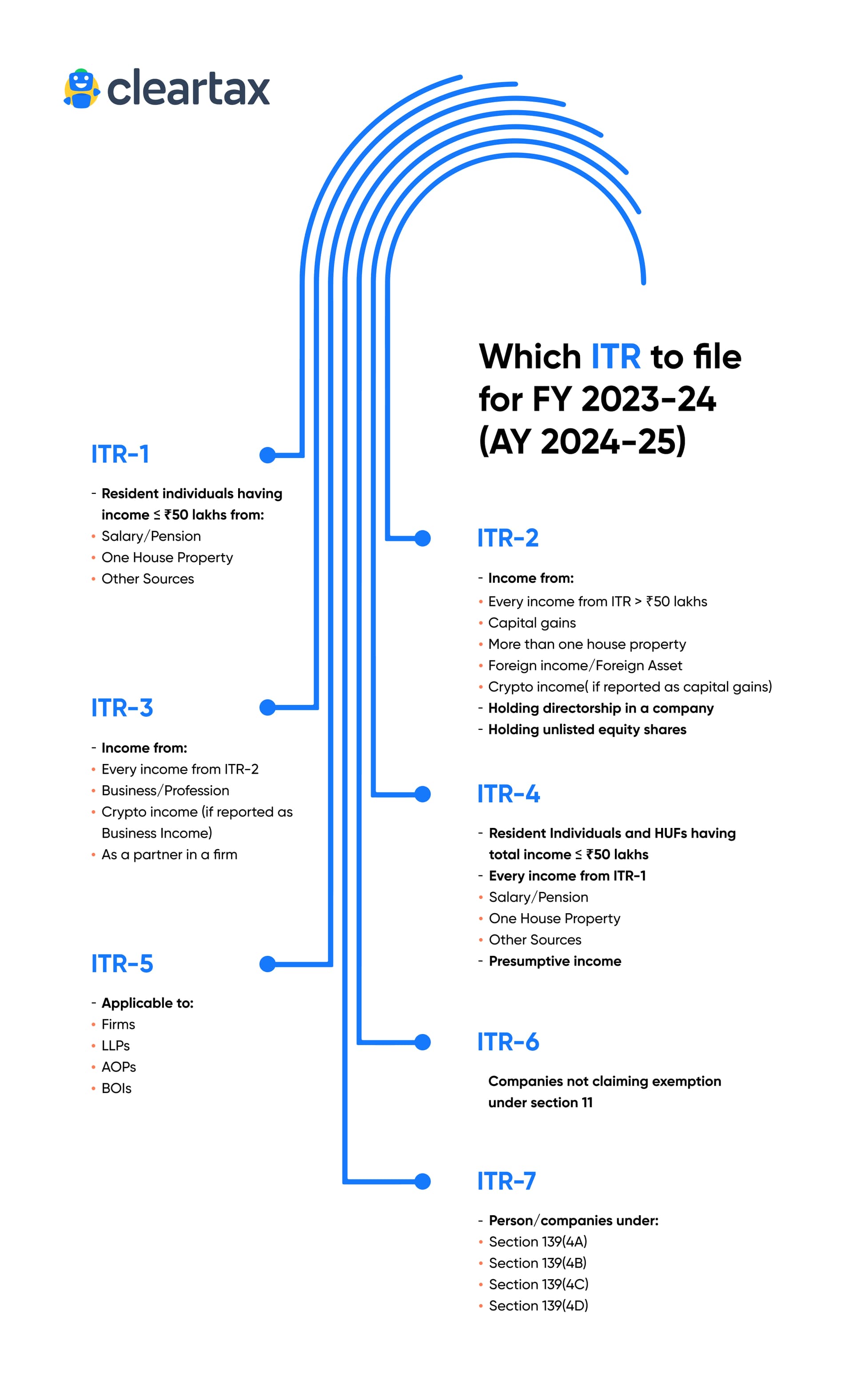

Tax filing season is on and this infographic beautifully captures all the different ITRs.

Source

Tax filing season is on and this infographic beautifully captures all the different ITRs.

Source

Thankyou for the pointers. I went through the details. I could not find why the promoters did not subscribe fully to the rights issue, but the pointers were really helpful to understand the business better. May be not a good business, but to develop and understanding, below are my assessments.

I no more hold this company but I am curious about understanding a business, their balance sheet, cash flow etc and this is now just one company that I am trying to understand as a part of my learning.

Krishca Strapping- a breakout after a long time, with strong volumes confirming the shift in the trend.

The new unit which is to sell higher margins straps is commercialized. They have doubled the capacity with this unit, taking the revenue potential to 300cr at peak utilisation. This yr they plan to do 40-50% utilisation, and will fully utilise it over 4yrs (although i expect it to be a lot earlier)

The peak revenue of 300cr, is excluding the packaging segment which can do a lot more then strapping segment once they get more approvals

They have also introduced another segment of products, primary packaging, which again is expected to be higher margin.

Have opened up their khaata with SAIL with 2 orders. Its very difficult to get into PSUs, SAIL has given them their smallest plant for now, SAIL has a lot many more plants, huge opportunity opens now.

Only 3 companies compete here, the new fourth one is krishca.

Mid East plan is still on, to setup a unit there, this can be very huge, as they will be the only one with a unit here and will be able to source rm from cheap asian countries, hence can compete even with china

Export sales is growing very rapidly, to do 30cr+ this yr and 100cr in the next 5yrs, i feel it can be done sooner.

Focusing on several new countries and already getting repeat orders, although smaller orders

The biggest risk here was a small TAM, but now they are getting into other prods (ofc a natural diversification and nothing else), these are higher margin then straps.

Also recently the company has given an intimation of a potential fund raise, which i assume will be used for this new expansion and the Mid East expansion.

there is detailed thread on this company, if needed

invested and biased

Securities and Exchange Board of India (SEBI) has debarred background check company SecUR Credentials and its managing director (MD) Rahul Belwalkar from the securities market, for imposing significant restrictions due to alleged financial irregularities and corporate governance lapses.

This action follows a series of communications between the company and the exchange, with the latter expressing concerns over the non-provision of crucial details by the company.

In the order, Ashwani Bhatia, whole time member (WTM ), says “The company and its MD have also adopted a cavalier approach while seeking to ensure compliance with fair and accurate disclosure requirements as is evident from the non–disclosure of the outstanding balance in respect of the unsecured loan availed from its MD, accurate disclosure of the status of its Rights Issue”

SEBI issued an Interim Order against Varanium Cloud Ltd and its MD, Harshawardhan Hanmant Sabale, for misusing public funds and manipulating financial statements. They were found to have made fictitious purchases from SecUR Credentials Ltd, where Mr Sabale’s shareholding increased from 1.22% to 17.83% between December 2023 and March 2024.

Further the market regulator noted that the order highlights several critical issues. SecUR Credentials had announced fund-raising efforts through Rights Issues totaling Rs6,190 lakh in December 2022 and September 2023, but subsequently did not proceed with these issues nor disclosed updates, which appears to contravene Regulation 30(7) of the LODR Regulations. Additionally, the company entered into an agreement with Varanium to outsource operations for conducting due diligence on Bank of Maharashtra’s loan applicants. However, discrepancies were found in the operational details provided, suggesting potential violations of Regulations 4(1)(c), 4(1)(e) read with 30(12) of the LODR Regulations.

SEBI’s investigation uncovered that there was no clear segregation between the bank accounts of SecUR and Mr Belwalkar, with funds being transferred between the company and various entities linked to the promoter and directors without adequate substantiation. This raises suspicions of fund diversion. Further scrutiny of transactions between SecUR and Varanium revealed that revenue recognition from these transactions resulted in an inflated net profit of approximately 30% in the company’s financial statements. Furthermore, Mr Belwalkar was found to have transferred significant funds to the MD of Varanium Mr Sabale.

The order also noted material related party transactions (RPTs) with Mr Belwalkar that exceeded shareholder-approved limits and were inadequately disclosed in the company’s financial statements. The company failed to reclassify its promoter and promoter group entities despite repeated requests, and Mr Belwalkar acted as the compliance officer without formal appointment, contravening the LODR Regulations.

SEBI findings indicated a troubling concentration of power in Mr Belwalkar’s hands, which led to a disregard for regulatory compliance and corporate governance practices. The company’s funds were used by Mr Belwalkar without proper checks, reflecting poorly on the management’s commitment to shareholder interests and market integrity. This situation is particularly concerning given SecUR’s migration from the SME platform to the mainboard in October 2022, attracting investments from a larger number of retail investors. As of 31March 2024, SecUR had 9,626 public shareholders, whose interests are now at risk.

SEBI has restrained SecUR and Mr Belwalkar from buying, selling, or dealing in the securities market until further orders. They are allowed to close out any open positions in exchange-traded derivative contracts within seven days. Additionally, Belwalkar is barred from acting as a Director or Key Managerial Personnel of any listed company or SEBI-registered intermediary until further notice.

Ref: SecUR Credentials, Managing Director Faces SEBI Action over Financial Misconduct

Concall notes for this quarter, they are expecting faster growth going forward with improvement in margins.

FY24Q4 Lincoln concall

Expect to grow sales by 15-18% CAGR and reach 1000 cr. in 3-4 years at 20-22% EBITDA margins

Export

Present in 60 countries. Strong presence in East Africa followed by West Africa, Latam, Southeast Asia

Transitioned from B2B to branded generics in 2021, and focus is now on generating prescriptions through doctor-MR

Have 30-35 MRs

1500+ registration; 750 pipeline

Focus is to grow exports to Canada, Australia and Europe

Commercialized 4 products in Canada (19 filed)

Domestic

Present in 13-15 states; top 3 are Uttar Pradesh, Assam, Odisha

Were earlier present in Tier 3 cities and now are increasing presence in Tier 2 and Tier 1 cities

600 MRs which should increase by 150-200 in next 2 years as they expand to more states

Strong in ENT segment (Tinnex brand)

Entire sales are through prescriptions (branded generic)

20% portfolio under NLEM

Launched 20-23 products in FY24

Cephalosporin

Plant was commercialized, injectable block has been implemented. Have WHO approvals and filed products

Expect 55-65 cr. in FY25

At full utilization, can reach 220-230 cr. revenues depending on final product prices

Also servicing Indian market from this unit

Capex

Invested 100 cr.+ via internal approvals in last 3-years

25-30 cr. annual capex plans for next 2-years

Currently they have 17-18 lines, with 25 lines they can do 1200-1300 cr.

Solar capacity is now 4 MW (solar plant + rooftop solar). Will be saving on energy costs because of this

Related party loans

Loans and advances increased from 82 cr. to 104 cr.

Explained this as a way to do capex; current year increase was for the next big product (like they did cephalosporin couple of years back) and for getting into more regulated (and higher margins) markets such as US

Have not suffered from currency issues because of their B2B model where distributors arrange payments

Dermatology, cardiology, diabetes are the main growth focus, contribute 100-150 cr. (domestic + exports). Expect to grow 50% in FY25

Munjal Patel is looking after finance, exports and factory

Disclosure: Invested (position size here, bought shares in last-30 days)

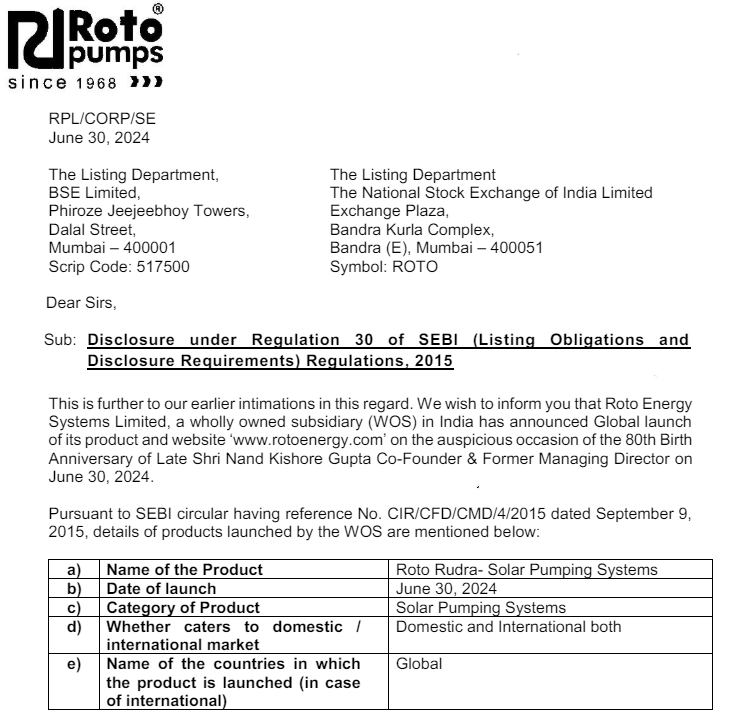

Global Launch of Roto Rudra -Solar Pumping Systems

Disc: Invested

Hariom Pipe Management Interview

Some Important things:

-Past growth will sustain

-Will focus on improving operating efficiency & VAP

-ROCE will inch upward to 21%

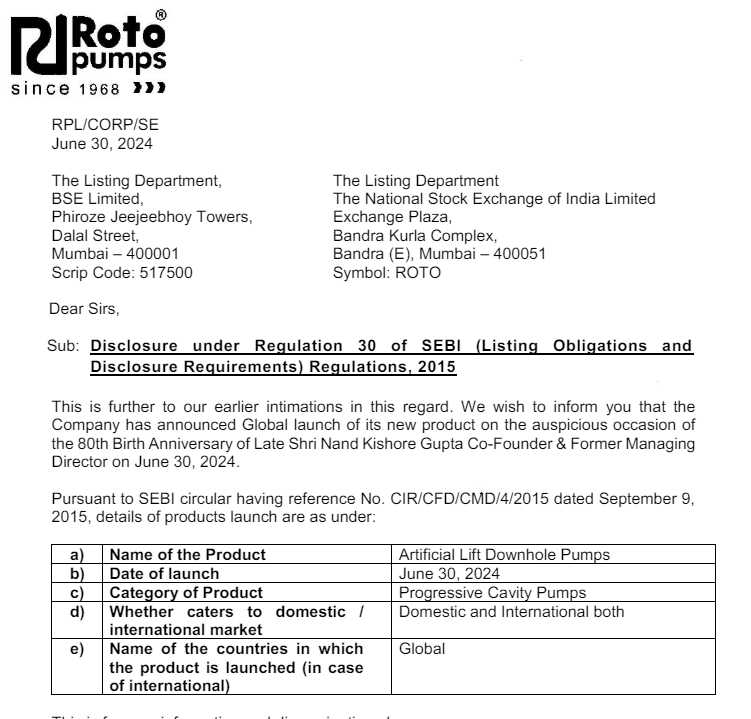

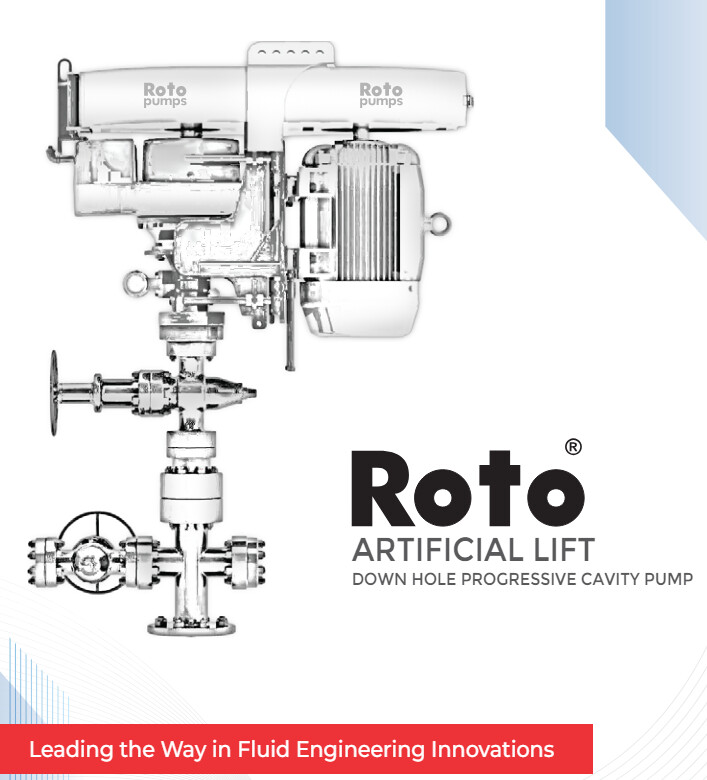

Global launch of new product Artificial Lift Downhole Pumps under Progressive Cavity Pumps

Dist: Invested

Delhivery and TCI Express have very different business models which reflects in their margin profile and balance sheet. TCI is very selective in their customer segments while Delhivery seems to have taken a kitchensink approach (growth at any cost).

I’m yet to see a new entrant disrupting a market purely on the basis of simply pricing in any industry. They may eat into some business of established players but eventually need for cash flow generation, sustainable margins and scalable business growth all catch up. So if the new entrants don’t have a differentiated offering, they simply fizzle out or are forced to scale back on price war.

Take diagnostics space. For two years people thought new players with cheap diagnostics service providers, backed with huge P/E money, will disrupt existing players like Lalpath. But now that’s all behind us.

TCI Express has maintained their pricing power and kept their balance sheet healthy with strong return metrics (industry leading ROE and ROCE) in the face of intense competition.

So when the new entrants eventually succumb to the pressure of showing profits and cashflows, we’ll see strong differentiated incumbents emerging much stronger.

The real waste to wealth could start from here

recent investor presentation