I am also investing in a similar thing using sheets for different universes. I am asking for CWA2 Sigma how you started after getting indicator access.

You mentioned earlier you have invested something in CWA2 Sigma.

Posts in category Value Pickr

Microcap momentum portfolio (07-11-2024)

Xpro India – getting bigger? (07-11-2024)

Any update on the conference call for this quarter. Couldn’t find the dates for it anywhere?

Vaibhav Global ~ Vertically integrated value e-tailer of Jewellery and Lifestyle Products (07-11-2024)

Can someone explain me how is US consumer different from Indian consumer, like I never see TV channels like Naaptol … Also what is the cost of having channel in US ?

Their website might have some organic traffic but do we know the ration of website vs tv-channel traffic. Like what traffic will remain on Website if no users sees TV channel?

Hi Tech Pipe-Recent Expansion and Operating Leverage to Drive Earnings (07-11-2024)

Hi-Tech Pipes Limited reported mixed results for Q2FY25:

• Sales Performance:

- Revenue declined 5% year-over-year (YoY) and 19% quarter-over-quarter (QoQ) to Rs 7 billion

- Sales volume reached a record high of 123,000 tonnes, up 23% YoY and 1% QoQ

- Blended realizations fell 23% YoY and 19% QoQ to Rs 57,378/tonne, primarily due to lower HRC prices

• Profitability:

-

EBITDA increasing 58% YoY

-

EBITDA per tonne was Rs 3,429, up 29% YoY

-

Adjusted profit after tax (PAT) grew 72% YoY

-

Strong volume growth offset by lower realizations

-

Operational efficiency gains helped maintain EBITDA margins despite falling HRC prices

-

Company demonstrated resilience in managing inventory losses – Can fellow VP members shed light on how Hi-Tech pipes managed lower inventory losses than APL APollo?

KPI Green- Turning Sunshine Into Cashflows (07-11-2024)

https://www.screener.in/company/KPIGREEN/consolidated/#quarters

Even in sequential terms, top-line and net profits have seen slight growth and are at record high levels.

Passing orders on to related entities is the company’s stated stated policy, is it not? It is how costs are controlled and timeline/ execution is ensured at better than industry standards. As long as KPI Green’s eventual results/ margins are not significantly impacted, it does not seem like a problem for shareholders.

Please note that I am a novice investor and looking to learn.

CCL Products (07-11-2024)

Cocoa Prices Reached All-Time Highs. What Does This Mean For Our Chocolate? | Big Business

No positions. Just tracking

IDFC First Bank Limited (07-11-2024)

This is regular banking event. If one needs to stay in touch with banking good to hear.

Not specific to IDFC First Bank though Vaidyanathan is one of the speaker participant.

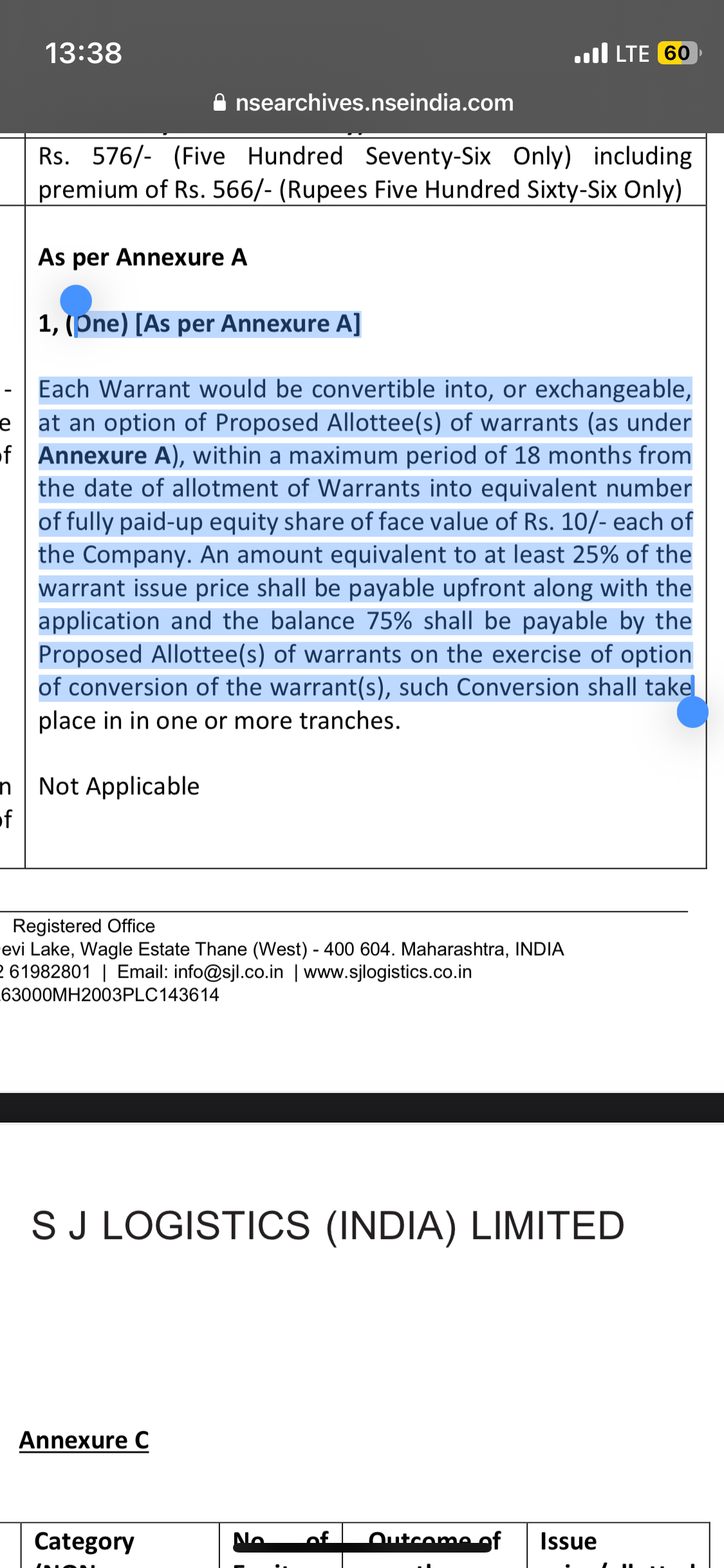

SJ Logisitics- Dark Horse (07-11-2024)

Great work…

Any idea why we are not seeing the 80cr allocation in sept balance sheet?

What do you think of market size and growth rates for project segment?