True, but in present market, before 50DMA goes below 200DMA, your PF will be down by 15-20%. Hence risk management is crucial. This is one reason I prefer part entries, instead of going in all at once

Posts in category Value Pickr

Carysil (earlier Acrysil) – Kitchen sinks (26-07-2024)

They had some acquisitions plans to meet 1000 Cr revenue target, QIP funds might be used for acquisition purpose only

PDS Limited – A platform for entrepreneurs (26-07-2024)

Did anyone attend the AGM earlier today?Would really appreciate if someone can summarise the findings and if there are any new interesting developments apart from what was said on the concall! Thanks in advance!

Nuvama Wealth Management: Proxy to Affluent India (26-07-2024)

Can we still call Nuvama a wealth management company when 2/3rd of the PBT is from capital markets biz. On the contrary, we have Motilal Oswal trading at 12 PE and having contribution of 50% of PAT from wealth management (https://www.bseindia.com/xml-data/corpfiling/AttachLive/e74755db-f79f-409f-a537-68e259ed9a59.pdf).

With this spike in capital markets contribution in recent quarters its getting difficult to have a peer to peer comparison on valuation with the likes of 360 ONE, Anand Rathi etc. The question is whether there is a possibility of derating?

All your views are appreciated on this!

Bulk Deals Bi-Weekly Log (26-07-2024)

15th Bulk Deals Log

Date: 25/07/2024

NSE Link: https://www.nseindia.com/report-detail/display-bulk-and-block-deals

BSE Link: BSE Equity : Bulk Deals

- Kataria Industries

Seems like a new listing which is in the Low Relaxation Pre-Stressed Concrete segment. I haven’t really heard of this segment before. I think it does deserve a deeper study.

Investor who bought: Multiplier Share and Stock Advisors

Quantity Purchased: 1.8 Lakh

Average Price: 201.05

- Mahickra Chemicals

Very interesting pattern on the charts, has seen significant promoter buying over quarters. Is in the dyes and pigments space, which is performing well. Could be a good story to play.

Investor who bought: Monil Kirtibhai Parsana

Quantity: 50K

Average Price: 106.29

Quant Firm Interest

- Apex Frozen Foods

- Bhagiradha Chemicals and Industries

- Confidence Petro

- Data Patterns

- Everest Kanto

- Hindustan Construction Company

- Hind Oil Exploration

- IFCI Ltd

- Intl Conveyers

- Khaitan Chemical and Fertilisers

Microcap momentum portfolio (26-07-2024)

One of the techniques that is used is when index 50 DMA goes below 200 DMA you have to start converting your position to cash. Momentum strategy works only with trend.

Xpro India – getting bigger? (26-07-2024)

dear all,

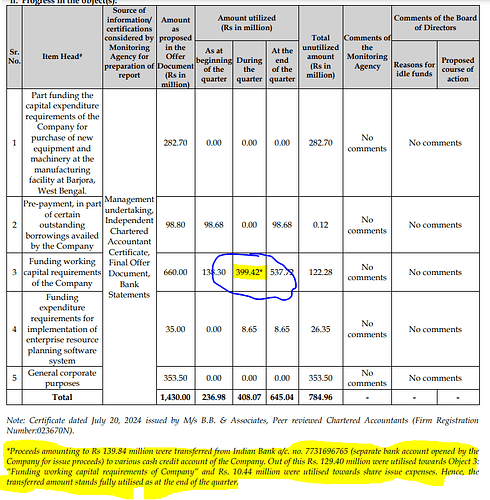

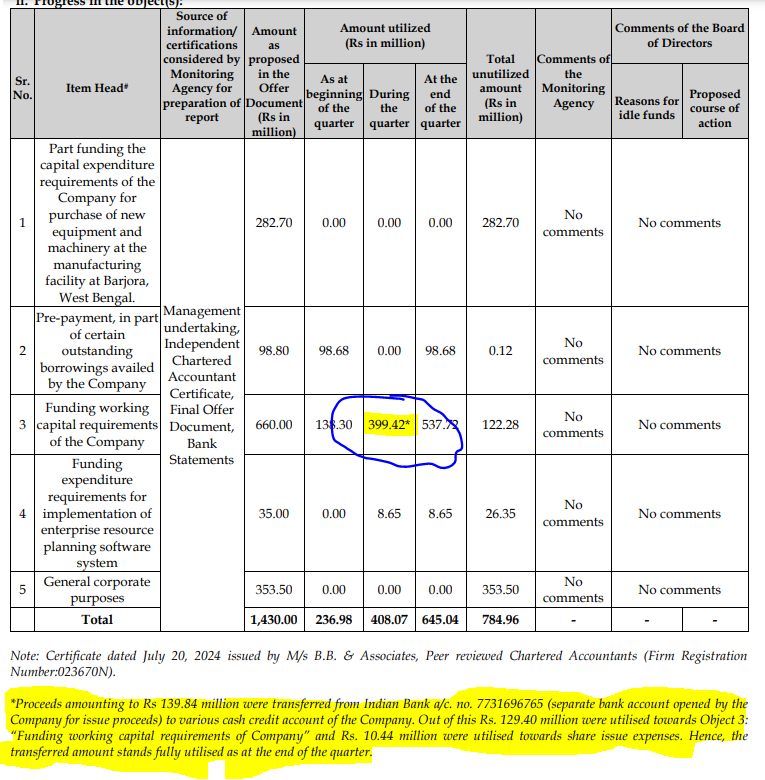

I am studying this business. While going through latest Monitoring Agency Report in relation to Preferential Issue & Qualified Institutions Placement dated July 26, 2024, i noticed that company used 399 M Rs for working capital. however in asterisk, only details for 139 M rs is provided. what happened to remaining amount. (i.e. 260 M rs.)

Queries

- If only 139 Mrs were transferred than why the utilisation for quarter is 399 Mrs.

Shivam27’s Portfolio and Investment Journal (26-07-2024)

Hey Shivam,

Regarding Ethos, wanted your view on consignment sales condition Ethos has adopted with certain brands! Instead of buying out whole inventory from the brand, they are getting the same inventory at certain advance payment after which they can return any inventory which doesnt sell, back to the brand,right?

Secondly, how I see Ethos is that its a multi-year theme playing out. I know retailers in general command premium when it comes to PE but with the recent run up it seems to have become quite expensive. What are your thoughts on this? and how would you describe your Exit strategy for your pf?

(PS: Beginner here trying to gather perspectives and learn)

Gujarat Themis Biosyn Ltd – Bulk Drugs growth momentum (26-07-2024)

Company is working on almost full capacity therefore revenue degrowth has happened YoY.

It got benefitted with excess inventory in Q1FY24 which is not present at the moment.

Growth is likely to be slow until migration happens from A) current Rifa-intermediate product to Rifapentine which will free up some capacity (it will lead to same revenues at 50% capacity as prices for the products are high while product’s requirment is low) coupled with B) New capex to be commissioned in FY25 end most likely.

But until then, don’t expect any growth this FY (especially since last year got the benefit of higher margins & stack up of inventory which was ultimately sold despite business running at full capacity)