@hitesh2710 sir what are your technical views on ujjivan small finance bank. Last 2-3 days there are heavy sellers with large volumes and stock is sliding.

Posts in category Value Pickr

Shriram Pistons & Rings Ltd (25-06-2024)

I used chatgpt to extract key details from the earnings call. Sharing here for everyone’s benefit.

Link: https://chatgpt.com/share/2cbecd37-2271-4199-a738-9b62c08637f7

Note: I had a hard time understanding this line – Investment in areas agnostic to the powertrain to ensure long-term growth and stability

Here is what it means:

Agnostic to the powertrain: “Agnostic” in this context means not specifically tied or dependent on any particular type of powertrain. A powertrain refers to the mechanism that drives a vehicle, including the engine, transmission, and drivetrain. Examples include internal combustion engines (ICE), electric powertrains, and hybrid systems. Being “agnostic” means the investments are not dependent on or specifically designed for any one type of powertrain.

Disclaimer: Not invested yet. Will be adding in near term.

Amoul Portfolio (25-06-2024)

There are a few pre-screens that I have, here are a few things I look for

- EPS should be More than 20

- Top-line growth should be more than 25% for the last 3 years

- Promotor should have skin in the game (good percentage of holding and this should be the only holding they have)

- PE ratio: High PE is okay as long as PE < 2-time profit growth

- The company should have a market cap between 300Cr to 30000 Cr

- There are other indicators like asset turnover, OPM, and PB ratio which vary from industry to industry

Once I have a basic prescreen then do a business model evaluation. I typically like stocks from the consumer, banking and IT sectors which are more secular.

LT Foods has grown at around 30% for the last 3 years which is good considering the nature of the business. Even if they grow at 25% stock should do well considering it is trading at a low PE. If there is PE expansion it will be icing on the cake.

Sealmatic India Limited (25-06-2024)

@rk1771

Thanks for the creating thread on SEALMATIC.

sharing few more things from my side:

BUSINESS MODEL:—-

1, OEM ( Non Project Related)

2, OEM ( Project Related)

3, O&M ( Starts after commissioning of Project)

OEM ( Non Project Related):—-Set of OEMs, which are not project related, which we call them as non-API business, which is profitable. So for example, we have business, let’s say example, KSB, Kirloskar and many more pump companies. So our business and our journey in mechanical Seals started in 2012. So predominantly, for the first eight years or nine years from 2012 until 2020, or rather ’21, was purely exporting mechanical seals globally to more than 47 countries, and which was – and which is still continuing. It’s a profitable business.

OEM ( PROJECT RELATED):—– when we do projects and OEM business, a huge amount of resources in terms of money, time and manpower are required. And secondly, it also requires a lot of accreditation, certification, approvals, and all those things.so,we stayed away from the Indian market for the first eight years or nine years.

The only time that we lose money is on this large project, which are refineries, oil and gas, petrochemicals, power plants, etcetera. But once our seal fitted into an oil and gas refinery or any other core sector application typically gets replaced between 12 months to 18 months after commissioning of project. So because you want to enter into that business and then once that seal goes into the end user you have an annuity of 30 years. So your seal will give your business for the next 30 years and which will recover your cost more than 30 times over the cost of investment that you made. So once the project gets commissioned, which typically take 2.5 years to commission that pump because there are many other peripheral activities happening simultaneously at the project site.

we also do very scientific approach to taking orders and balancing them off. We don’t want to blow too much of cash away by taking too much of projects. So, we balance it out with end users, retailers, project and OEMs.As per Management, anything which is happening here in India, where we supply to OEMs, it is a project business. And that’s a business which drains our resources and drains our cash flows. So, that business would be approximately 20% of the turnover.

O&M ( Starts after commissioning of Project):—

All projects which are being commissioned at various stages from FY22-23 will be converted into O&M business would start from April 2026. So, that would contribute significant revenue on the top line and also increase the bottom line.

As per Management the gross margins of O&M would be in the range of 85% to 90% and that would be a Golden period for Sealmatic.

A project typically, let’s discuss a project of Rs.15 cr which is for Mongol Refinery. So we will execute this project by last quarter of this financial year. So by March or April 2025 we would be completing the execution of this project. It will get assembled at the pump OEM site and it will be transported to the refinery in Mongol. Say 3 years down the line when the plant gets commissioned, any product which has come as anOEM remains as an OEM. So with Mongol I will have say example 200 pumps which are fitted with the Sealmatic mechanical Seals and that itself is going to generate a revenue of rs. 16 crs every year for us.

EARNING GUIDANCE:—-

we will double our turnover in 3 years’ time and from the FY2027 and half of the revenue will come from O&M business, that is our golden period, we will kick in where we will be able to encash on all the investments that we made in projects.Revenue potential from cuurent capacity will be INR 200 crs, if we do only O&M business.

RECESSION PROOF BUSINESS MODEL:–

As per management, Our product is recession proof. If you look at the 2 years of COVID that went by and if you look at our financial performance, we have increased our turnover and profit. So, these products are critical, they are required. And no matter what, if there’s a recession but they need to run a refinery or they need to run a power plant or they need to run a petrochemical plant and these products are required. So, I have never seen in my 35 years of experience any cycling, disturbance affecting our business. So, at the moment our major hunting ground would be refinery which would include oil and gas. Then I would say power, both nuclear and thermal, and petrochemical and chemical. So, I would say that surmises a majority of the market requirement and one of the most profitable business for any mechanical seal company globally. So, I would still like to focus in this area is because it is critical, actually it is highly profitable and certainly, it has got a long lifecycle. So, equipment in such an industry are having a life cycle of 30 years.

OPPORTUINITY IN GREEN HYDROGEN PROJECT:—–

Anything which is conveying media in any kind of form, maybe a liquid or a gas or any other medium, a mechanical seal comes into play, maybe a solar power plant, maybe a hydrogen cell unit. Or maybe hydropower. So, a seal is always deployed.

CMPETITION:—

Mechanical seals are critical installations and once it is installed in a project it is impossible to replace it during the lifetime of that project. It is important for you to just enter. Once you enter, then it’s 100% for you. There will be no competition for that particular project.

DISCLOSURE:– INVESTED.

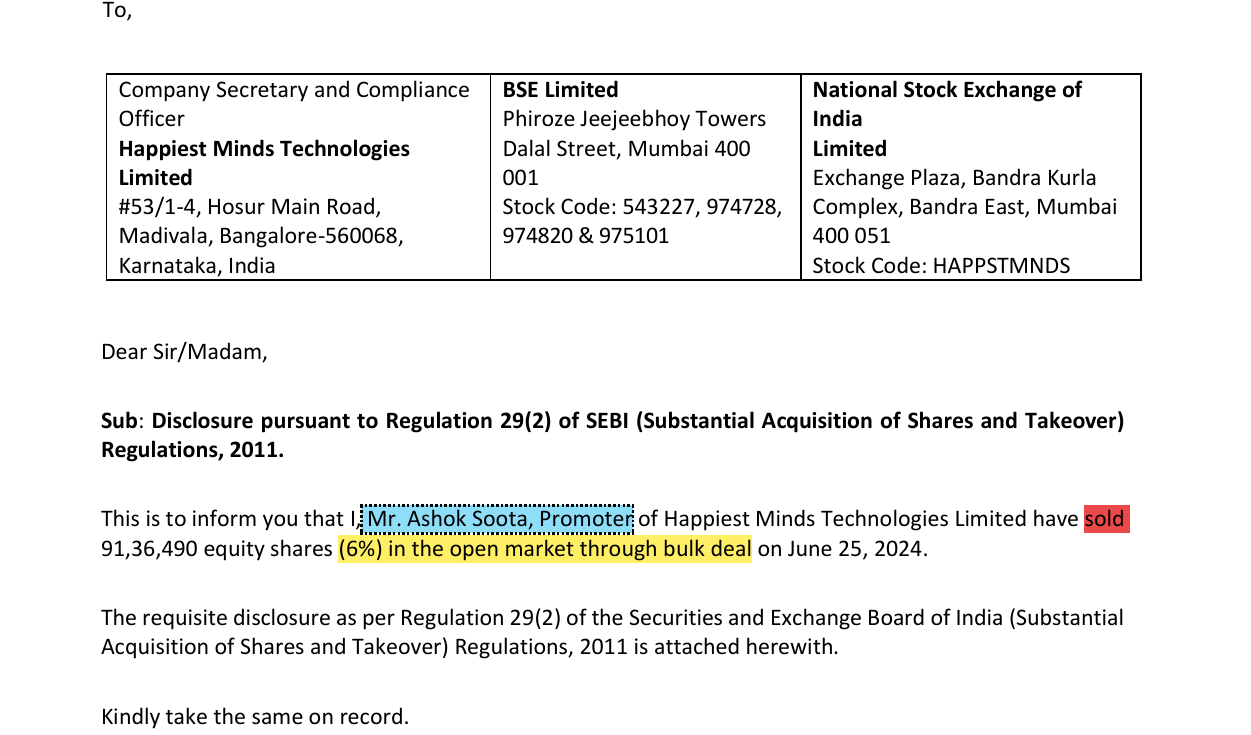

Happiest Minds Technology (25-06-2024)

Promoters Sold 6% stack

SG Finserve Ltd – Does it has a scalable business? (25-06-2024)

q3fy 24

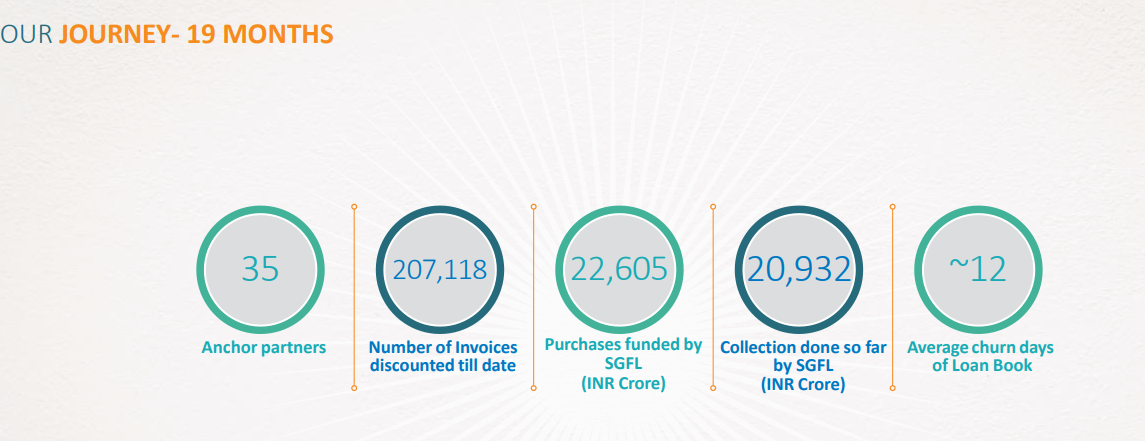

q4fy24

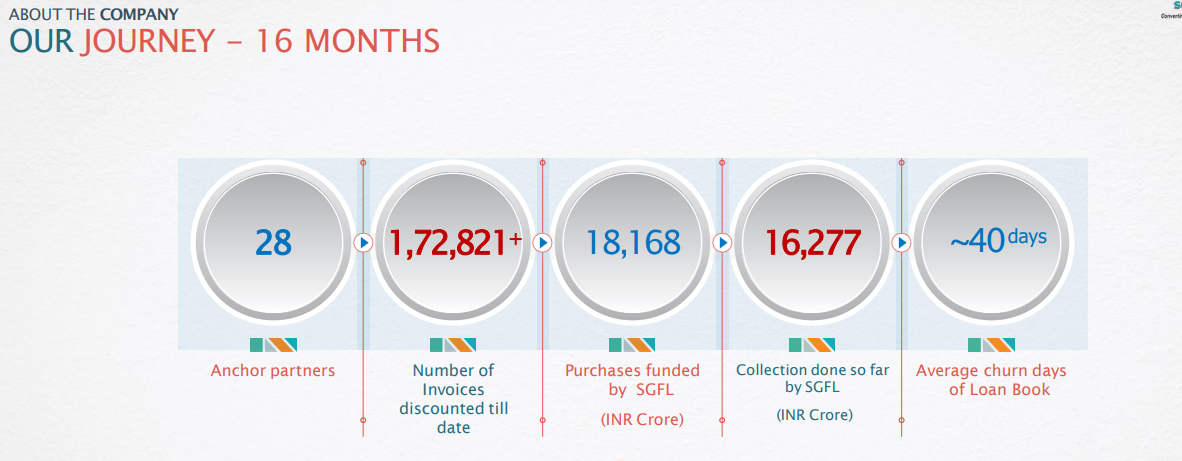

in q4fy24 result presentation 19 months journey average churn days of loan book have come down to 12 days from 40 days in q3fy24 result presentation 16 months journey

Sealmatic India Limited (25-06-2024)

Few observations:

- The recent half yearly results looks not so great.

- Apart from consistent negative cash flows, other ratios are also on higher side (Inventory days, payable days, working capital days).

- YOY the operating margins have come down.

SG Finserve Ltd – Does it has a scalable business? (25-06-2024)

gross disbursement q4fy2024= 4437 cr >>gross disbursement q3fy2024=4139 cr,

reduction in AUM reflects that the new loans issued were of shorter duration ,