Well written summary of the con call. Thanks!

Posts in category Value Pickr

Aarti Pharma Labs (22-07-2024)

Hello,

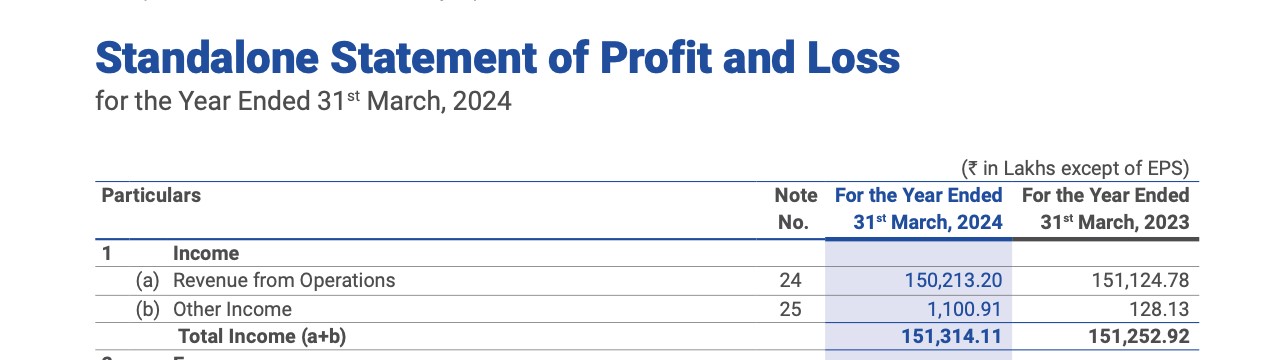

(Numbers in Lakhs)

-

Company reported almost 8x increase in other income in standalone P&L i.e 120 (2023) to 1100 (2024) (in Lakhs)

as dividend income

-

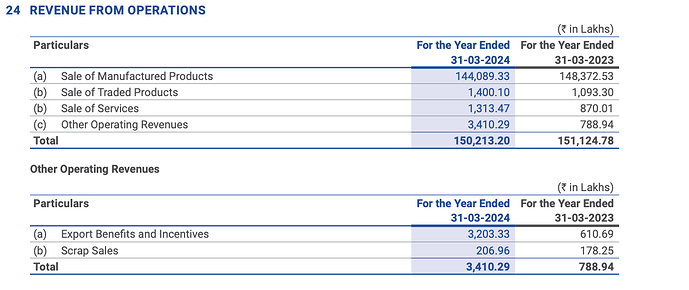

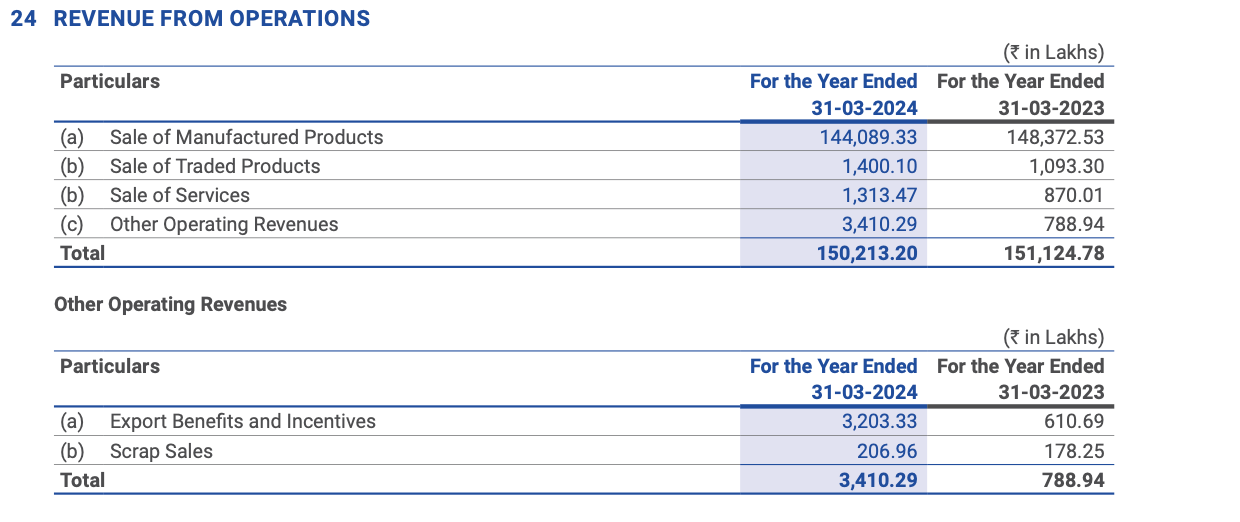

Export incentive benefit of 3200

-

Company added vehicles worth 200 Lakhs

396 to 585 (in Lakhs) -

Recently added R&D products under intangible assets worth 1800 Lakhs

-

Almost 10000 in CWIP

-

Interesting holding by the company – (Dilesh Roadlines Private Limited 464,550 1,239.40)

-

Company is stocking raw materials, 1128 (2024) from 132 (2023)

-

Anushakti Enterprise Private Limited holds 3.28% of the company, (Could not get any info on this)

-

25% increase in director renumerations, fairly higher than PAT growth

-

Xanthine capacity increase proposed from 5,000 to 9,000 MTPA through brownfield expansion and debottlenecking projects.

Disclosure: Not a buy/sell recommendation

Shakti Pumps – solar shakti (power)! (22-07-2024)

My KTAs from today’s Q1FY25 earnings concall:

-

Ajmer Comp C pilot project should get over in next 2 quarters. It will help all stakeholders to learn from this pilot project and move forward with expanding it to the wider audience.

-

Ajmer project includes solarization of 200-250 feeder pumps. So their capability is good for both Individual Pump Solarization and Feeder Level Solarization.

-

Shakti Pumps seems to be having an edge in Comp C through their patent. Their technology allows the system to transfer solar energy (electricity) to the grid automatically post pump has been used to draw the water. Where as, according to the management, for competitor’s grid connected solar pump, a human has to go and flip the switch to start the transfer of solar energy (electricity) to the grid. This can be a strong competitive advantage for farmers to choose only Shakti Pumps for their Comp C investment.

-

Tendering process for fixing solar pump prices are completed with 5 more quarters to go before next round of tender bidding starts for next leg of Comp B. So there is good chance that windfall margins might continue for next few quarters if solar panel prices remain subdued. There is good chance that to bid competitively, management might bid at lower prices and effectively we should see 16-17% kind of EBITDA from H2 of FY26.

-

New capacity to go live from FY27.

-

One thing which I am not able to digest is that management has guided 30% growth in FY25. So that means about 1800cr topline. Management has already guided for 500cr in Q2. Bringing total to 1070cr for H1FY25. This leaves about 360cr in Q3 and Q4 which would be very poor Q3 and Q4 given current strong tailwinds in Kusum scheme. Either management is being super conservative or there is something that management is hiding from investors.

Disc: invested with no transactions in last 30 days.

Sterling & Wilson Solar Ltd. – Will the Sun Keep Shining? (22-07-2024)

Company profile: The company provides EPC and O&M services under turnkey EPC and BoS solutions for utility-scale, rooftop, and floating solar power projects. It also offers solar plus storage solutions. It boasts an EPC portfolio of 19.4 GWp and an O&M portfolio of 8.2 GWp. It has a presence across 28 countries.

a) Q1 FY25 results: The company’s Q1 FY25 revenues stood at Rs 915 crores, up 78% YoY, whereas gross margins stood at 11.1% versus 11.3% YoY. EBITDA stood at Rs 37 crore versus a loss of Rs 34 crore YoY. PAT stood at Rs 5 crore versus a loss of Rs 95 crore YoY. This was the second consecutive quarter where the company posted a positive EBITDA, PBT, and PAT on a consolidated basis. On a QoQ basis, revenue declined 22% due to tighter liquidity conditions and the fact that Q4 is the strongest quarter of the year.

B) Orderbook and order inflows: The company’s order inflows for Q1 FY25 stood at Rs 2,170 crore versus Rs 488 crore in Q4 FY24. The company’s unexecuted order book as of Q1 FY25 stood at Rs 9,396 crore (70% is domestic and 30% is exports) versus Rs 8,084 crore as of Q4 FY24. The company has also commenced a pilot project for solar plus BESS for Reliance Industries at Jamnagar, Gujarat.

C) Debt Status: The company’s net borrowings have declined by Rs 19 crore and the total net debt as of Q1 FY25 stood at Rs 97 crore. Net working capital continues to be negative at Rs 732 crore as of Q1 FY25. Also, the company has no scheduled debt repayments till Q3 FY25. Also, on a net basis, the company will receive about Rs 85-90 crore in indemnity claims from the promoters which will largely take care of the debt repayments in FY25. The balance debt of Rs 328 crore post November 2024 will be paid in installments commencing from December 2024 to October 2026.

D) Outlook for FY25: The following is the outlook provided by the management for FY25:

-

The management has provided a revenue guidance for FY25 at Rs 8,000 crores. It has been reiterated that revenues will start inching up from Q2 onwards with the majority of it being earned in H2 FY25. For context, FY24 revenues were Rs 3,035 crore.

-

It has also provided an order inflow guidance of Rs 8,000 crore (excluding the Nigeria & RIL orders) for FY25. Domestic ordering activity is expected to pick up from Q2 FY25 onwards as Q1 was muted. In terms of bid pipeline, the company is actively pursuing projects worth 23 GW in India and 5 GW in other geographies.

-

Also, low module prices globally make the time ripe for more projects to come onstream.

-

Margin profile for both domestic and international projects largely remain in the range of 10-11% as major international legacy projects are now behind. EBITDA margins are also expected to recover to 4-5% in the medium term due to better absorption of fixed costs with the increase in scale of operations.

-

With respect to the Nigeria MoU (961 MWp along with BESS capacity of 455 MWh, approx. value Rs 12,483 crore), the company expects it to get finalized very soon as the final terms have been negotiated and procedural steps are in progress. Also, there is no risk from regime change in the US as the project is already an approved one in their list.

-

The Reliance pilot project will be completed in FY25 itself. Many new technologies are being tested which would set the base for larger projects with RIL. Also, with respect to the land allocated to RIL at Khavda, Gujarat, the company expects to receive orders soon.

-

Also, the company is making efforts for a credit rating upgrade which will ease the liquidity for the company and increase the fund-based and non-fund-based limits.

-

The company is taking orders on a BoS basis along with the modules. However, it is extremely cautious with respect to the module price risk. It has onboarded multiple vendors for supply of modules.

E) Some key risks: Here are some key risks found in the company:

-

The management has repeatedly emphasized that order inflows could remain lumpy.

-

During the quarter, promoters sold stake in minimal quantities. Also, 37.2% of the promoter holding remains pledged.

-

Arbitrations are going on for certain projects in the US, on which the company will inform stakeholders on any material developments. This is with respect to invocation of bank guarantees worth Rs 400 crores.

-

Nigeria order was to be finalized in Q1 FY25 but has witnessed a delay. This remains a key monitorable.strong text

BLUE PEBBLE- The next high growth SME? (22-07-2024)

@VibhavB How do you plan an office visit? Do companies allow investors to meet, I always thought you should be a large player to meet the company for investing.

Angel One: Metamorphosis into a Fintech? (Previously Angel Broking) (22-07-2024)

I am in a similar boat. The average price is 5% higher than the current market price. The current valuation looks really attractive, I am waiting for the budget tomorrow and next quarter’s results.

Its transition to AMC will bring stability, they have also started giving loans and planning to add more financial products in their suite. It looks like a very attractive company for long run with a business model that is here to stay.

Disclosure: Biased and invested

Bulk Deals Bi-Weekly Log (22-07-2024)

Bulk Deals Daily Log

13th Bulk Deals Log

Date: 22/07/2024

NSE Link: https://www.nseindia.com/report-detail/display-bulk-and-block-deals

BSE Link: BSE Equity : Bulk Deals

- Can Fin Homes

This stock saw buying from SBI Life Insurance Company. The budget might see some more incentives to first time homebuyers and that is why this company might be in focus.

Investor who bought: SBI Life Insurance Company

Quantity Purchased: 10 Lakh Shares

Share Price: 827.94

- Effwa Infra and Research

This company is an SME which is in the water pollution reduction domain. It has a fantastic return profile which seems to be too good to be true. Promoters also sold 43 Crs as offer for sale for a company who’s market cap even today is only 430 Crores. Several reasons to be skeptical of this story, but the fact that Multiplier stock and advisors are the buyers here is a very interesting development for the company.

Investor who bought: Multiplier Share and Stock Advisors

Quantity Purchased: 1.98 Lakh shares

Price: 208.6

- Ganesh Green Bharat

This company is another one that Multiplier Shares has bought which again seems to be in an interesting domain. It is in the Water Supply and renewable energy business. Definitely worth a look.

Investor who bought: Multiplier Stock Advisors

Quantity Purchased: 2.72 Lakh Shares

Price: 437.65

- Latteyes Industries Ltd

This company is in the pump space. The stock has seen a significant correction in the past one year and promoter selling too, but Mansi Share and Stock Advisors is a credible name, perhaps it might help to look into this story.

Investor who bought: Mansi Share and Stock Advisors

Quantity Purchased: 2.97 Lakh Shares

Price: 20.27

- Sati Polyplast

Another SME company that saw investor interest, however there is very little data, maybe this might be a listing that happened today.

Investors who bought: Mansi Share and Stock Advisors, Multiplier Stock Advisors

Interest from Quant Trading Funds:

- Apex Frozen Food

- Anthony Waste Handling

- BCL Industries

- MTNL

- Navkar Corporation

- National Fertilisers

- Nitin Spinners

Banswara Syntex – Deleveraging, Changing Product Mix, Proxy to Fast Fashion (22-07-2024)

Anyone still tracking this? Since textile sector is gaining momentum, this looks interesting. Business has bottomed out in FY24 and it has capacity utilisation to do around Rs 2000 crs in revenue.

BLUE PEBBLE- The next high growth SME? (22-07-2024)

Interesting. Where did you find the Auditors fees mentioned?

Planning on writing a mail to them in case this arises as a concern.

Also, I might visit to their office in case they allow. Would love to see their set up and meet the team which has produced some genuinely high quality work.