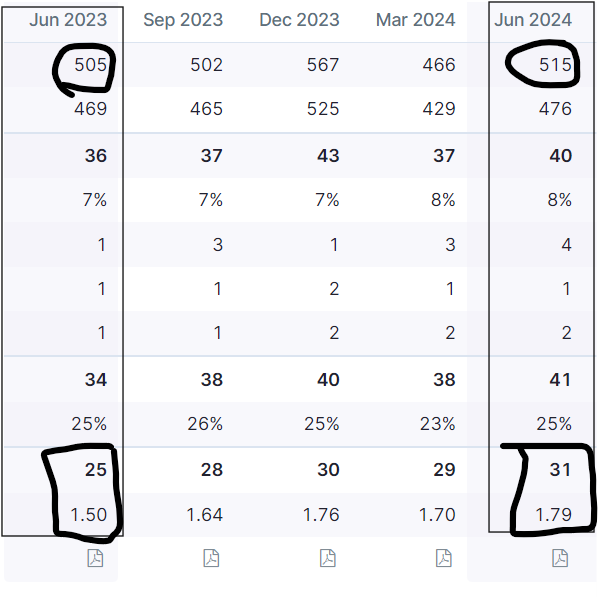

Can someone please help me to know the criteria for calculating ‘Expected Quarterly EPS’ of any company on screener. The description only talks about the Expected sales growth as the criteria. I am unable to understand that how does screener forecasts the future sales and also the EPS. Is it that some AI being used and if so then what is the raw data.

Posts in category Value Pickr

Screener.in: The destination for Intelligent Screening & Reporting in India (12-07-2024)

Can someone please help me to know the criteria for calculating ‘Expected Quarterly EPS’ of any company on screener. The description only talks about the Expected sales growth as the criteria. I am unable to understand that how does screener forecasts the future sales and also the EPS. Is it that some AI being used and if so then what is the raw data.

Walchandnagar Industries | Return of a Golden Era (12-07-2024)

we need to this month closing. There will be intermediate cliffs but it shall keep going higher. Lets also connect quarterly results

Walchandnagar Industries | Return of a Golden Era (12-07-2024)

we need to this month closing. There will be intermediate cliffs but it shall keep going higher. Lets also connect quarterly results

Ranvir’s Portfolio (12-07-2024)

Eris Lifesciences –

Q4 and FY 24 results and concall highlights –

Acquisitions made by the company in last 24 months –

Oaknet Pharma – entry into Derma business – paid Rs 650 cr

Select brands of Glenmark Pharma – paid Rs 340 cr

Derma brands of Dr Reddy’s – paid Rs 275 cr

Biocon’s domestic Nephro and Onco business – paid Rs 366 cr

Swiss Parenterals – sterile Injectables business – paid Rs 640 cr for 51 pc stake

Biocon’s India Injectables business – paid Rs 1242 cr

**Total cost of all acquisitions put together – 3510 cr **

Total revenues of the acquired assets at the time of acquisition – 1240 cr

Q4 outcomes –

Revenues – 547 vs 396 cr, up 38 pc ( domestic revenues @ 480 vs 389 cr )

Gross Profit – 432 vs 402 cr, up 31 pc

EBITDA – 148 vs 118 cr, up 25 pc

PAT – 79 vs 61 cr

FY 24 outcomes –

Revenues – 2009 vs 1685 cr, up 19 pc ( Domestic revenues @ 1902 vs 1606 cr )

Gross Profit – 1629 vs 1332 cr, up 22 pc

EBITDA – 674 vs 536 cr, up 25 pc ( margins @ 34 vs 33 pc )

PAT – 397 vs 374 cr, up 6 pc ( due much higher depreciation, amortisation, finance costs )

There were non-recurring one time expenses of aprox 38 cr in Q4. Adjusted to that, PAT for FY 24 would have been 430 cr

Consolidated Debt on balance sheet @ 3000 cr. Company intends to reduce it to 2600 cr by end of FY 25 out of internal accruals. By the end of FY 26, aim to bring it down to 2000 cr !!!

Aiming for organic revenue growth of 12-14 pc in the domestic formulations business. Aim to maintain EBITDA margins > 35 pc for FY25. Will share complete company level guidance post completion of integration of Swiss Parenterals and Biocon’s domestic business by end of Q1 FY25. Biocon’s domestic business is currently clocking annual sales of 360 cr. Swiss parenterals clocked FY24 revenues of 280 cr with 37 pc EBITDA margins

Eris – Biocon combined will create 5th largest Anti Diabetic franchise in India with Anti Diabetes only revenue base of close to 1000 cr / yr. It will have significant presence across oral and injectable Anti-Diabetic products

Company can work on expanding margins by using Swiss Parenterals manufacturing facilities to manufacture a lot of Biocon’s injectable products

Eris – MJ Biopharm JV ( 70:30 JV formed in 2022 to sell Insulins and GLP-1 products ) is now clocking a monthly sales of 5 cr. It reported an EBITDA loss of 20 cr in FY 23. In Q4 FY 24, EBITDA loss has narrowed down to 1 cr. Should turn EBITDA positive from Q1 FY 25

The Insulin penetration in the domestic mkt is very low. Company sees fairly large growth runway for their Insulin products – both from Biocon’s and MJ Biopharm’s portfolios

Aim to launch 4-5 new brands in India in Q1 in the Critical care space to be manufactured out of Swiss Parenteral’s facilities

Aprox capex lined up for next 2 yrs @ 70 – 80 cr each

Disc: holding, biased, not SEBI registered

Ranvir’s Portfolio (12-07-2024)

Eris Lifesciences –

Q4 and FY 24 results and concall highlights –

Acquisitions made by the company in last 24 months –

Oaknet Pharma – entry into Derma business – paid Rs 650 cr

Select brands of Glenmark Pharma – paid Rs 340 cr

Derma brands of Dr Reddy’s – paid Rs 275 cr

Biocon’s domestic Nephro and Onco business – paid Rs 366 cr

Swiss Parenterals – sterile Injectables business – paid Rs 640 cr for 51 pc stake

Biocon’s India Injectables business – paid Rs 1242 cr

**Total cost of all acquisitions put together – 3510 cr **

Total revenues of the acquired assets at the time of acquisition – 1240 cr

Q4 outcomes –

Revenues – 547 vs 396 cr, up 38 pc ( domestic revenues @ 480 vs 389 cr )

Gross Profit – 432 vs 402 cr, up 31 pc

EBITDA – 148 vs 118 cr, up 25 pc

PAT – 79 vs 61 cr

FY 24 outcomes –

Revenues – 2009 vs 1685 cr, up 19 pc ( Domestic revenues @ 1902 vs 1606 cr )

Gross Profit – 1629 vs 1332 cr, up 22 pc

EBITDA – 674 vs 536 cr, up 25 pc ( margins @ 34 vs 33 pc )

PAT – 397 vs 374 cr, up 6 pc ( due much higher depreciation, amortisation, finance costs )

There were non-recurring one time expenses of aprox 38 cr in Q4. Adjusted to that, PAT for FY 24 would have been 430 cr

Consolidated Debt on balance sheet @ 3000 cr. Company intends to reduce it to 2600 cr by end of FY 25 out of internal accruals. By the end of FY 26, aim to bring it down to 2000 cr !!!

Aiming for organic revenue growth of 12-14 pc in the domestic formulations business. Aim to maintain EBITDA margins > 35 pc for FY25. Will share complete company level guidance post completion of integration of Swiss Parenterals and Biocon’s domestic business by end of Q1 FY25. Biocon’s domestic business is currently clocking annual sales of 360 cr. Swiss parenterals clocked FY24 revenues of 280 cr with 37 pc EBITDA margins

Eris – Biocon combined will create 5th largest Anti Diabetic franchise in India with Anti Diabetes only revenue base of close to 1000 cr / yr. It will have significant presence across oral and injectable Anti-Diabetic products

Company can work on expanding margins by using Swiss Parenterals manufacturing facilities to manufacture a lot of Biocon’s injectable products

Eris – MJ Biopharm JV ( 70:30 JV formed in 2022 to sell Insulins and GLP-1 products ) is now clocking a monthly sales of 5 cr. It reported an EBITDA loss of 20 cr in FY 23. In Q4 FY 24, EBITDA loss has narrowed down to 1 cr. Should turn EBITDA positive from Q1 FY 25

The Insulin penetration in the domestic mkt is very low. Company sees fairly large growth runway for their Insulin products – both from Biocon’s and MJ Biopharm’s portfolios

Aim to launch 4-5 new brands in India in Q1 in the Critical care space to be manufactured out of Swiss Parenteral’s facilities

Aprox capex lined up for next 2 yrs @ 70 – 80 cr each

Disc: holding, biased, not SEBI registered

JTL Industries – Fast Grower at an inflexion point (12-07-2024)

Axis securities limited has released an initiating coverage report in which it has recommended a BUY with a price target of 430 apiece.

The stock shows quite a good technical approach

- The price level of 215 and 221 are its Gann level and is consolidating in that price range for couple of days. historically, it has proven that it gives a good momentum to the stock if it breaks the Gann level.

- The Stock is also moving above 10-day moving average, which indicates some bullishness in the stock.

Fundamentally speaking, in June 2024 Quarter, the stock has performed pretty well, with increase in their Revenues, PAT, and EPS, on QoQ basis.

The company has able to reduce its debtor days drastically by 50% from 74 days to 32 days, in the last 10 years and have also maintained a net cashflow in FY24.

The only concern with the stock is that the Promoters have decreased their holdings in the company by 15% in the last 7 years.

However, FII’s have increased their holdings by 5.82% in the same time frame of 7 years.

Natco Pharma: Focusing On Complex Products (12-07-2024)

Following article elaborate on how generic drugs are very important to US.

-

90% of prescriptions were for generic drugs.

2.FDA is increasing speed of ANDA reviews.

3.US is looking for supply continuity over pricing, that result in increase in price. -

Supply side constrains.

When I ask Copilot about companies I hold, following summary come out. Interesting. -

Natco Pharma:

- Strategic Presence in the US: Natco Pharma has actively engaged in the US market since 2007. By forging co-development and licensing partnerships with leading US generic pharmaceutical companies, Natco has successfully developed and launched several first-to-market generics and complex formulations.

- Recent Transition: Natco Pharma recently completed the transition of DASH Pharmaceuticals into Natco Pharma USA, its US subsidiary. This strategic move strengthens Natco’s commitment to the US pharmaceutical landscape12.

- Recent Launch: Natco Pharma also launched the first generic version of Nexavar (Sorafenib) tablets in the US market3.

- Supriya Lifesciences:

- API & Intermediates: Supriya Lifesciences is engaged in the manufacturing of active pharmaceutical ingredients (APIs) and intermediates. It produces 38 APIs across diverse therapeutic segments.

- Global Reach: The company has a global footprint, with export sales contributing significantly to its revenue. Key customers include Mankind Pharma, Acme Generics, and Akums Drugs and Pharma2.

- Aarti Pharmalabs:

- APIs and Intermediates: Aarti Pharmalabs is a generic pharmaceutical company focused on developing and commercializing APIs and FDFs (finished dosage formulations). It has a strong presence in the Xanthine derivatives segment.

- Global Compliance: The company’s facilities are compliant with worldwide standards (EMA, US FDA, WHO, PMDA, TGA, KFDA, ANVISA).

- R&D Capabilities: Aarti Pharmalabs emphasizes R&D and has filed over 52 patents. It partners with both innovators and generic companies for API development4.

In summary, all three companies have made significant strides in the US generics market, leveraging their expertise, partnerships, and global reach. Keep an eye on their performance as they continue to navigate this dynamic industry! ![]()

D: invested in Natco, supriya and Aarti Pharmalabs.