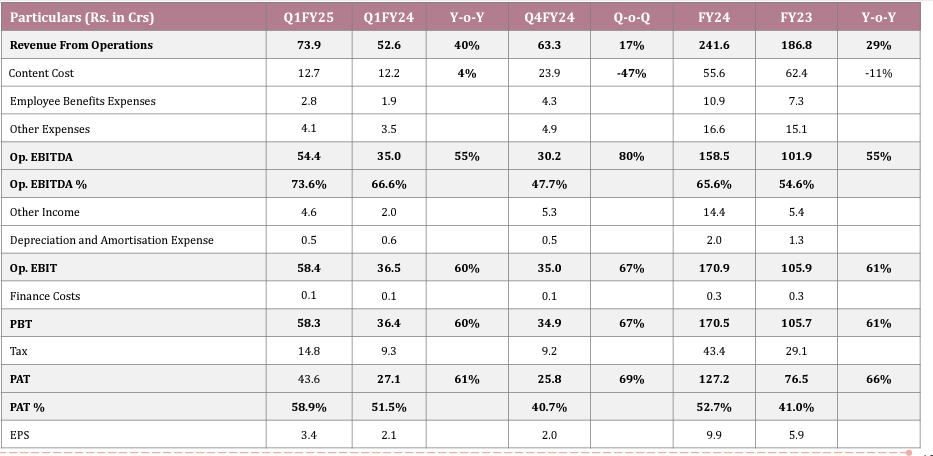

Another superb quarter

Disclosure: Invested

Another superb quarter

Disclosure: Invested

Anyone invested in KNR construction.is it a good company for long term

Couple of interesting snippets from the transcript:

Operating leverage and the scope for margin expansion:

“

So, only one question I have, so the margins have really improved the EBITDA margin, is it

something that is sustainable in future quarters or in upcoming years?

Tarun Dua: Ours is a platform business so, the overall team size, the platform size doesn’t need to really

increase with the amount of cloud business that we do. So, we can potentially scale up the

business 10x where the platform remains practically the same in terms of the size of the dev

team and the size of the operations team, it needs to grow very organically compared to,

whatever the growth on the side of the content revenue. So that way, there is always any

platform business, the scope for growth of margins is always there

“

On what they perceive as their USP:

“

Aman: My question is, what is our USP over the, if we are in a competition with the largest player or

an emerging domestic player, somewhere what we see the competition that makes us different

from the competitor, which is infrastructure heavy player and what add on’s we provide in

terms of cloud services to our clients?

Tarun Dua: So there is a long list of cloud services that we have been providing from last many years. And

typically, what happens with software usage is that software usage is a habits, so whether it’s

a larger player with like a bigger piece of software, whether it is like a player which is more

infra heavy, less software, ultimately the differentiator would become the stickiness of the

software that we eventually produced, with the help of like understanding from our customers,

that we build from our customers. So ultimately the differentiator is going to be the software

platform that we are building.

Aman: So are you trying to convince me that we are.

Tarun Dua: I am not trying to convince you of anything.

Aman: No, are we at better.

*Tarun Dua: I only want to convince our customers to use our product, I don’t need to convince anyone *

else.

“

Management sees Op margins over the medium term to be around 60%:

“

Pankaj Kumar: Okay. So, can we say that we have moved from +50 percent kind of margin to +60 percent kind

of margins, is that a reasonable estimate or reasonable understanding?

Tarun Dua: I already answered this question, in the medium term and the long term the trend should

sustain.

“

Key Highlights:

Segment Performance:

Outlook:

Other Points:

Key Points:

Other Call Highlights:

Inorganic Growth:

Overall, the call portrayed a positive outlook for LTTS with strong growth prospects and a clear M&A strategy. L&T Technology Services is focused on growth and is making investments to achieve its goals. They are confident that their revenue and margins will improve in the coming quarters.

Follow me on X for many other company updates: x.com

Newgen Software Technologies Limited Q1 FY 25 Analyst Conference Call:

Revenue growth: Newgen reported strong revenue growth of 25% Y-o-Y for Q1 FY 25. This growth was driven by good business growth across all regions, with EMEA, India, and APAC showing growth.

Seasonality: Historically, Newgen’s business has been seasonal, with Q1 being the leanest quarter. However, the impact of seasonality is slowly reducing.

New client additions: Newgen added 13 new logos in Q1, indicating strong customer acquisition.

Upselling and cross-selling: Upselling and cross-selling to existing customers are significant contributors to revenue growth.

Product innovation: Newgen launched a new product, Newgen LumYn, an AI-powered hyper-personalization platform designed for the banking sector.

Profitability: Newgen delivered healthy growth in profits and expanded margins. Profit after tax was at INR48 crores for the quarter, witnessing a growth of 58% Y-o-Y.

Global expansion: Newgen is focusing on increasing its global reach, especially in mature markets like the US and Europe. They partnered with Finastra to offer better banking solutions and expand their market base.

Investments: Newgen is continuing to invest in R&D and sales and marketing initiatives to support future growth.

Employee growth: Newgen has been hiring aggressively to support its growth plans. They hired around 500 campus recruits in Q1 and are also doing some lateral hiring.

Product Offerings: Newgen is focusing on expanding its horizontal product offerings (NewgenONE, LumYn, Marvin) which cater to broader functionalities. They are also expanding their vertical offerings to include areas like Trade Finance, Supply Chain Finance, and Insurance.

Sales Strategy: The GTM strategy is primarily verticalized, with sales teams focused on named accounts in Banking, Insurance, Financial Services, and Government. Horizontal product sales are driven through partnerships and inbound leads.

Impact of New Products: The newly launched LumYn and Marvin are expected to contribute to the top line and bottom line in the long term (3-4 years) as the sales funnel matures. They are not expected to have a significant impact in the near future.

In addition, the company clarified that ESOPs are granted to a broad base of employees and the financial impact is not expected to be significant.

Overall, the transcript paints a positive picture of Newgen’s financial performance and future prospects. The company is experiencing strong revenue growth, expanding its margins, and investing in new products and global expansion.

Follow me on X for many other company updates: x.com

Technical View: BCC Fuba

Price breaking out on a weekly and daily chart with High Volume after 10 months of consolidation.

Daily chart breakout after the budget announcement with Highest Volume of the Year

There was some increase in the customs duty (BCD) from 10 to 15 percent on PCBA of specified telecom equipment.

However, PCB is chosen based on the specific requirements of the telecom equipment, such as durability, heat resistance, and signal integrity.

Mutilayer PCBs are one of them and Bcc Fuba is a manufacturer of the same.

It’s my guess based on the budget announcement and positive reaction by the stocks, I may be wrong altogether.

Disc: Have a position based on technical, will close the trade if it falls below the resistance level marked.

guys any latest update or information regarding stock? long term view? pls guide

A good read on medplus

Hi @vikas_sinha What do you think about All E Technologies. Their revenue projections are looking very good to me.

Highlights:

Key Questions and Answers:

Additional Notes:

The company stopped disclosing individual product volume breakdown due to competitive reasons.

Pledges on promoter holdings have been released.

The debottlenecking project is different from the brownfield expansion project. The basic engineering study for the latter is still ongoing.

Realization increase is mainly due to product mix changes. The company also sells SAN and polystyrene at lower costs compared to ABS.

Capacity Utilization: Styrene Performance Materials is operating at near full capacity for ABS and Polystyrene. Debottlenecking projects are underway to increase capacity.

ABS Spreads: There is disagreement between the company and a caller on ABS spreads. The company claims spreads haven’t changed in the last two years, while the caller argues they have increased 30-40%.

CAPEX: The company plans a total CAPEX of Rs. 650 crores over the next few years to nearly double ABS capacity and increase Polystyrene capacity by 50%. They will provide more details on the spending timeline in the next few months.

Debottlenecking: Debottlenecking is expected to increase ABS capacity to 100-105,000 tonnes by the end of the current quarter. The company is aiming to complete debottlenecking for Polystyrene in the next quarter.

Other Expenses: The benefit seen in other expenses in Q1 is expected to be sustainable, with some variations due to product mix and seasonality.

New Products: The company has launched new products under the brand names STYROLOY and ASALAC. ASALAC uses a specialized ASA rubber along with SAN and AMSAN. They have received some validations and small commercial orders but expect bigger benefits later in the year.

Stake Sale: The recent stake sale by the promoter was to retire debt taken for acquiring the company’s shares.

Revenue Distribution: ABS revenue comes from Automotive (40%), Household Appliances (40%), and other industries. Polystyrene revenue comes from Household Appliances (40%), Packaging (40%), and other industries.

Impact of Management Change: The new management has implemented changes to improve product efficiency, projects, and customer relationships, focusing on growth.

Freight Costs: The recent increase in ocean freight costs is not reflected in Q1 results but may be seen in Q2.

Power and Fuel Costs: The company is implementing projects to use alternate fuel sources, which will reduce costs significantly. The benefit will be seen incrementally from Q2 onwards and fully realized next year.

Overall, the company is experiencing volume growth and stable margins. New product launches and cost-saving initiatives are positive signs for future performance.

Follow me on X for many other company updates: x.com