They may be crossing 3500 to 4000 Cr on consolidated basis in FY 25. As per management, they are eying more than that.

Posts in category Value Pickr

Kothari Petrochem Ltd~ A hidden moated small-cap company? (26-07-2024)

Kothari Petrochem AGM Notes~

- Sole manufacturer of PIB in India

- Domestic demand grew by 10-12% owing to changes in formulations & new applications of PIB

- Lubricant Industry is expected to grow despite EV

- Established presence in china,UAE among others

- Planning to establish stock points

- Newer chemicals in PIB side & forward integration plans

- Captive power plant operated 311 days with additional demand met by state power

- Solar panels of 244 KWH

- New facilities are being created

- Significant changes are going to be present in lube additives market ~ EV, synthetic lubes etc- PIB finds new applications in Battery coolants

- Conventional PIB is expected to be replaced by highly reactive in next 10 years in lube additives market

- Industry to grow at 4-6%

- Rohit Balakrishnan & keshav Garg is also present in the AGM

- TOtal market is 2Mn MTPA , Indian is 28,000 MTPA (1-2% )

- Low cost manufacturing, end market growth (from south east asia solely) & make in India initiatives is leading to value migration towards company’s product from lubes

- Local supplier preference + proximity will help snatching mkt share from western players in SOuth east

- Conventional PIB applications will continue even after transition to HR PIB happens

- Company has developed HR PIB- at a semi-commercial plant (3MTPA per day), primarily to understand issues before scaled up to a larger plants

- Will take approvals from customers before doing any capex

- HR PIB demand growth will be higher than C PIB (conventional)- customers will be same+market is highly consolidated with 2-3 players

- Auto-lubricants & fuels hold only 45% of portfolio, sealants & adhesives contributed 45% & remaining from rubber etc

- Expects application from Rubber market to increase significantly

- “Unwise to expand without access to feedstock”~ feedstock is scare either on quality or quantity

- Company uses high quality feedstock leading to an edge

- Capex plans in ideation stage at the moment

- Legal etc costs saw abnormal increase to hire people for research work

- R&D front focus- new applications of PIB & new molecule discovery (HR-PIB)

- PIB is a carrier to carry engine oil in vehicle-which includes adhesives, etc & work on applications & work backwards

- Principal on Capex- full benefit within 3 years

- Tax rates will reduce in the coming year

- PCPB is asking for change in fuel from existing fuel to natural gas which will potentially decrease margins (trying to pass on to some extent)

- Working on optimization to reduce packing & transportation

- Doesn’t see a drop in the market in next 15-20 years

- Consultants work with the company to foresee demand going forward

- Looking at debottlenecking exercise in existing plants (already done the activity in FY24)

- Problem towards expansion is the scarcity of raw material

Investing Basics – Feel free to ask the most basic questions (26-07-2024)

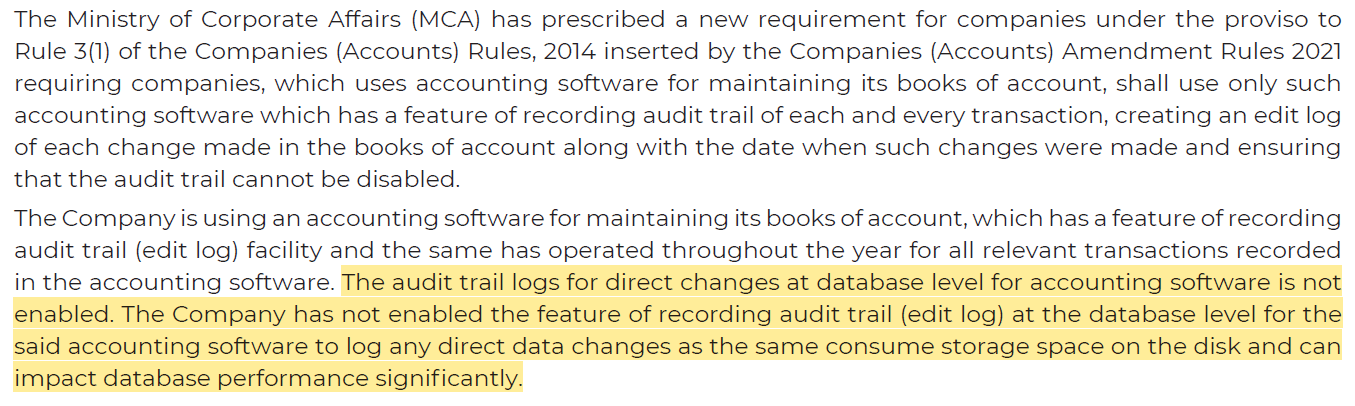

A company has made the following disclosure in its Annual Report

Since there are a lot of techies active here on ValuePickr, can someone comment on the legitimacy of this practice? Are these stated drawbacks really so severe as to disable the audit logs for database updates? What is the normal practice in the industry?

Kriti Industries (India) Ltd (26-07-2024)

Purchase by promoters continues

More warrants announced today ~95 lakhs to promotors ( to be finalized on 27.7.24) >https://www.bseindia.com/xml-data/corpfiling/AttachLive/402eeb73-d9d4-4797-83e2-72c4a93f8d23.pdf

D- holding, added few today.

Talbros Automotive Components Limited (TACL) (26-07-2024)

why they haven’t added subsidiaries numbers in consolidated statements? FY24 topline (773 cr – Gasket + forging) TACL standalone in PPT

Manappuram Finance (26-07-2024)

An employee in manappuram finance taken out 20cr illegal loan

P.E. Analytics Ltd (PROPEQUITY) – Another Data Analytics Platform for Real Estate Players (26-07-2024)

Promoter sold ~2% of shares in 2 days in bulk deal:

Hitachi Energy – A Century old MNC in a new bottle! (26-07-2024)

Q1FY25 Concall Summary

Business Updates

- The order backlog as on end of the quarter was at Rs 8539 crores which is highest since inception of the company

- The new greenfield plant at Chennai has received orders not just from India but from other parts of the world

Participants

Goldman Sachs

HDFC Securities

LIC Mutual Fund

PL Capital

Birla Mutual Fund

UBS

Jupiter Financial

QnA

- At end of FY25 the EBITDA margins will get into double digits

- There is a lot of bidding activity in the transmission space and due to the elections ongoing there were delays but it will accelerate going forward

- The first priority is to serve the domestic market, as there is tremendous demand in the country. The management is keeping provisions to cater to demand in the world as well

- The company initially had 10% of sales from exports which has now gone around 30% of revenues without even taking large scale orders from abroad

- One of the largest producers of medium voltage transformers in India and also the world with decent market share in the country

- Globally the parent will be investing $1.5 billion to enhance the capacity of transformers and in India the company has added capacity with new greenfield expansion

- The project in Australia that was announced was from the factory in Chennai and demand is coming from all across the world

- Going forward India can become a manufacturing hub for transformers to the world as there are enough resources to do the same

- In terms of exports already gone above 25% of revenues and trending upwards from there as well towards 30%

Axis bank – Turnaround imminent (26-07-2024)

notes from FINANCIAL RESULTS FOR THE QUARTER ENDED 30th JUNE 2024

Q1FY25 core operating profit of 9,637 crores up 16% YOY,3% QOQ , NIM at 4.05%, cost growth moderating, aided by steady growth in average deposits and advances

• Net Interest Income grew 12% YOY and 3% QOQ

• Fee income grew 16% YOY, Retail fee grew 18% YOY, granular fees at 93% of total fees

•Operating cost growth moderated to 11% YOY and declined sequentially, PAT at 6,035 crores up 4% YOY

•On a QAB, total deposits grew 14% | 3%, term deposits grew 21% | 4%, CASA grew 4%| 3% on YOY | QOQ basis, respectively

•Total advances grew 14% YOY, Retail loans grew 18% YOY, SME grew 20% YOY, Corporate loans grew 6% YOY

•Overall CAR stood at 16.65% with CET 1 ratio of 14.06%, net accretion to CET-1 of 32 bps in Q1FY25

•GNPA% at 1.54% declined by 42 bps YOY, NNPA% at 0.34% declined by 7 bps YOY

MEB deposits grew 13% YOY; CASA ratio at 42%, which is amongst the best for peer private banks

•On MEB basis, term deposits grew 20% YOY, CA grew 12% YOY, SA flat YOY

o Average LCR during Q1FY25 was ~120%, outflow rates improved ~ 400 bps over last 2 years

o ~1 million credit cards issued in Q1, CIF market share4 of ~14%, card spends up ~12% YOY

o Largest player in Merchant Acquiring with market share of 21%, incremental share of 45% in last one year4

o Citi integration completed successfully in July 2024

o Credit card CIF market share at 14%, Retail Card spends grew 14% YOY

o Asset quality stable, credit cost higher due to seasonality and lower recoveries and upgrades, not indicative of full year credit costs

o PCR healthy at 78%; On an aggregated basis5, Coverage ratio at 150%

o Gross slippage ratio at 1.97%, Net slippage ratio at 1.37%

o Q1FY25 net credit cost at 0.97%

Key domestic subsidiaries continue to deliver steady performance

o Q1FY25 profit at 436 crores up 47% YOY, with a return on investment in domestic subsidiaries of 54%

o Axis Finance Q1FY25 PAT grew 26% YOY to 154 crores; asset quality metrics improve, ROE at 14.7%

o Axis AMC Q1FY25 PAT grew 27%YOY to 116 crore,

o Axis Securities Q1FY25 PAT grew 171% YOY to 121 crores

o Axis Capital Q1FY25 PAT grew 220% YOY to 49 crores and executed 22 investment banking deals in Q1FY25

Core Operating Profit and Net Profit

The Bank’s core operating profit for the quarter grew 16% YOY to 9,637 crores. Operating profit grew 15% YOY to 10,106 crores. Net profit stood at 6,035 crores in Q1FY25 as compared to 5,797 crores in Q1FY24, and grew 4% YOY.

Net Interest Income and Net Interest Margin

The Bank’s Net Interest Income (NII) grew 12% YOY and 3% QOQ to 13,448 crores. Net interest margin (NIM) for Q1FY25 stood at 4.05%.

Other Income

Fee income for Q1FY25 grew 16% YOY to 5,204 crores. Retail fees grew 18% YOY; and constituted 71% of the Bank’s total fee income. Retail cards and payments fee grew 12% YOY. Retail Assets (excluding cards and payments) fee grew 13% YOY. Fees from Third Party Products grew 68% YOY. The Corporate & Commercial banking fees together grew 12% YOY and 1% QOQ to 1,497 crores. The trading income gain for the quarter stood at 406 crores; miscellaneous income in Q1FY25 stood at 173 crores. Overall, non-interest income (comprising of fee, trading and miscellaneous income) for Q1FY25 grew 14% YOY to 5,783 crores.

Provisions and contingencies

Provision and contingencies for Q1FY25 stood at 2,039 crores. Specific loan loss provisions for Q1FY25 stood at 2,551 crores. The Bank holds cumulative provisions (standard + additional other than NPA) of 11,732 crores at the end of Q1FY25. It is pertinent to note that this is over and above the NPA provisioning included in our PCR calculations. These cumulative provisions translate to a standard asset coverage of 1.20% as on 30th June, 2024. On an aggregated basis, provision coverage ratio (including specific + standard + additional) stands at 150% of GNPA as on 30th June, 2024. Credit cost (annualized) for the quarter ended 30th June, 2024 stood at 0.97%.

Balance Sheet: As on 30th June 2024

Balance Sheet: As on 30th June 2024 The Bank’s balance sheet grew 13% YOY and stood at 14,68,163 crores as on 30th June 2024. The total deposits grew 13% YOY on month end basis, of which current account deposits grew 12% YOY; total term deposits grew 20% YOY and 1% QOQ. *+The share of CASA deposits in total deposits stood at 42%**. On QAB basis, total deposits grew 14% YOY and 3% QOQ, within which

savings account deposits grew 3% YOY and 3% QOQ,

current account deposits grew 8% YOY and 2% QOQ;

and total term deposits grew 21% YOY and 4% QOQ.

The Bank’s advances grew 14% YOY and 2% QOQ to 9,80,092 crores as on 30th June 2024.

Gross of transfers through Inter Bank Participation Certificates (IBPC), total Bank advances grew 15% YOY and 1% QOQ. Retail loans grew 18% YOY to 5,85,112 crores and accounted for 60% of the net advances of the Bank.

The share of secured retail loans was ~ 71%, with home loans comprising 28% of the retail book. Home loans grew 6% YOY, Personal loans grew 29% YOY, Credit card advances grew 22% YOY, Small Business Banking (SBB) grew 26% YOY and 2% QOQ; and rural loan portfolio grew 24% YOY. SME book remains well diversified across geographies and sectors, grew 20% YOY to 1,04,016 crores.

Corporate loan book (gross of IBPC sold) grew 10% YOY;

domestic corporate book grew 7% YOY and 4% QOQ.

Mid-corporate book grew 24% YOY and 2% QOQ.

89% of corporate book is now rated A- and above with 89% of incremental sanctions in Q1FY25 being to corporates rated A- and above. The book value of the Bank’s investments portfolio as on 30th June 2024, was 3,16,851 crores, of which 2,47,795 crores were in government securities, while 56,384 crores were invested in corporate bonds and 12,672 crores in other securities such as equities, mutual funds, etc. Out of these, 67% are in Held till Maturity (HTM) category, 12% of investments are Available for Sale (AFS), 19% are in Fair Value through Profit & Loss (FVTPL) category and 2% are investments in Subsidiaries and Associate. **Asset Quality** As on 30th June, 2024 the Bank’s reported Gross NPA and Net NPA levels were 1.54% and 0.34% respectively as against 1.43% and 0.31% as on 31st March, 2024. Recoveries from written off accounts for the quarter was 591 crores. Reported net slippages in the quarter adjusted for recoveries from written off pool was 2,700 crores, of which retail was 2,456 crores, CBG was 13 crores and Wholesale was 231 crores. Gross slippages during the quarter were 4,793 crores, compared to 3,471 crores in Q4FY24 and 3,990 crores in Q1FY24. Recoveries and upgrades from NPAs during the quarter were 1,503 crores. The Bank in the quarter wrote off NPAs aggregating 2,206 crores.

As on 30th June, 2024, the Bank’s provision coverage, as a proportion of Gross NPAs stood at 78%, as compared to 80% as at 30th June, 2023 and 79% as at 31st March, 2024.

Disc – tracking