But even in cable segment , the total sector has got very high PE Rating. If you do reverse DCF , I think, this may not be sustainable

Posts in category Value Pickr

Samhi Hotels – Turnaround with Tailwinds (18-07-2024)

Shares in Supply :

Lock-in of shares is also near March 21st 2025

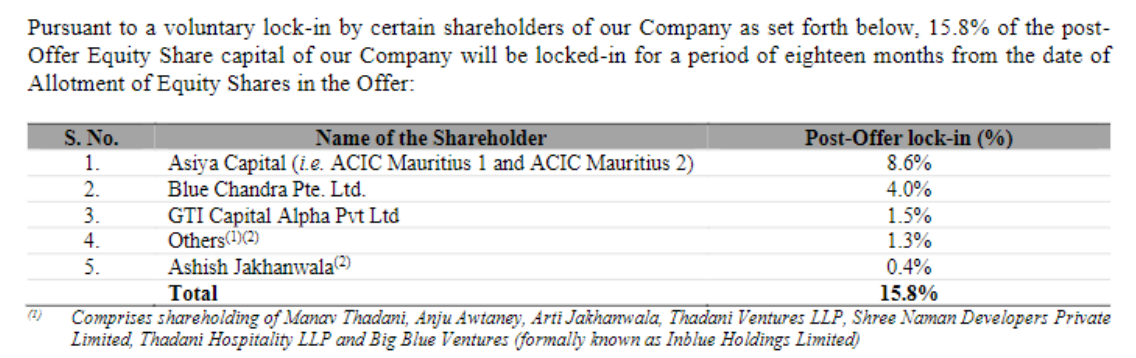

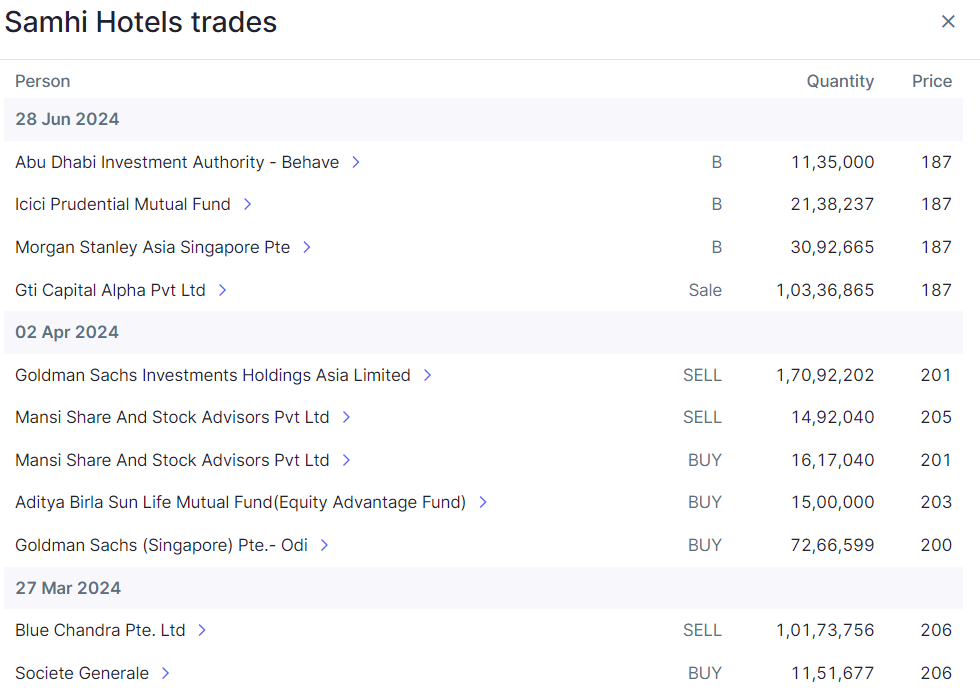

Actually only 15.8% of the shares o/s are locked in for a period of 18 months, i.e. till March 2025. Beyond this 15.8%, pre-IPO and anchor investors are free to sell and they have been selling through the last few months.

Blue Chandra and GTI Capital have in fact already sold down to their 18 month lock-in levels. So the selling overhang is not a March 2025 event, its already very much underway.

ACIC Portfolio: ( Good or Bad )

One of the bad side is they have diluted lot of equity,and got the land bank in Navi Mumbai and that’s written off ( 70cr )

The land issue was unfortunate but as Chinmaya pointed out I think the ACIC acquisition happened at a fair valuation. Not cheap (as you can imagine in the middle of a strong hotel upcycle), but fair, at around 13x EVEBITDA considering ACIC’s FY24 EBITDA nos. So I don’t think over-dilution happened.

Expansion Delay:

-. Samhi is having ongoing expansion of hotels which are not up in past 3 to 4 years ? Why it’s being delayed.

Caspia Pro Hotel , Bangalore expansion, Hyatt Regency etc…

Not sure if they have addressed this in the DRHP or the concalls, cannot recall. If I had to guess I would think it was due to a drag in free cash due to high debt and Covid. Hopefully these assets will be rebranded and functioning by H2 FY25 as management has guided.

Disc: Invested and biased.

ValuePickr- Mumbai (18-07-2024)

There is a whatsapp group.

Kirloskar Electric – A Turnaround Bet? (18-07-2024)

Second bulk deal today by Ajay Upadhyay ji.First one was at 158.

Wockhardt: an NiCE story (18-07-2024)

@parkhi_nazar – Appreciate the number-crunching man ![]()

Few things to keep in mind

-

I think royalty here is bound to be in the high teens on par with orphan drugs, first-in-class drugs (BLE acknowledgement and higher breakpoint point than Cefepime points in this direction) and highly specialised drugs with a small target market.

-

If drug is manufactured and marketed by another party, along with royalty there is generally a one-time upfront licensing fee which brings in substantial value, alongside the DCF from royalty

-

The market size of WCK-5222 may have gone up after the higher breakpoint since its understood now that its a lot safer to use without risk of resistance (relative). Though it might be early, we may have to compare market size of WCK-5222 with carbapenems ($4b in sales) instead of with Avycaz (already doing close to $1b in sales)

-

The way WCK-6777 (Ertapenem+Zidebactam) works is fairly similar with Zidebactam functioning as BLE and lowering the MIC of Ertapenem.

The MICs are so low even where Ertapenem is resistant.

You can see at what MIC 90% cumulative reduction in population happens for Ertapenem vs Ertapenem+Zidebactam (almost 2-3 dilutions lower!).

Zidebactam can give a new lease of life to lot of old beta-lactam antibiotics in combination as a BLE perhaps. So success of WCK-5222 has more riding on it than just its value. There’s a step-wise recalibration that can happen in expectation at that point of time in future where the money from WCK-5222 upfront licensing fee can help with taking the rest of the drugs through trials and unlocking further value. The balance sheet once it gets deleveraged can make this look like a completely different business once cash flows start.

Again, these are at least a year or 2 in the future, so a lot can change and all of it hinge on WCK-5222’s success, so its like building castles in the air talking more about it at this point prematurely. But WCK-5222 is not the only thing that can affect valuation once its approved is the limited point.

Disc: Invested. No recent transactions

Screener.in: The destination for Intelligent Screening & Reporting in India (18-07-2024)

Hey @kowshick_kk are the projections (expected sales growth, sales, etc) proprietary to Screener or do you source this estimates data from elsewhere?

Tejas Networks – Product based IT business in a favored sector? (18-07-2024)

Tejas AGM video. They plan completing the TCS/BSNL order this fiscal year. They might also get a reasonable order out of Rs 65000 crore BharatNet phase-3 tender, and US Rip and Replace program will definitely benefit companies like Tejas.

KEI Industries Ltd – A consistent performer over the last decade (18-07-2024)

The summary of my point is that in the context of their outlook and the lack of companies that come with such clean managements in the Industrials space in India the severe derating that you are waiting for might be less likely unless something fundamentally changes about this company

KEI Industries Ltd – A consistent performer over the last decade (18-07-2024)

Hi, I am not sure if I understand your pov. Can you please elaborate?