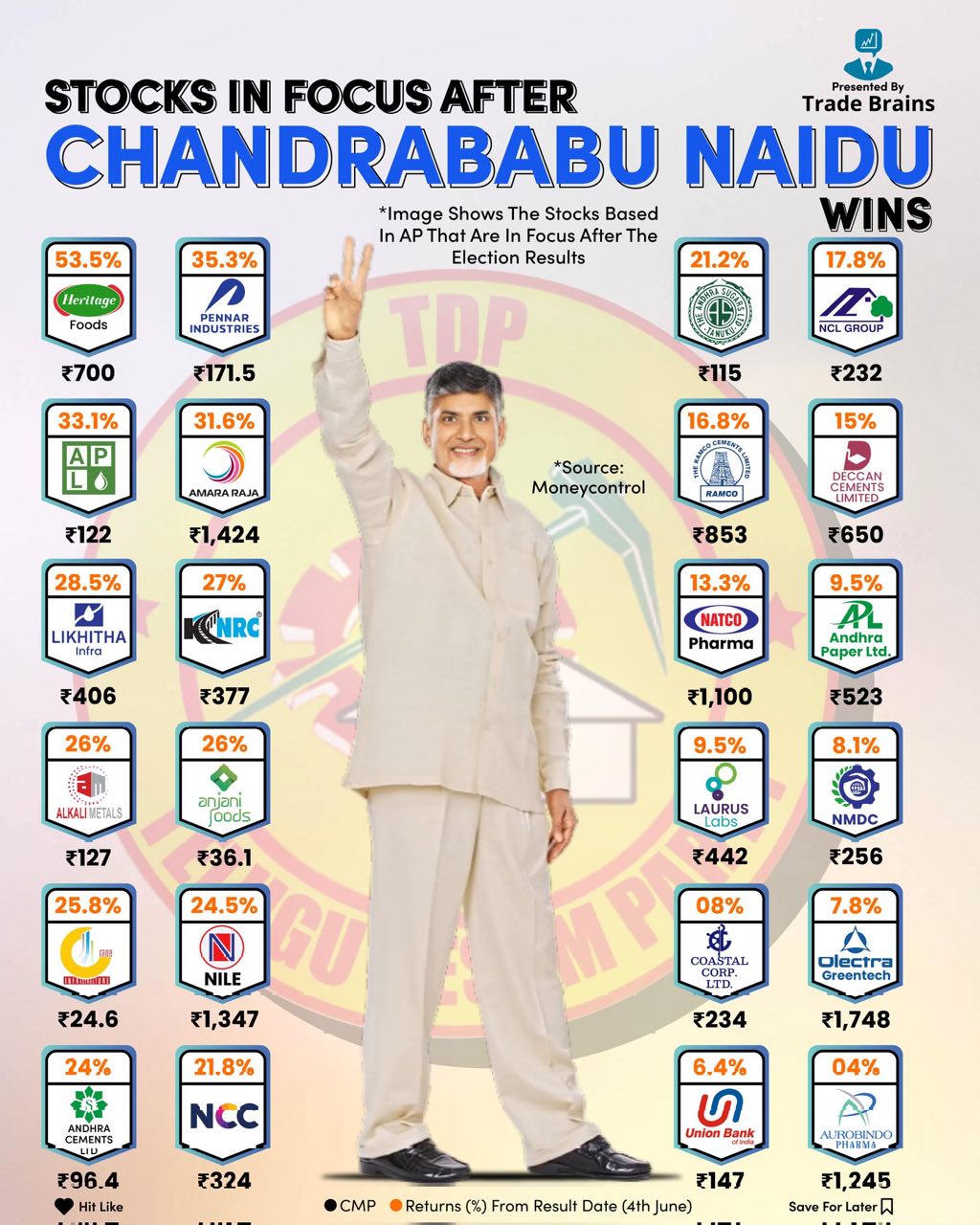

SINGLE PICTURE AND SHARE IS 20% UP UNBELIEVABLE.

SINGLE PICTURE AND SHARE IS 20% UP UNBELIEVABLE.

Dear All,

In below thread we will start analyse about NBFC companies with basic items. If we can continue this topic long enough, based on historical data we will try to understand how business prospects are changing based on basic items.

As I use AI tools for Analysis, there may be some mistakes too.

Kindly use Basic Analysis of NBFC companies data only for educational purposes. Don’t make investments decisions based on this. For investments more than basic data need. Kindly aware of that

I’m also learner of NBFC company. So Requesting your inputs to improve this thread. So our learning will keep Improve.

Dear All,

In below thread we will start analyse about NBFC companies with basic items. If we can continue this topic long enough, based on historical data we will try to understand how business prospects are changing based on basic items.

As I use AI tools for Analysis, there may be some mistakes too.

Kindly use Basic Analysis of NBFC companies data only for educational purposes. Don’t make investments decisions based on this. For investments more than basic data need. Kindly aware of that

I’m also learner of NBFC company. So Requesting your inputs to improve this thread. So our learning will keep Improve.

The biggest investment they have made is in NSE 425crs. They have got 13,25,000 shares at the Rs. 3,207 a share. I think unlisted share price of nse is more than rs 5000 a share, which means the company has already made unrealized gain of 50%+ on this investment. If the management can deliver returns in excess of 15-20% on the cash they hold on balance sheet, I think investors still benefit because ultimately book value keeps on expanding. Yes, I agree to an extent doing investments at peak margins and peak valuation is quite risky, especially in current scenario where PSUs are overowned. So, a negative.

The biggest investment they have made is in NSE 425crs. They have got 13,25,000 shares at the Rs. 3,207 a share. I think unlisted share price of nse is more than rs 5000 a share, which means the company has already made unrealized gain of 50%+ on this investment. If the management can deliver returns in excess of 15-20% on the cash they hold on balance sheet, I think investors still benefit because ultimately book value keeps on expanding. Yes, I agree to an extent doing investments at peak margins and peak valuation is quite risky, especially in current scenario where PSUs are overowned. So, a negative.

Electrolyzer as a product is not feasible. To replace grey hydrogen, green hydrogen needs to be sold at or around 2$/kg. No one is close to this price, except a company called Hysata. Secondly, with the advent of white hydrogen, electrolyzer might actually get disrupted in near future. However, remain very bullish on fuel cells. Disc: Biased and Invested

The client bases are different. Incremental orders for Bloom is going to come from data centers. Now, i get your point regarding high interest rates, but data centers industry in US is booming and growing, with the advent of Nvidia and others. Don’t see why won’t Bloom and ultimately MTAR benefit from this

Thanks for the reply. Yes that I know higher credit cost is in fact compensated by higher yield, but was unsure of the part of credit cycle we are in. Thanks for sharing your view.

I think management has explained this point in the concall- MFIN is becoming a high credit cost industry, but at the same time, ROAs and ROEs compensate them for the risk they are taking.

My sense is, in the past we have seen cycles like 2011-2016 with no credit events or 2003-08. If Macro remains strong, good credit cycle for lenders can continue. There is no high stress or systemic risk at the moment anywhere. Wholesale lenders are still seeing write backs

Pratap Snacks –

Some highlights from Q4 and FY 24 results –

FY 24 outcomes –

Revenues – 1618 vs 1653 cr

EBITDA – 141 vs 63 cr ( margins @ 9 vs 4 pc – massive margin expansion !!! )

PAT – 53 vs 20 cr

Q4 outcomes –

Revenues – 388 vs 387 cr

EBITDA – 35 vs 19 cr ( margins – 9 vs 5 pc – massive margin expansion )

PAT – 12 vs 22 cr ( had some tax reversals in Q4 FY 23 )

Rural demand continues to be tepid vs the Urban demand

Margin expansion mainly led by – restructuring of distribution channel and margins, cost optimisations and process improvements

Focussing on sales force automation to further reduce costs and to improve decision making using data analytics

Increased share of Namkeens in the company’s portfolio is also margin accretive

New Jammu and Rajkot plants have been operationalised recently. Jammu facility has a revenue potential of 160 cr at full capacity

Hopeful of a rural revival which should aid company’s growth and margins. Seeing some green shoots in Q1. If they sustain, company aims to do a double digit revenue growth for FY 25

In FY 24, company’s Namkeens portfolio contributed 16 pc of sales and grew by 15 pc YoY. All other categories de-grew marginally

( Extruded snacks, Potato chips, Sweet snacks )

Company has recently been listed in D-Mart, Reliance retail. This should help aid margins as more of high volume packs are sold through modern retail channels

Company’s core target consumers are middle class and below – both in rural and urban markets (unlike for players like ITC, Pepsi etc who mainly target middle class and above )

Confident of maintaining EBITDA margins > 8 pc for FY 25 ( there may be Quarterly variations ). The ultimate aim is to go to double digit margins on a sustainable basis

Aim to realise 50 – 100 cr sales from export ( basically Middle East ) markets inside next 2 yrs

Out of 20 lakh outlets at which company’s products are available, namkeen is available at only 5 lakh outlets. Clearly, there is a lot of scope for growth in this segment

Company’s overall capacity utilisation is @ 55 odd pc. Not likely to incur any major Capex expenses over next 2 yrs

Potential of yearly sales from Reliance Retail + D Mart for the company is around Rs 50 cr / yr

Marketing and sales promotion spends for FY 24 @ 1.5 pc of sales

Disc: hold a tracking position, may add if rural recovery sustains, biased, not SEBI registered