One follow up question here that I didn’t think of before – was the same model followed in MH? Because I don’t seem to be aware of any large orders to other companies coming from MH?

Posts in category Value Pickr

Arman Financial Services Ltd (07-11-2024)

Sir why you think so? Why not credit access grameen which is market leader in mfi sector. I am betting on market leader which has significant promoter holding with very less retail holding which is exactly opposite in Arman case.

I will love to hear your counter arguments.

Max Healthcare: A Growing Force in India’s Healthcare Sector (07-11-2024)

Max Healthcare’s Q2 and H1 FY25 Earnings Call

Key Pointers

- Stellar Growth: Max Healthcare experienced significant growth in the first half of FY25, largely driven by the successful integration of recent acquisitions, particularly Max Lucknow and Max Nagpur. The company is expanding into new geographies, supplementing its organic growth momentum.

- Strong Financial Performance: The company reported strong revenue growth, healthy profitability, and robust EBITDA per bed.

- Focus on Capacity Expansion: Max Healthcare is aggressively expanding its capacity through both brownfield projects at existing facilities and greenfield projects like Max Smart Super Speciality Hospital. They are aiming to address capacity constraints and cater to the burgeoning demand for healthcare services.

- JP Hospital Acquisition: The recent acquisition of JP Hospital in Noida is a strategic move to strengthen Max Healthcare’s presence in the NCR. Management views it as a marquee asset with significant potential.

- Dwarka Hospital’s Performance: The newly operational Max Dwarka Hospital is demonstrating promising performance and is expected to break even sooner than anticipated.

Key Financials in Tabular Form

| Metric | Q2 FY25 | H1 FY25 | YoY Growth (%) | QoQ Growth (%) |

|---|---|---|---|---|

| Network Gross Revenue (INR Crore) | 2,228 | 4,222 | 22 | 10 |

| Network Operating EBITDA (INR Crore) | 591 | 1,189 | 19 | 17 |

| Operating EBITDA Margin (%) | 28.2 | 27.2 | – | – |

| Annualized EBITDA per Bed (INR Lakh) | 75.5 | 72.8 | 0 | 6 |

| Average Occupancy (%) | 81 | – | – | – |

| Average Revenue Per Occupied Bed (INR) | 76,100 | – | 2 | 0 |

| Profit After Tax (INR Crore) | 383 | – | 13 | – |

Note: These figures exclude extraordinary items, as clarified by the management during the earnings call.

Future Outlook

- Continued Growth Momentum: Max Healthcare is poised for continued growth, driven by its expansion strategy, strong brand recall, and the growing demand for quality healthcare services in India.

- Focus on High-Value Specialties: The company is prioritizing high-value specialties like oncology, cardiology, and orthopedics to further improve ARPOB and overall profitability.

- Integration and Turnaround of Acquisitions: Max Healthcare has a proven track record of successfully integrating and turning around acquired hospitals. This capability is expected to drive future growth and profitability.

- Potential for Margin Expansion: As newly acquired hospitals ramp up their capacity, surgical mix, and payer mix, there is significant potential for margin expansion in the coming quarters.

- Dwarka Hospital’s Break-even: Max Dwarka Hospital is projected to achieve break-even sooner than anticipated, further contributing to the company’s profitability.

Challenges

- International Patient Revenue: Growth in international patient revenue remains subdued due to geopolitical factors and credit risk management. The company is working to diversify its international patient base and expects recovery in the medium to long term.

- Competition: The healthcare sector in India is witnessing increasing competition. Max Healthcare will need to continue innovating and differentiating itself to maintain its market leadership.

- Regulatory Environment: The Indian healthcare sector is subject to evolving regulations. Max Healthcare needs to navigate these changes effectively to ensure compliance and sustain its growth trajectory. This is not stated in the source but is a common challenge for businesses in regulated industries.

Max Healthcare: A Growing Force in India’s Healthcare Sector (07-11-2024)

Business Overview

Max Healthcare Institute Limited (Max Healthcare) is a leading private healthcare provider in India, primarily operating in North India and expanding to other regions. They offer a comprehensive range of healthcare services, from routine check-ups to complex procedures, across a network of 22 facilities, including owned and operated hospitals, partner healthcare facilities, and managed healthcare facilities.

Key services include:

- Advanced Cardiac Care

- Orthopedics

- Oncology

- Renal Sciences

- Neurosciences

- Minimal Access, Metabolic, and Bariatric Surgery

- Obstetrics and Gynecology

- Pediatrics

- Laboratory and Diagnostic Services

- Homecare Services (Max@Home)

- Non-Captive Pathology Services (Max Labs)

Competitive Advantages

- Established Market Position with Strong Brand Equity: Max Healthcare holds a leading position in the North Indian healthcare market, particularly in the Delhi-NCR region, where it derives over 60% of its revenue. The company benefits from strong brand recognition and trust, built over years of delivering quality healthcare services.

- Focus on Premium Market Segment: Max Healthcare primarily operates in metropolitan cities, catering to a premium patient segment. This strategy allows the company to command higher average revenue per occupied bed (ARPOB) compared to industry peers.

- Diversified Specialities and Channel Mix: Max Healthcare offers a wide range of specialities, including oncology, cardiology, neurology, and orthopedics. This diversification reduces reliance on a single speciality and mitigates potential risks. The company also has a diversified channel mix comprising cash, third-party administrators (TPAs), corporates, institutions, referrals, and international business.

- Superior Operational Efficiency: Max Healthcare consistently demonstrates strong operational efficiency, as evidenced by industry-leading metrics such as high ARPOB, occupancy rates, and EBITDA per bed. This efficiency stems from optimized processes, a skilled workforce, and effective cost management.

- Robust Digital Ecosystem: Max Healthcare leverages its brand equity, customer loyalty, and extensive data to build a digital ecosystem. This digital platform enhances patient experience, improves operational efficiency, and drives innovation in healthcare delivery.

- Strong Financial Position and Growth Potential: The company has a healthy balance sheet with strong free cash flows, providing financial flexibility for strategic acquisitions and expansion plans. The company’s consistent financial performance and ambitious growth strategy position it for long-term success.

Financial Performance

Max Healthcare has consistently demonstrated robust financial performance, characterized by strong revenue growth, high profitability, and healthy cash flow generation.

Key Financial Highlights:

- Revenue: In FY24, Max Healthcare recorded gross revenue of ₹5,406 crores, representing a growth of 18.5% over the previous fiscal year. This growth momentum continued in FY25, with Q2 FY25 revenue reaching ₹2,228 crores, a 22% year-on-year increase.

- Profitability: The company’s operating EBITDA in FY24 was ₹1,907 crores, with a significant 16.6% increase. The consolidated operating margin for FY24 was 28.23%, showcasing the company’s strong profitability. In Q2 FY25, the operating EBITDA was ₹566 crores with a margin of 26.6%.

- Cash Flow: Max Healthcare generated strong free cash flow from operations, amounting to ₹258 crores in Q1 FY25. The company’s robust cash flow generation provides financial flexibility for investments and expansions.

- Key Metrics: Max Healthcare exhibits industry-leading metrics, including high ARPOB and occupancy rates. The ARPOB increased to ₹75,800 in FY24 from ₹67,400 in FY23 and further rose to ₹76,100 in Q2 FY25. Occupancy rates remained consistently healthy at around 74.5% in FY24.

Max Healthcare Division-wise Growth

| Business Unit | FY 2023-24 Revenue (INR Crore) | YoY Growth (%) | Key Highlights |

|---|---|---|---|

| Max Network Hospitals | 5,406 | 18.5 | * Stellar growth attributed to higher-end quaternary work, latest medical technology, higher occupancies, and better average revenue per occupied bed days |

| * Revenue growth of 18% YoY and 7% QoQ in Q1 FY25 | |||

| Max Lab | 796 | 28 | * Presence in 41 cities with 1,100+ active partners |

| * Revenue of INR 41 Crore in Q1 FY25, a growth of 21% YoY and 6% QoQ | |||

| * Gross revenue of INR 47 Crore in Q2 FY25, a growth of 21% YoY and 13% QoQ. Max Lab services are now available across 50 cities | |||

| Max@Home | 172 | 24 | * Provides health and wellness services at home |

| * Revenue of INR 49 Crore in Q1 FY25, reflecting a strong growth of 23% YoY and 6% QoQ. Offers 14 service lines over 10 cities and continues to experience a very high rate of repeat transactions | |||

| * Gross revenue was INR 53 Cr in Q2 FY25, a growth of +24% YoY and +8% QoQ, driven by physio & rehab, critical care & pathology sample collection |

Growth Drivers

- Strategic Expansion Plans: Max Healthcare is aggressively pursuing expansion plans, aiming to double its bed capacity in the next 4-5 years. These plans involve a mix of brownfield development, asset-light strategies, and capital-light adjacencies. Recent and ongoing expansions include acquisitions of existing hospitals, development of greenfield projects, and refurbishments and capacity additions to existing facilities.

- Increasing Demand for Quality Healthcare: India’s healthcare sector is experiencing robust growth, driven by factors such as rising disposable incomes, an aging population, increasing awareness of health issues, and improved access to health insurance. This growing demand for quality healthcare services presents a significant opportunity for Max Healthcare to expand its reach and market share.

- Focus on High-Value Specialities: Max Healthcare’s emphasis on high-value specialities, such as oncology, cardiology, and neurology, contributes to its higher ARPOB and profitability. The demand for these specialized services is increasing, further driving the company’s revenue growth.

- Expanding Digital Ecosystem: Max Healthcare’s investments in building a robust digital ecosystem are expected to enhance patient engagement, improve operational efficiency, and enable innovative healthcare delivery models. This digital transformation will likely play a key role in the company’s future growth.

Risk and Challenges

- Regulatory Environment: The healthcare industry in India is subject to regulations and policies that can impact pricing, reimbursement rates, and operational procedures. Changes in the regulatory environment could pose challenges to Max Healthcare’s profitability and growth prospects.

- Intense Competition: The private healthcare sector in India faces intense competition from both established players and new entrants. Maintaining market share and profitability requires continuous efforts to enhance service quality, optimize costs, and differentiate offerings.

- Availability and Retention of Skilled Workforce: The availability and retention of skilled healthcare professionals, including doctors, nurses, and technicians, are critical for Max Healthcare’s operations. The demand for qualified healthcare personnel is high, and competition for talent could lead to increased labor costs and potential challenges in maintaining staffing levels.

- Financial Risks Associated with Acquisitions: Max Healthcare’s growth strategy involves acquisitions of existing healthcare facilities. Integrating acquired entities and achieving operational synergies can pose challenges and financial risks.

- Execution of Expansion Plans: The successful execution of the company’s ambitious expansion plans is crucial for achieving its growth objectives. Delays in project timelines, cost overruns, or challenges in obtaining necessary approvals could impact the company’s financial performance.

Overall Outlook:

Max Healthcare is well-positioned for continued growth and success in the long term. The company’s strengths, including its strong brand equity, focus on premium market segments, diversified service offerings, operational efficiency, and robust financial position, support its positive outlook. However, navigating the challenges of the healthcare industry, such as regulatory changes, competition, and workforce availability, will be crucial for sustained growth.

The company’s aggressive expansion plans, coupled with the increasing demand for quality healthcare services in India, are expected to drive revenue and profitability in the coming years.

Disc: Invested in stock. Views are biased

Shivalik Bimetal Controls Ltd (SBCL) (07-11-2024)

Shivalik Bimetal Controls Limited Earnings Call Summary: Q2 and H1 FY 2025

This summary focuses on the key takeaways from Shivalik Bimetal Controls Limited’s earnings call for Q2 and H1 FY 2025.

Financial Performance:

- H1 FY 2025 Revenue: ₹26.77 crore, a slight decrease of 3.86% from H1 FY 2024.

- H1 FY 2025 Gross Margin: 46.57%, marking a reduction of 272 basis points compared to the previous year. This is due to the shift towards high-demand products with slightly lower margins.

- H1 FY 2025 Profit Before Tax (PBT): ₹47.24 crore, down 11.09% from H1 FY 2024, with a margin contraction of 178 basis points to 21.79%. This was influenced by rising input costs.

- H1 FY 2025 Profit After Tax (PAT): ₹35.2 crore, representing a PAT margin of 16.27%, a modest decline from the previous year.

- Sequential Growth: Q2 FY 2025 revenue grew by 2.8% over Q1 FY 2025, signaling early signs of recovery in the automotive and industrial electronics sectors.

Business Segment Performance:

- Shunt Resistors:

- Growth expected in Q4 FY 2025 and into the next financial year, driven by existing business and new opportunities.

- Growth is expected in India and Asia, with the Indian market showing substantial growth.

- US market is currently in decline but is expected to improve in Q4 FY 2025.

- Bimetal:

- Decline in revenue is attributed to lower global commodity prices for nickel and copper, and reduced demand in certain markets, particularly Europe and Asia.

- Strong growth is expected in the Indian market due to infrastructure growth and a strong real estate market.

Margin Guidance:

- Gross margin is expected to improve to around 50% in the next financial year, assuming a better year for the shunt business.

- Improvement is driven by stabilizing raw material costs and an expected shift in product mix with a higher contribution from the shunt business.

Management Guidance for the Future:

- Focus on delivering quality growth and building on existing R&D efforts.

- Expanding into new component applications, particularly in electric vehicles and industrial applications.

- Continued commitment to innovation, quality, and customer relationships.

Key Risks in the Business:

- Global Inventory Reset: This has impacted demand over the past two quarters, particularly in the US.

- Rising Input Costs: Contributing to margin contraction.

- Dependence on Key Markets: Performance is significantly impacted by demand fluctuations in the US, India, and European markets.

- Competition: The contact business faces more competition compared to shunt resistors.

Industry Outlook:

- Automotive and industrial electronics sectors are showing early signs of recovery, with demand gradually returning.

- The smart meter market is experiencing significant growth, driven by the increasing localization of latching relay production in India.

- Infrastructure growth and a strong real estate market in India are expected to drive demand for bimetal in the switchgear industry.

Disc: Invested

Pricol limited – OEM automotive (07-11-2024)

Pricol Limited Q2 and H1 FY2 Conference Call Summary

- Financial Performance: Pricol Limited reported strong financial results for Q2 and H1 of FY25.

- Revenue from operations reached 6,500 million with an EBITDA of 871 million, resulting in an EBITDA margin of 13.4% for Q2.

- Profit after tax (PAT) was approximately 450 million, with a PAT margin of 6.93% and basic EPS of 3.70 rupees per equity share.

- For the first half of the fiscal year, sales reached 12,530 million, EBITDA was 1,677 million, with an EBITDA margin of 13.39%. PAT for the half year was 96 million, and basic EPS was 7.44 rupees.

- Margin Guidance: Management expects EBITDA margins to remain around 13% to 13.5%. They believe this range is reasonable for their current product mix. Margins are expected to improve by approximately 50 basis points once export volumes recover. Margin softening in Q2 compared to Q1 was attributed to product mix and a wage increase implemented on July 1st.

- Business Segment Performance:

- Automotive: The automotive industry experienced muted sales in Q2, impacting Pricol growth. However, the company still managed to achieve a 15.54% revenue growth compared to the same period last year. Exports have been significantly impacted due to the US election and new policies, leading to much lower demand than initially projected.

- Defense: Pricol currently has no business in the defense segment but is exploring inorganic opportunities in the railway and defense sectors in India. They believe these segments offer higher margins and growth potential.

- New Products: Revenue from new products, such as those in the PE and So segments, is expected in 18 to 24 months. The products are ready and are being tested by customers. The company is on track to achieve its revenue target of 3200 Crores in FY26, through a combination of organic and inorganic growth.

- Battery Management System (BMS): BMS products are still under development and have not yet generated commercial revenue. Management is not overly optimistic about the BMS market due to its fragmented nature and uncertainties surrounding EV adoption.

- Disc Brake (DB): Commercial production of DB has begun, and supplies have commenced to six manufacturers. Significant volume ramp-up is expected in the next fiscal year (FY26).

- Smart Cockpits and Connected Vehicle Solutions: Pricol is witnessing traction and growth in this segment.

- Management Guidance for the Future: Pricol Limited is targeting a revenue of 3200 Crores in FY26. The company plans to achieve this goal through organic growth and strategic acquisitions. They are exploring opportunities in the automotive, railway, and defense segments.

- Key Risks in the Business:

- Muted Demand in the Automotive Industry: The automotive industry is experiencing a slowdown, which is impacting demand for Pricol products.

- Slow EV Adoption: The pace of EV adoption is slower than initially anticipated, potentially affecting demand for EV-related products.

- Export Market Volatility: The US market has been impacted by elections and policy changes, leading to reduced export demand for Pricol.

- Industry Performance: The two-wheeler industry is facing muted demand, with Q3 expected to be particularly weak. The industry is experiencing inventory pileups at dealerships, further indicating sluggish demand.

Capital Expenditure (CAPEX): Pricol is investing 600 crores over three years in various projects, including a new plant in Pune, expansion of the Manesar plant, land acquisition for future plants, line upgrades, a new plastic component molding shop, tool room upgrades, and new PCB lines. Approximately 200 crores will be invested this year, with 150 to 180 crores planned for next year.

Debt and Acquisitions: Pricol currently has no long-term debt and holds comfortable cash reserves. The company is willing to incur up to 300 crores of debt to fund acquisitions, primarily targeting opportunities in the automotive space.

Disc: invested and may be biased

Kotyark Industries – Only Listed pure Biodiesel Player (07-11-2024)

Indian Oil advocates integrating biodiesel processing within existing refineries to meet 5% biodiesel blending target

If OMCs make their own Processing plants of Biodiesel then who will procure Biodiesel from private players like kotyark?

Will it drawdown sales of kotyark?

Kotyark Industries – Only Listed pure Biodiesel Player (07-11-2024)

Govt. Pushing ethanol to blend with diesel instead of biodiesel!

Will it affect Biodiesel industry?

Yatharth Hospital & Trauma Care Services Limited (07-11-2024)

It was a decent quarter as it was expected, good improvement in ARPOB, occupancy in jhansi is ramping up that’s a good sign. Also the unfreezing of nearly half of the amount by IT department also is a good news, also 244cr of cash though around 160cr would be released for Delhi accusation is still decent for the quarters to come, debtors days down to around 122days TTM. Let’s see how will be the Management’s commentary tomorrow but I still dont think we can get close to 1000cr this FY, 500-600cr in 2 quarters that too Q3 being a weak quarter doesn’t look achievable!!

I still don’t understand the fund raising though let’s hope to get a good explanation tomorrow.

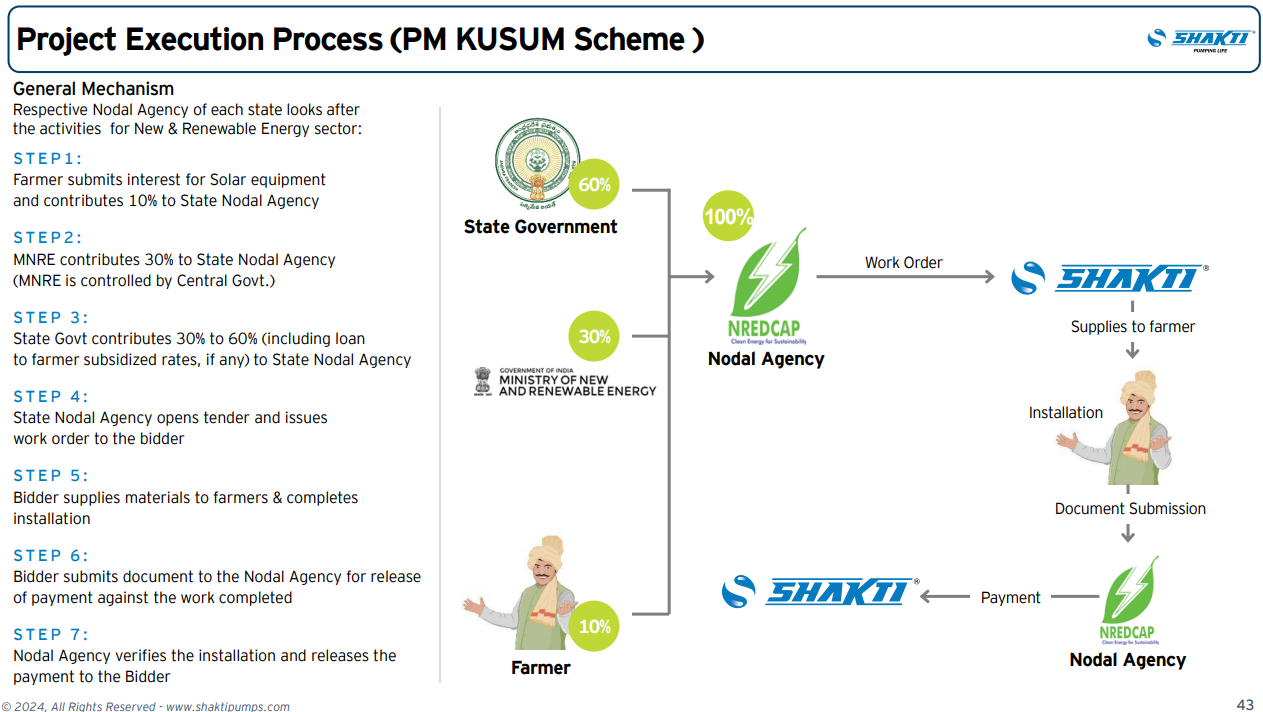

Shakti Pumps – solar shakti (power)! (07-11-2024)

Process flow:

-

Nodal agency (or appropriate state agency) opens the online portal for farmers to place their request.

-

Farmers selects the brand of pump and submits the request online along with their portion payment

-

Nodal agency closes the online portal after they receive enough orders from the farmers. Sometimes max limit is 20k-50k pump and varies according to the requirement of the implemetation.

-

Nodal agency forwards order to the brands selected by the farmer. Rest of the flow you can read from below which is shared by the management

Hope this clarifies.