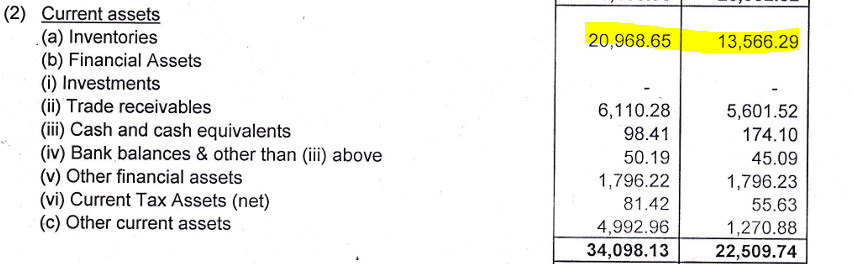

While the bottom-line looks decent YoY. The company is either loosing market share, or the demand has not picked up. Could there by any other reason for spike in inventory? (numbers are Mar 2024 vs Sep 2024)

While the bottom-line looks decent YoY. The company is either loosing market share, or the demand has not picked up. Could there by any other reason for spike in inventory? (numbers are Mar 2024 vs Sep 2024)

Added by a renowned PMS

Read for thesis pls

I dont think there are any tools that do that.

.

You can DM me the excel file.

ValueResearch and Moneycontrol is what I use to track the portfolio. Both of them provide the market cap stat which Zerodha is giving you issue with.

RPG Lifesciences –

Q2 FY 25 results and concall highlights –

Revenues – 172 vs 153 cr, up 12 pc

EBITDA – 48 vs 39 cr, up 22 pc ( margins @ 27.8 vs 25.5 pc ) – highest ever EBITDA margins

PAT – 31 vs 26 cr, up 19 pc ( this is adjusted PAT – not accounting for 27 cr of transfer charges as the same is going to be nullified in Q3/Q4 post completion of land sale deal )

Segment wise performance in H1 ( Q1 + Q2 ) –

Domestic formulation sales @ 216 vs 196 cr, up 10 pc YoY

International formulation sales @ 66 vs 56 cr, up 16 pc YoY

API sales @ 52 vs 46 cr, up 14 pc YoY

Domestic MR productivity @ Rs 6 lakh/month

H1 growth driven by 10 pc volume growth ( which is an extremely healthy number considering poor volume growth for IPM )

Company has sold its surplus land holdings located near Navi Mumbai for 144 cr

Actively looking for M&A opportunities in both formulations and API spaces in order to utilise the cash on books ( which post the land deal should rise to above 250 cr )

For domestic formulations business, the breakup of in-house : outsourced manufacturing stands @ 70:30

Currently 35 scientists are working in the company’s R&D center at Navi Mumbai. They intend to add a few more in near future. Currently working on expanding their Immuno-supressants portfolio so as to cement their position in this niche therapy area. Also working on a few molecules in the CNS and Cardio therapy areas. In all – working on 12 molecules

Going fwd – company intends to keep clocking gains on EBITDA margins. Although the gains hereafter should be gradual and not as steep as last 4-5 yrs

Wrt acquisition strategy for APIs – looking for small volumes, high complexity, niche molecules so as to avoid competition from bigger players. In the formulations space, looking to acquire brands in the chronic therapies

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

Yes, sometimes stepping away might seem like the right choice. I’ve tried it in the past, and my experience taught me that rejoining with the same conviction is often challenging. So, if the business has strong long-term prospects, stepping away could mean missing out on significant gains.

Regarding Trent’s results, they are exceptional—among the best in the industry, not just in retail. Other retail players have faced losses this quarter (V2, ABFR), and while DMart also saw a reduction in profit, Star Bazaar reported improved profitability. Emerging categories like beauty & personal care, innerwear, and footwear have continued to gain customer traction and now contribute to over 20% of revenues. Zudio Beauty, in particular, seems highly promising to me. Even in a challenging month like September, Trent delivered an impressive operational profit of ₹643 crore. I believe their consolidation of 25 stores is a strategic step, showing management’s careful and profitable approach to expansion.

Yes, the stock price action has been disappointing, but I remain confident. For me, it’s business as usual. For the past year, I’ve been searching for a third company to add to my concentrated portfolio, but I have yet to find one that convinces me. Currently, my portfolio includes only Trent and Divi’s Laboratories, and I’m still on the lookout for a third.

Disclaimer: I am invested in Trent and have added a few more units recently. This is not a buy/sell recommendation, nor should it be taken as investment advice—these are solely my personal views.

The Latest and last credit rating from ICRA, Summary of possible Risks and past events.

Numbers muted both QoQ and YoY

It won’t be proper to compare q2 of CAG with q1 of Arman to check the leverage. Arman did qip in Dec 23 and hence its leverage is understandably lower and Capital Adequacy higher.

Secondly, on >4 borrowers, all the MFI lenders and SFBs have burnt their fingers. Everyone seems to have been chasing growth at the cost of asset quality. If this is not ever greening of loans, then what is this? Irony is none of these players are new entrant in the sector. They all have credible mgmts with existence of >20 yrs, to say the least.

Thirdly, to the best of my knowledge, almost all of MFIs have reported q2 numbers except Satincare and Arman. Some mgmts are expecting worst will get over by q3 and growth to resume from q4 others like ujjivan are saying pain to continue for next 2 quarters. The q2 of equitas reported the same pain and 16% of their AUM (MF Loans) has eaten away the PAT, in credit cost. To me, it appears, this pain won’t settle in next 6 months, and may take longer to settle down and report growth.

Fourthly, it seems there are no formal system of assessment of income levels of these mf borrowers. So, there are left to best judgement and assessment of each of these MFI. Their underwriting skills will get tested this time again.

Lastly, on technicals, stocks of all MFIs and SFBs are in stage 4 decline though fundamentally all are trading below with long term averages.

Q2-2025(oct 2024) concall

1…Highest quarterly volume and export volume

2…NL(Overcapacity is problem)

=Significant increase in nitrile latex and gloves inventory due to overcapacity from COVID-era production.

=Current capacity utilization around 60%, with EBITDA margins slightly negative.

=Margins pressured by overcapacity in the global market and high inventory levels.

3…NBR(Dumping is problem)

=Anti-dumping duty case initiated by the government; expected findings in 8-12 months.

=Current high imports of NBR impacting margins; positive EBITDA achieved but not sustainable.

=Expansion plans on hold pending anti-dumping case results and market conditions.

=nbr@dumping by china and russia due yo their slowdown

4…Carpet and Paper Product Challenges:

=Increased capacity by competitors leading to margin pressure in the paper segment.

=Freight rates significantly impacted by geopolitical tensions, especially in routes affected by the Red Sea situation.

=Overall pressure on margins expected to persist into Q3.

5…SB latex

=Exports accounted for 32% of total sales; SB latex exports grew by approximately 16-17% in value.

=Competitive landscape primarily against European players for SB latex

6…Strategy

=our strategy has been very clear that we are going to push

through with volumes as far as possible, even at lower margins and as and when overall the

external scenarios change we will be benefited

=Management remains cautiously optimistic about long-term growth potential despite current challenges.

=Plans to invest in R&D and renewable energy

Disc…invested