I’ve a novice question regarding their furniture business. Is there re-usability of the furniture they make? For example, a customer contract get over, so do they retire the current set of furniture and deploy new one or they continue using the old ones (the former feels more like the answer).

With their furniture business, a lot of depreciation cost will come up if I’m not wrong. Do we have any estimate on what kind of life are they deciding for the furniture items?

Posts in category Value Pickr

EFC – Entrepreneurial Facilitation Centre (14-07-2024)

Aavas Financiers :: Banking on the unbanked (14-07-2024)

If the interest expenses on borrowed funds is high, it might compress the NIM if the increase in interest income is not proportionate to the increase in interest expense. So need to understand where the new funds are going to be deployed into. If it is for high-yielding loans, NIMs can improve also.

INOX Wind (14-07-2024)

The long-term aim is make Inox GFL renewable arm a $10Billion company(i think it might includes unlisted companies also) as they see huge order visibility and sector tailwinds. Devansh Jain

InoxGfl Group: Co Bags New Turbine Order, How Will Firm Reduce The Debt For Future Growth? | ET Now

Aavas Financiers :: Banking on the unbanked (14-07-2024)

In the latest Credit rating by ICRA, they mentioned the following

Going forward, the NIMs are likely to be under some pressure on account of the higher gearing.

Can someone please explain why NIMs is related to gearing?

From my understanding, gearing is the debt that the company can take, which implies that they can take more debt (according to the statement), which means that either the ROA reduces or they can give out more loans as they’ve more leverage.

How does NIMs come into the picture? Is it because of the ROI at which the new gearing have been given to the company?

Thanks

REPCO home finance (14-07-2024)

This does look like it is trading cheaply at 0.9 * Book value but some of the key monitorables and triggers to track could be:

Growth guidance – They missed the guidance of Rs 14,000-crore loan book by FY24. Management expects AUM to reach Rs 20,000 crore by FY27. So they need atleast a CAGR of 14-15% over the next three years.

Expansion – New branch addition in Tier 2 and 3 towns of Tamil Nadu as planned and also expand its presence in non-core states.

NIMS – NIMs improved to 5.2 percent in FY24 despite the higher cost of funds. Maintain this pricing power

NPAs – Asset quality must continue to improve (especially non-salaried segment). On the right track since FY22 but needs to keep it that way.

Credit Cost – Keep the incremental credit cost low in FY25 to boost earnings

ROA – Maintain atleast its current ROA of 3%

Policy impact – Govt’s rural focus, potential higher allocation under the PMAY-Gramin scheme (Pradhan Mantri Aawas Yojna) and impending rate cuts – will all be positive triggers

Azad Engineering – A stock picker’s dream! (14-07-2024)

seems to be a wonderful business but in terms of valuations and some numbers situation doesn’t seem to be very good right now.

Ugro Capital – Opportunity To Invest in a Fintech-like Company Below Book Value (14-07-2024)

Both businesses are different. One is B2B lender (MSME) and 2nd one is a retail lender.

Natco Pharma: Focusing On Complex Products (14-07-2024)

Hi folks, new to investing and recently started to analyze pharma sector and this company, what I have learned is: this company has built a strong position in the value chain. It is expanding geographically into new market areas outside India. The Revlimid patent is expiring in the coming months (i guess its 20 months or so) but they have some ideas that they are working on. Kothur plant has recieved a warning letter but they say the risk can be mitigated through other plants.

Looks like this company is still undervalued compared to peers as of today. Company has guided 20%+ profit growth YoY for FY25

Rajeev Nannapaneni: This year, we did about Rs. 1,388 crores profit. I think going forward next year, we at least see if all goes well and there are not too many surprises, we should do greater than 20% growth for the year.

Why this company is still given low P/E compared to peers? What am i missing? Or are there any other metrics to look at beside P/E?

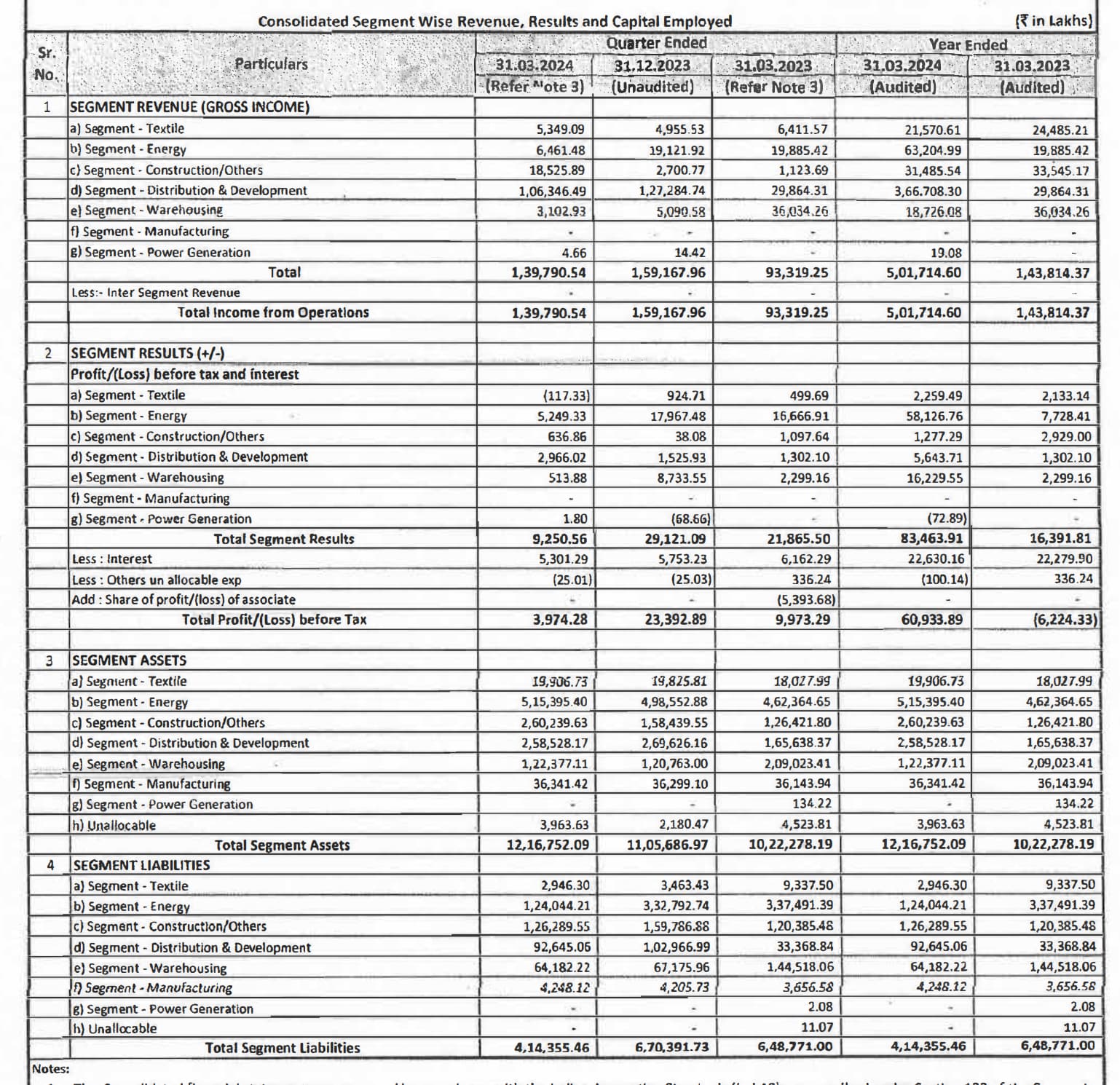

SWAN ENERGY LIMITED (SEL): The company focussing on sectors with strong tailwinds (14-07-2024)

Here is the segment wise break up:

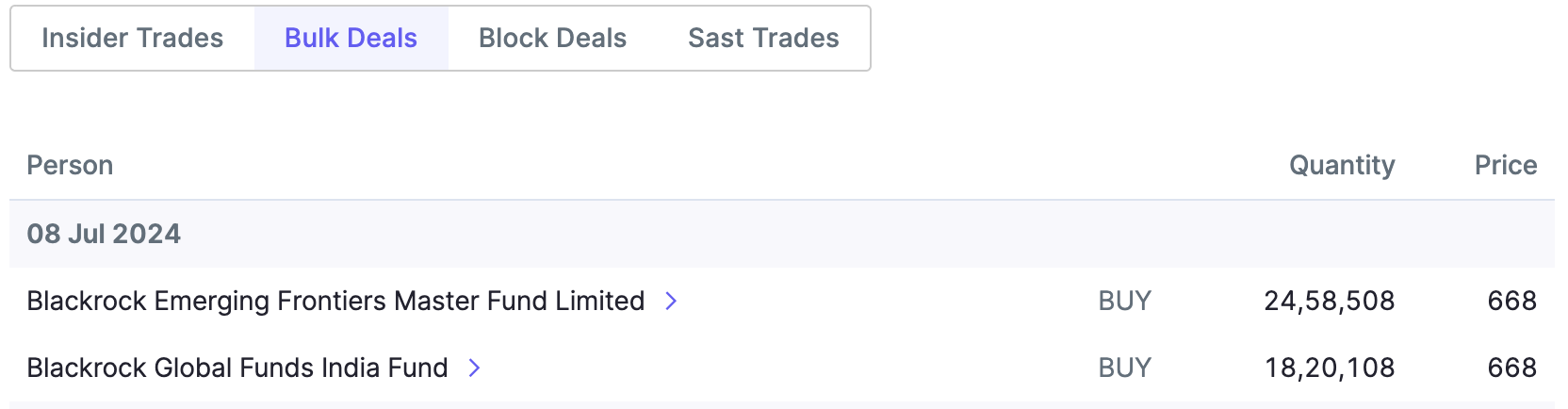

Blackrock has taken a stake worth 285cr aprox, last week:

Everest Kanto Cylinders Ltd. – A long runway ahead! (14-07-2024)

Supplies to Bajaj seem to be very small right now. Once volumes pick up there will be other suppliers also. EKC will most likely lose out on this opportunity also.

In investing the most important criteria is management quality. Bad management will let go of all opportunities as in the case of EKC. And good management can create opportunities where there are few.

For the past few years, the management has been consistently saying the composite cylinders will not be competition – and while EKC had capability to make composite they chose not to. And companies like Time Techno and Supreme are making huge margins in composite cylinders and demand is exceeding capacity. EKC capacity utilisation is 60% !!

Wonder what happened to the new plant in Gujarat… there is no talk of it now.

Even the success of Egypt plant is doubtful. Capacity utilisation of Dubai plants is low – what will do with new plant in Egypt?