Posts in category Value Pickr

Jupiter Wagons Ltd (previously CEBBCO) (27-07-2024)

- Overall Performance:

- Impressive revenue growth of 19% year-on-year (YoY) and robust EBIDTA growth of 32% YoY.

- Profit after tax (PAT) growth at 40%, with improved margins.

- Notable impact due to elections and peak summer conditions at multi-location facilities.

- Successful completion of a 6-month trial for the 11.2 kW system, securing an order from Siemens for the Vande Bharat train.

- EV Business:

- ARAI approval for commercial production of a 1.0-ton, four-wheel light electric vehicle with fast charging capabilities (full charge in 20 minutes). Certified range of 127 km.

- Production set for Q2 2025, with an initial batch of 500 vehicles (primarily B2B).

- High localization (80%) makes it eligible for subsidies.

- Promising demand potential in the 1 to 3-ton category.

- BIPL (Wheel Set Business):

- Remarkable 5X revenue growth reported.

- Plans to sell wheel sets to Indian Railways, Vande Bharat, and metros.

- Ambitious goal of establishing a 100,000-wheel set facility by 2027 for both exports and domestic consumption.

- QIP funds utilized for building a forged wheel and axle plant, enhancing backward integration.

- Jupiter (Brake Business):

- Leveraging partnerships, design capabilities, and backward integration.

- Sustainable margins attributed to wheels and braking systems.

- Strong order inflow expected, with ongoing work on Lithium-Ion batteries.

- Wheel Set Segment:

- Wheel sets need replacement every 7 years.

- Demand: 500,000 wheel sets per year (aftermarket) and 100,000 wheel sets per year from OEMs.

- Initial capacity of 100,000 sets per year by 2027, with potential for expansion.

- Forged wheels are the future due to high-speed requirements.

- Different pricing for freight vs. high-speed wheel sets.

- Anticipated revenue of 200 to 250 crore in FY 2024/2025 with Stone India.

- Forging facility expected to contribute significantly, achieving revenue of 4,000 to 5,000 crore with margins exceeding 15%.

- Container Business:

- Focusing on enhancing capacity for containers used in data centres and battery applications (not marine containers).

- Higher margins in data/battery containers.

- Collaborating with major players like TATA, Reliance, and Schneider.

- Global Total Addressable Market for container solutions estimated at 5.0 gigawatts, with potential growth to 10 gigawatts.

- Guidance:

- A strategic shift: By 2028, more than 50% of revenue will come from non-wagon businesses.

Conclusion:

1. There are multiple levers of growth.

2. Margins are increasing continuously with commentary of further increase.

3. Non Wagon revenue going to increase to 50% by 2028.

4. 7000 cr. of order book give visibility for approx 1.5 years.

5. Wheels business will give stability to revenue as it is replacement as well as OEM product.

6. Strong partnerships.

7. Valuation are high.

D: Invested

Ranvir’s Portfolio (27-07-2024)

thank you so much ranvir for sharing your valuable insights about innova captab ltd. it is my biggest holding in my portfolio .

Smallcap momentum portfolio (27-07-2024)

@visuarchie , Your strategy is more watertight. Generally if you select top 20 stocks then unless the stock exit top 40 ( 2 times ur selected number) , you are not supposed to sell. But you sell immediately when stock goes out of top 25. So you are more strict about your exit criteria. Also your re-balancing is weekly, instead of bi-weekly or monthly. Hence , even if you dont follow any stop loss or dont sell when stock goes down substantially, its still OK, as you are already quite strict. But ppl like me who give the stock rope till it doesn’t cross 2 times the number and do bi-weekly or monthly re balancing, its better to have some mechanism like stop loss or some fixed percentage, below which you wont permit the stock to go.

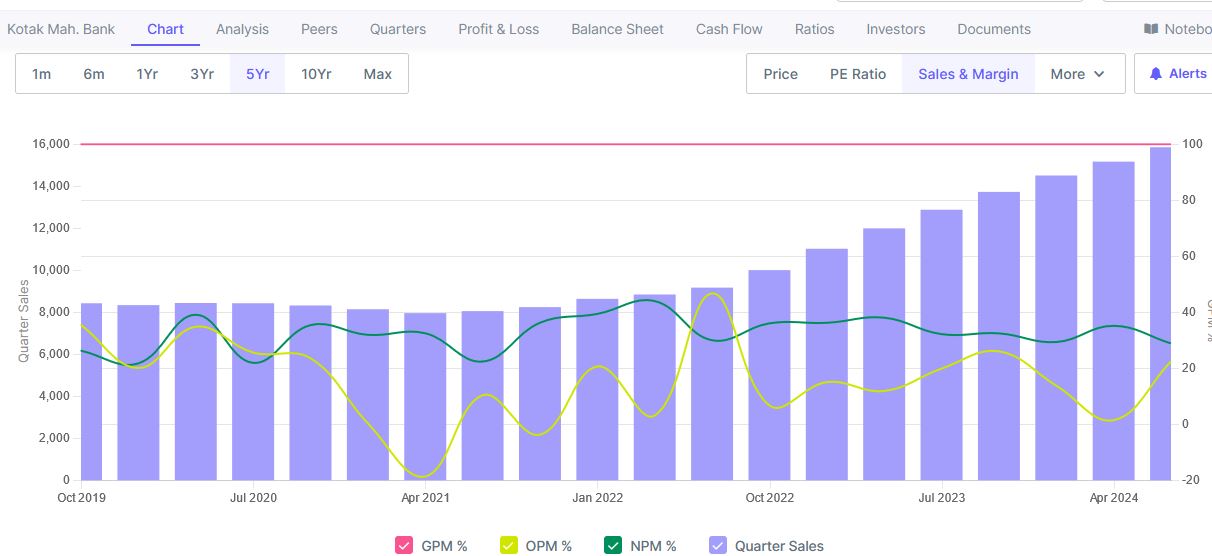

Analysis of kotak mahindra bank in screener.in (27-07-2024)

I was analysing kotak mahindra bank in screenr.in when I checked out sales & margin in chart , their is net profit margin is higher then operating profit margin

As i found in other stocks operating profit margin is higher then net profit margin.

why NPM and opm are behaving diffrently in case of kotak mahindra bank

what conclusion we can drive from this data of opm and npm ?

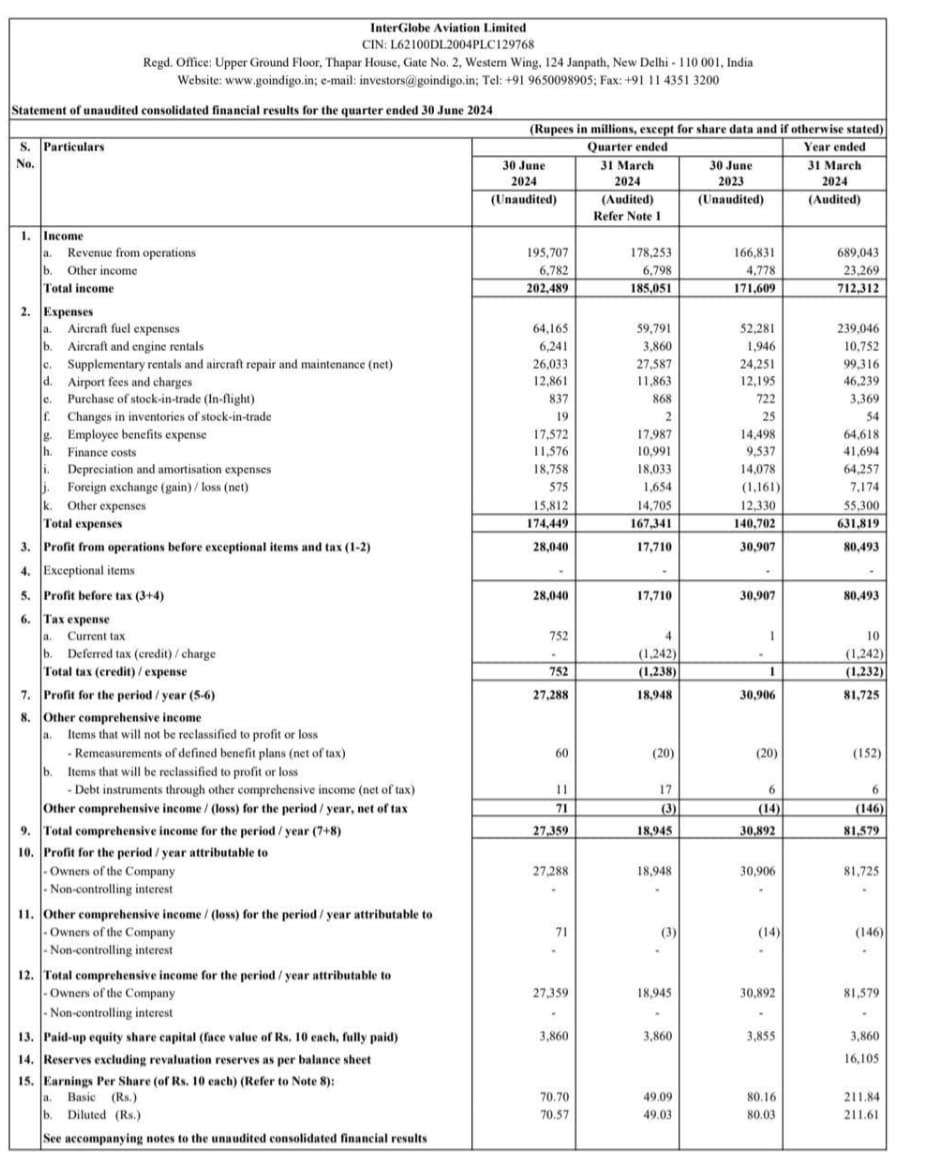

InterGlobe Aviation – Indigo (27-07-2024)

Stunning results by Indigo

Same time an year back GoAir issues helped indigo and thus we initially thought confluence of things would make this Qtr tepid. But Indigo did one up. Great show.

They held onto their own YoY which is great and commendable.

SBI Cards & Payment Services Limited (27-07-2024)

broad level question – this looks like similar to AMC industry the high margin – high expense ratio led businesses of active management got replaced by very low fee passive fund management.

Initially, everybody pictured the doomsday scenario for AMC’s in market then bcoz of unprecedented shift in saving pattern in india recently the sheer volume of move to index fund compensated for it and also cost rationalization help AMCs recover margins and back to growth path.

Can Credit Card industry see the same fate? the easy money business model of charging high interest on revolvers is gone. All fintech’s like CRED , Paytm etc and fin influencers have disrupted it by continuously reminding user about the late fee and charges now revolvers are going down. All companies are left with is

a) EMI products (somebody buying online on EMI using card)

b) Annual Fee on credit cards

c) Cut backs on cashbacks and offers.

This i believe will have temporary impact on earning but eventually this is highly healthy business model but hard to gauge here how fast this shift is happening and what steady state growth we will see over a long run.

I welcome your thoughts here let me know ?

TVS Supply Chain Solutions- A Business Analysis (27-07-2024)

good read on TVS Supply Chain Solutions Ltd. – by Dhruva Pandey

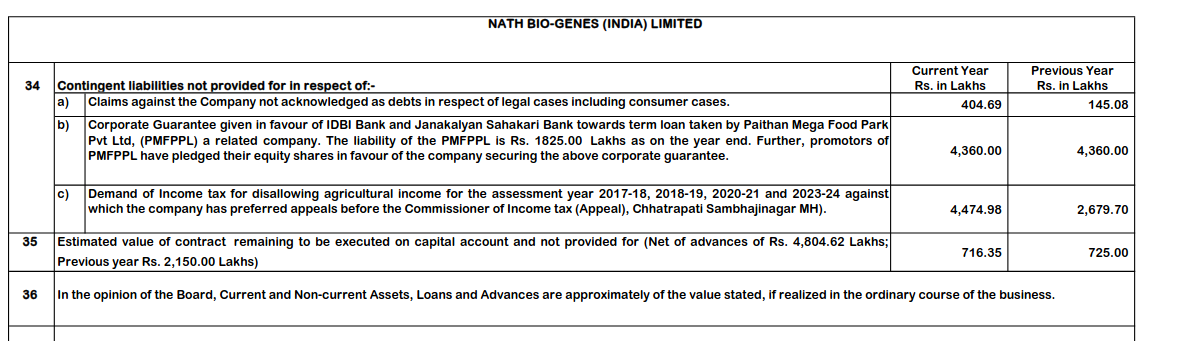

Nath Bio-Genes ….. Seeds player (27-07-2024)

There is an increase in contingent liabilities from about 77Cr to 97Cr. Out of this, 43Cr is income tax demand for disallowing agricultural income.