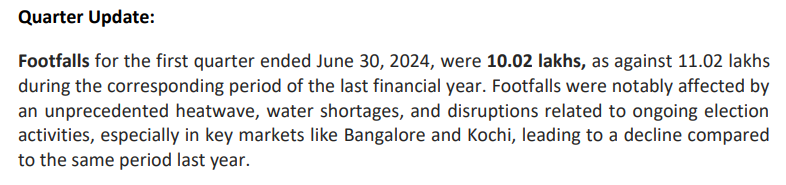

I hope this is true, why did they mention water in the press release?

I hope this is true, why did they mention water in the press release?

Invested (please verify calculations):

We are definitely disappointed.

There is a conference call today, and we hope they have some optimism for us to latch onto.

The company has not excited us for the last few quarters. Of course, there is the expenditure in Chennai and, to a smaller extent, Orissa. Again, we suffered lower footfall and less spending on food. Now, we hear about water problems. Operating profit margin (OPM) is still good but has dropped compared to before.

If the situation is going to be lower footfall at all the old parks, are we looking at chasing a snowball downhill with capital expenditure across the country?

Even the old parks have to remain viable. If not increasing profits, we definitely should not be looking at lowering profits by 25%, especially in our busiest season. Our bread and butter right?

We hope sir has answers for us.

| Growth | YonY |

|---|---|

| Revenue | -6% |

| Other Income | -19% |

| Expenses | 20% |

| PBT | -26% |

| PAT | -25% |

| EPS | -25% |

| OPM | 48% |

From the concall of nitin spinner. courtesy suru bhai on x. inventory levels are not huge.

It is vital to look at business , mgt then take a call. A company of 13 crore raising capital of almost same amount and Q1 business update is 3 times revenue then last year and future looks even better if they are able to execute. Do your due diligence I am invested for longer term and see hundred bagger in making in years ahead , will keep an eye on business potential as they are changing business model.

Fy25 Q1 results are out

Net profit at up 25.5% ₹1252.6 cr vs ₹994 cr (YoY)

Revenue up 28.3% at ₹7,197 cr vs ₹5,611 cr (YoY)

EBITDA up 31.8% at ₹1,991 cr vs ₹1,511 cr (YoY)

Margin at 27.7% vs 27% (YoY)

Cons. sales volume growth 28.1% YoY / India 22.9%

Stock split announced: 5Rs FV will split to 2Rs FV

Interim dividend of 25% of the face value, i.e., Rs. 1.25 per share

Ravi Jaipuria, Chairman, Varun Beverages Limited said,

“We are pleased to report robust performance for the second quarter of CY2024, achieving a consolidated sales volume growth of 28.1%, which includes volumes from BevCo. The impressive volume growth of 22.9% in India primarily contributed to this outstanding performance, supported by our expanded capacities, enhanced distribution network, and a strong summer season. Meanwhile, our international markets remained relatively flat, moreover it was a seasonally weak quarter for African market. We are excited to announce further expansion in our partnership with PepsiCo, having entered into an Exclusive Snacks Franchising Appointment to manufacture, distribute, and sell “Simba Munchiez” in Zimbabwe by October 2025 and in Zambia by April 2026. This follows our recent announcement to manufacture and package Cheetos in Morocco by May 2025.

With strong performance in a key quarter, we are on track to deliver healthy double-digit growth in this

calendar year.

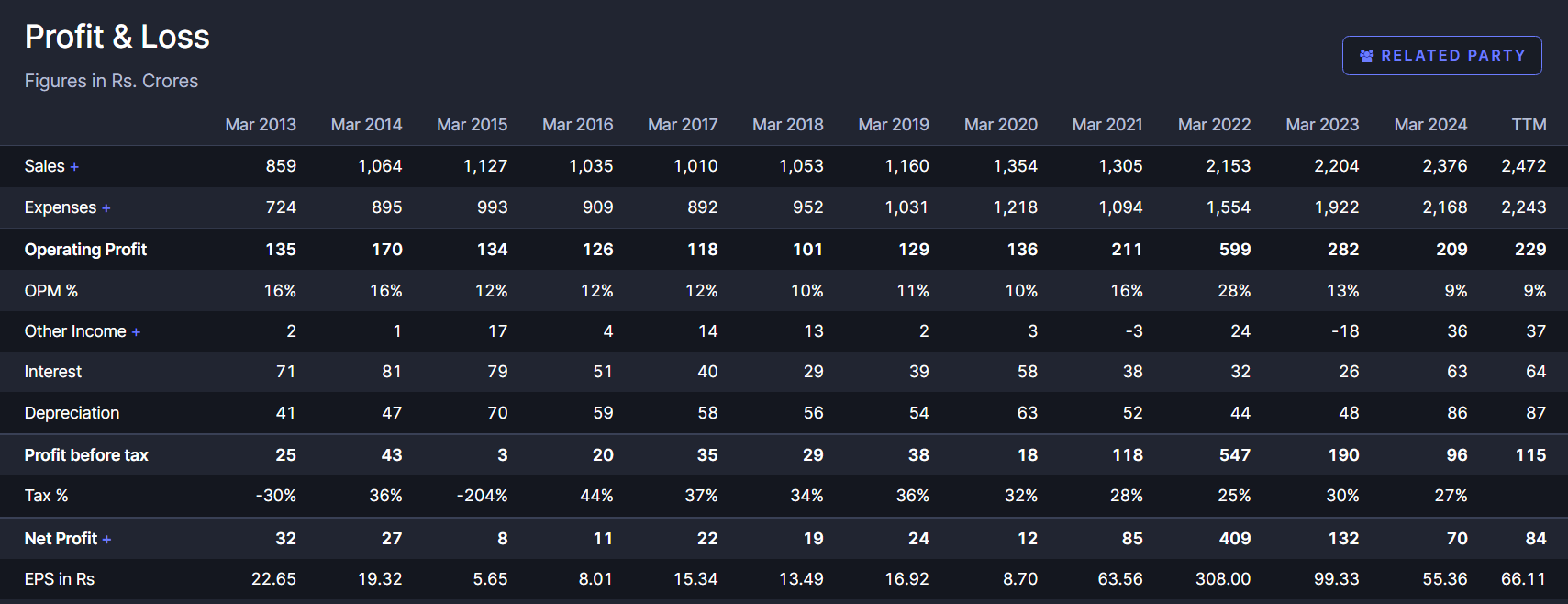

FIxed assets have gone up substantially and the max turn of more than 5 was achived in last upcycle. So the company has the ability to achieve good sales growth and scale with current capacities. Also i noticed a large jump in depreciation which will be aiding the FCF.

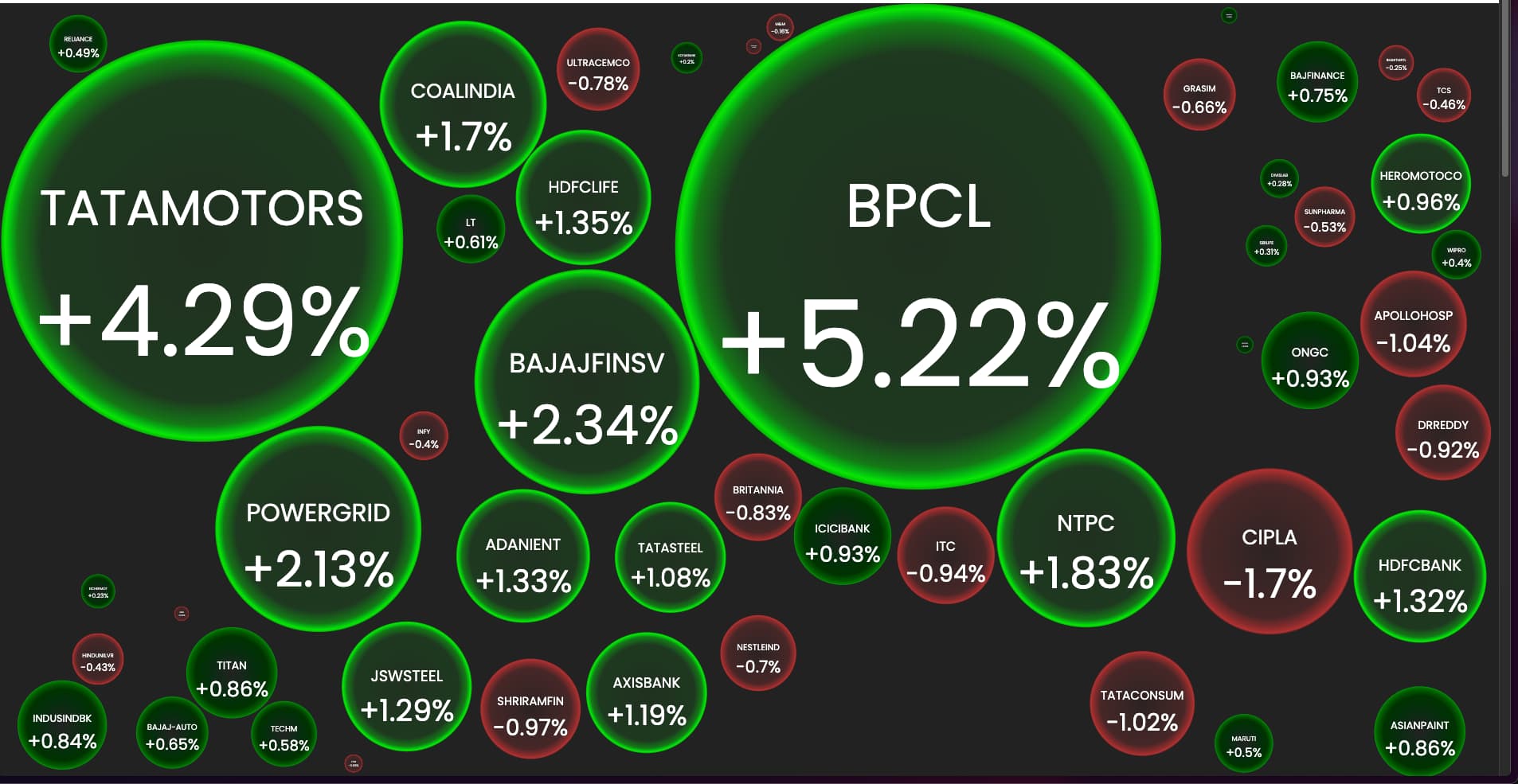

Tata Motors Blasting Today

Management has guided for 50% gross margins so it will probably sustain in this range.

Chart broke out of a long consolidation and contraction. volumes were pretty supportive.

I liked that the sales growth continued during the downmove as well which kind of signify stable and growing business profile. Margins were in double digit for the year 21 and double of that in 23.

4. Excellent work by @phreakv6 as always in inspiring and documenting his thoughts on the thread. I will now try the same and am open to feedback.

5.

disc : invested from 1100 levels