Problem is not capex. Problem is working capital. How do you solve for that?

Posts in category Value Pickr

Companies with 20%+ growth guidance for next few years (17-06-2024)

The management has been very conservative in disbursing loans(which should actually be a good sign but that has led to slow growth) but now they want to go a bit aggressive. Plus the revenues, financing profits, and net profits have risen consistently but the share price has not inculcated the growth in last 5 years. NPAs are controlled and declining on both QoQ and YoY basis. I tried but couldn’t find any major red flags in the company.

So, the main reason is the valuations (one of the lowest price-to-book multiples in the industry currently). I really think that when banks and financials start to give a run-up, city union bank will benefit from 2 way- reversion to the mean industry valuations, and sector bullishness.

Maharashtra seamless-a value plus cyclical play (17-06-2024)

The numbers are fine and dandy so is the opportunity. I suppose the anti-dumping duty ends by 2026 and unless extended it can impact margins. Another anti-thesis pointer could be competition, as peers are also expanding capacities, but this can be partially offset by the large opportunity set

Disc: 1% of my PF

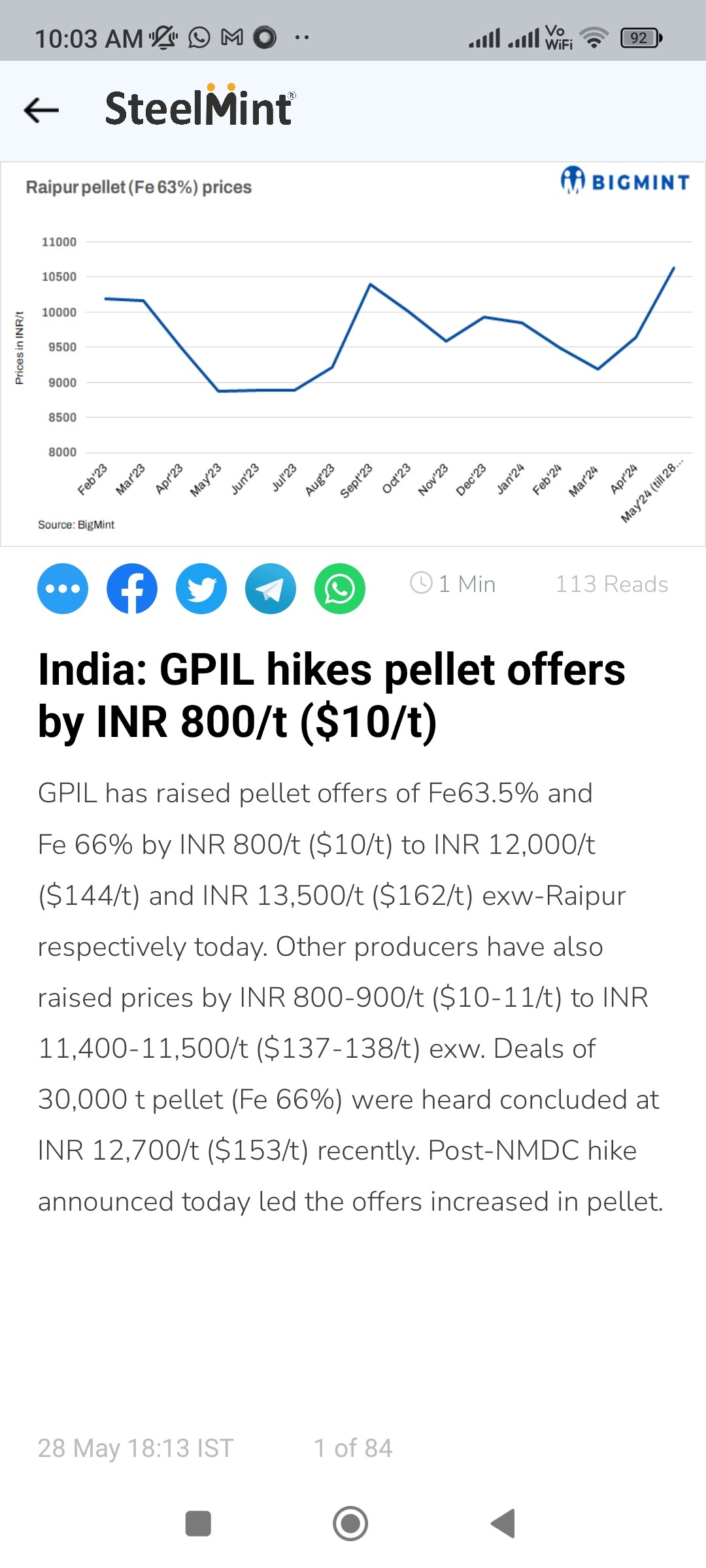

Godawari Power – Any Trackers? (17-06-2024)

GPIL hikes pellet prices by 800 Rs per ton and they are selling everything domestic only as per concall. Moreover as elections are over, now they can get steel plant approval anytime. I believe this is not the time to sell but I could be wrong.

HBL POWER SYSTEMS: Booting-up for the Race of the Century (17-06-2024)

Kaynes Technology in their investor call has projected significant revenue from Kavach. Not sure whether they are onboarded as an primary vendor like Hbl, kernex etc or they are supplying to one of the multinationals.

HBL POWER SYSTEMS: Booting-up for the Race of the Century (17-06-2024)

“New OEMs are expected to be onboarded for the upcoming tenders as the railways plan to expedite the implementation of Kavach.”

“Other benefits of ‘Kavach’ include the controlling speed of trains by automatic application of brakes on the approach of turnouts, repeating of signal aspects in the cab, which is useful for higher speeds and foggy weather, and auto whistling at level crossing gates.”

Disc: invested

Companies with 20%+ growth guidance for next few years (17-06-2024)

I am a bit curious to understand why you have picked City Union Bank? What are it growth drivers?

Companies with 20%+ growth guidance for next few years (17-06-2024)

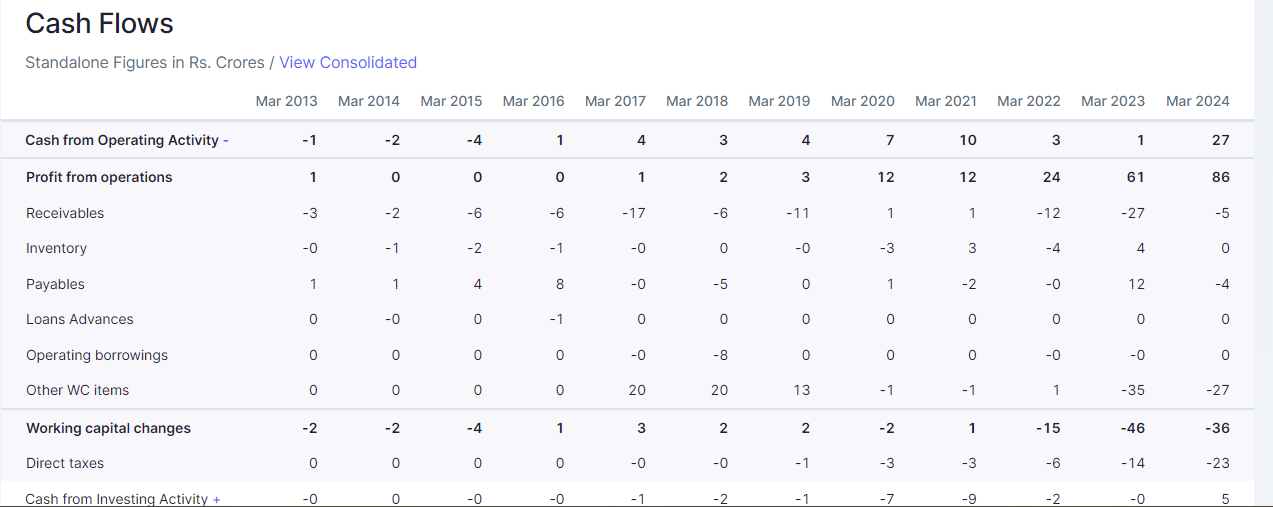

I had kept Jyoti resins in my portfolio for a long time. However, I dumped the stocks after realizing that the cashflows are subdued and not in line with the income this company is reporting.

Cashflow from Operations is a mere 25% whereas the benchmark is ~80%

Transpek Industry limited (17-06-2024)

Transpek did FY24 revenue of 605cr with EBITDA of 108 cr at 18%. Degrowth in FY24 was led by volume decline and low price to some extent. Management expects modest revival in H2FY25 and guided for near to double digit growth for FY25. Notes from Q4 call:

Fy 24 was challenging to the industry due to global destocking, slow demand from end customers and pricing pressure, China impact and red sea crisis in the late half.

Overall market structure/end uses are not changing but customers are taking a cautious approach in placing orders. Polymer industry (which contributes major revenue) customers and are expanding capacities and Transpek products are used in high end aramid fibers where China is not active.

During the last 3-4 years we have developed 5 to 6 new acid chloride products. These products can reach 100 Cr over 2-3 yrs.

Non acid chlorides(3-4 products) : going through validation by end customers followed by performance testing. So these products will take 3-5 yrs. These are high margin products and the target is to reach 30-35% of revenue from this segment. Once we achieve 30% of revenue these products’ margins will be 20-23%. Potential for these products together is 200cr.

Our products go into critical applications like medicines, critical applications polymers like defense/fire fighting. Validation of these products from customers and regulators takes time.

Started supplying new acid chlorides to korea which has good potential.

New product pipeline in R&D is quite robust.

Capex for 3-4 new products will be based on demand from customers. Company is looking to acquire small facilities or job work rather than greenfield expansion.

Current capacity can do peak revenue of 900cr. FY24 utilization at 68% and expecting to reach 78% for FY25.

Discl: tracking

Corporate Fraud/Misdemeanor – Public Domain – Global lessons (17-06-2024)

Keep the crore with u, that I’m sure you don’t have.

Point is promoter has sold na.

His holding has come down na.

I wouldn’t feel comfortable in a share where promoter is offloading or reducing his share and clubbed with price action like this.

U feel comfortable with such scripts .

Good luck to u !