This looks quite interesting @Mudit.Kushalvardhan is there any resource on how to use this for beginners?

Posts in category Value Pickr

Indiabulls Housing – A compounder from here? (03-07-2024)

Atlast long awaited change of name!!!

Indiabulls Housing Finance Limited 4.pdf (936.8 KB)

Indiabulls Housing – A compounder from here? (03-07-2024)

Atlast long awaited change of name!!!

Indiabulls Housing Finance Limited 4.pdf (936.8 KB)

Gujarat Themis Biosyn Ltd – Bulk Drugs growth momentum (03-07-2024)

Analysis is good but how come exit PE of 17 is considered the norm ? Almost no pharma company trades at that PE even during this downturn of pharma/ api companies and it did not during the last upturn phase in 2020 – 2021.

Gujarat Themis Biosyn Ltd – Bulk Drugs growth momentum (03-07-2024)

Analysis is good but how come exit PE of 17 is considered the norm ? Almost no pharma company trades at that PE even during this downturn of pharma/ api companies and it did not during the last upturn phase in 2020 – 2021.

Black Box: Building infrastructure for the AI revolution (03-07-2024)

- Basic businesses do make money but there has to be some moat protecting their castle – branding, regulations, deep technical expertise (low barrier), upfront capex, long contracts, etc. The fact that their primary moat is global presence, execution record and probably low price means that their margins will always be capped + I am not sure what premium you would pay for the first 2 things

SaaS players in US, you will notice that the reasons company is throwing around for delay in execution and in decision making is actually true and echoed by many.

But the companies main clients for data centers are hyperscalers, large social media companies, etc. both of which aren’t slowing down. So, this is probably a contract thing

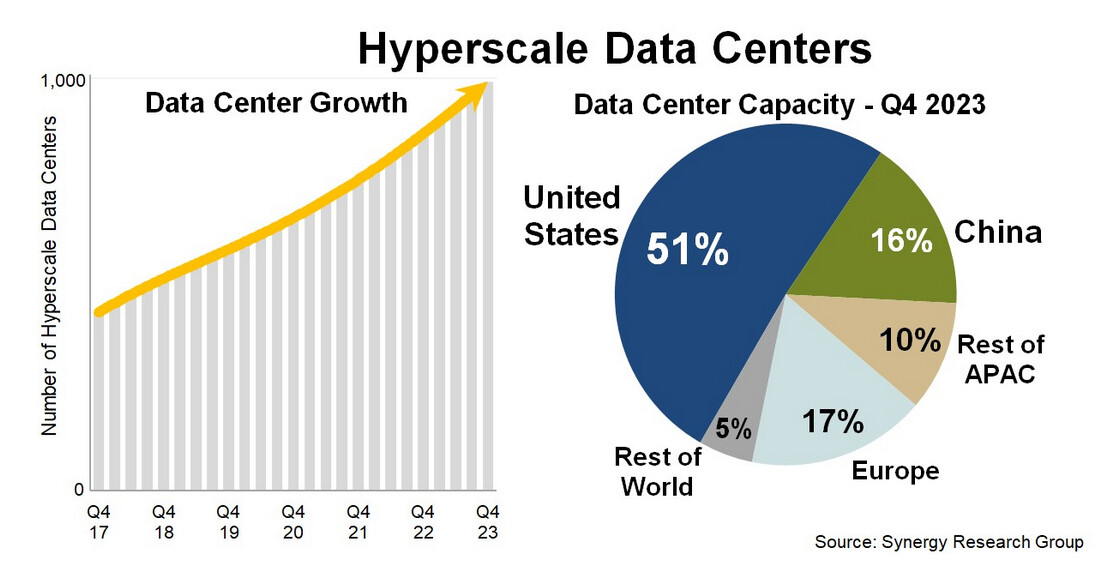

No. of hyperscale data centers are doubling every 4 years, meaning ~18% CAGR growth which is not present here.

Black Box: Building infrastructure for the AI revolution (03-07-2024)

- Basic businesses do make money but there has to be some moat protecting their castle – branding, regulations, deep technical expertise (low barrier), upfront capex, long contracts, etc. The fact that their primary moat is global presence, execution record and probably low price means that their margins will always be capped + I am not sure what premium you would pay for the first 2 things

SaaS players in US, you will notice that the reasons company is throwing around for delay in execution and in decision making is actually true and echoed by many.

But the companies main clients for data centers are hyperscalers, large social media companies, etc. both of which aren’t slowing down. So, this is probably a contract thing

No. of hyperscale data centers are doubling every 4 years, meaning ~18% CAGR growth which is not present here.

Sirca Paints India Limited (03-07-2024)

Apoorv clearly mentioned 25-30% growth in wood segment so that alone will be about 370 cr + wall paint and decorative paint about 60 cr + welcome brand 50 to 100 cr so its quiet likely they can hit 500 cr in fy25 with 20-22% ebitda they can easily do 70 cr profit in fy25.

With regards to cagr growth post fy25 there were 2 different statements…to 1 participant he mentioned 25-30% growth and in final closing question he mentioned 40% cagr for next 3 yrs…

looking at the current outlook on paint industry after birlas entry even 30% growth is quiet satisfactory.

Disc

Invested and will be adding on further declines