And that interest rate is paid by merchant right.

Posts in category Value Pickr

Focus Lighting & Fixtures Limited (SME) (10-06-2024)

*Focus Lighting – **

Q4 and FY 24 concall highlights –

Q4 outcomes –

Sales – 60 vs 41 cr

EBITDA – 14 vs 8 cr ( margins @ 23 vs 20 pc – very healthy margins for a manufacturing company )

PAT – 11 vs 6 cr

FY 24 outcomes –

Sales – 224 vs 168 cr

EBITDA – 46 vs 33 cr ( margins @ 21 vs 20 pc )

PAT – 39 vs 23 cr

Breakdown of Q4 revenues –

Retail Lighting ( high end / specialised lighting solutions for brick and mortar retail outlets ) – 31 vs 32 cr

Home lighting ( company is into high end home lighting unlike most other players like – Havells, CG Consumer, Surya etc ) – 26 vs 8 cr

Infra Lighting ( basically – projects / orders based business ) – 2 vs 10 cr

Railways – 0.1 vs 0.4 cr

Company’s retail lighting is primarily sold under PLUS – brand name

Company’s MD gave out a presentation on the kind of cutting edge / unique lighting solutions that the company has developed / is developing. Its a must watch for anyone trying to understand the moats that the company is building

Company’s retail clients include – Mercedes, Volvo, Porsche, Citroen, BMW, Tata Retail, Reliance Retail, Ikea, Lenskart etc

Some marquee projects where company has done the lighting work include – Central Vista – Parliament, Surat Fort, Guwahati Airport, ITC – Shanghai, Mumbai Airport etc

Reliance is the biggest retailer in India. Company expects Reliance retail to be back to aggressive expansion mode wef Q3 this year. That’s when they see a lot of domestic retail business to come to them

Retail segment in ME markets is doing well

Overall, guiding for > 15 pc growth in retail segment for FY 25

Expect to see high growth coming from Home and Infra segments for FY 25

All verticals combined, company is guiding for 30 pc kind of topline growth with margins at current levels

Avg ticket size per retail store ( except very large format stores like IKEA ) @ Rs 20 lakh to Rs 1 cr. For Infra, its Rs 5 to Rs 40 cr depending on project to project. For Homes, its between Rs 5 lakh – Rs 3 cr per house

Company is going to enter the trade segment in 6-8 months. Initially, the company will get into contract manufacturing for the bigger brands. But the company will only make the differentiated products. In medium term, company also intends to develop its own brand

Disc : holding, biased, not SEBI registered

SBI Cards & Payment Services Limited (10-06-2024)

I am not aware of the specifics. But I know one instance. Bought a macbook air on no cost emi of 9 months. The interest rate is being shown as 15%.

The typical interest rate on normal credit card dues are 25-40%. So if I would have to guess, I would say IR on no cost emi is much lower.

Ranvir’s Portfolio (10-06-2024)

**Focus Lighting – **

Q4 and FY 24 concall highlights –

Q4 outcomes –

Sales – 60 vs 41 cr

EBITDA – 14 vs 8 cr ( margins @ 23 vs 20 pc – very healthy margins for a manufacturing company )

PAT – 11 vs 6 cr

FY 24 outcomes –

Sales – 224 vs 168 cr

EBITDA – 46 vs 33 cr ( margins @ 21 vs 20 pc )

PAT – 39 vs 23 cr

Breakdown of Q4 revenues –

Retail Lighting ( high end / specialised lighting solutions for brick and mortar retail outlets ) – 31 vs 32 cr

Home lighting ( company is into high end home lighting unlike most other players like – Havells, CG Consumer, Surya etc ) – 26 vs 8 cr

Infra Lighting ( basically – projects / orders based business ) – 2 vs 10 cr

Railways – 0.1 vs 0.4 cr

Company’s retail lighting is primarily sold under PLUS – brand name

Company’s MD gave out a presentation on the kind of cutting edge / unique lighting solutions that the company has developed / is developing. Its a must watch for anyone trying to understand the moats that the company is building

Company’s retail clients include – Mercedes, Volvo, Porsche, Citroen, BMW, Tata Retail, Reliance Retail, Ikea, Lenskart etc

Some marquee projects where company has done the lighting work include – Central Vista – Parliament, Surat Fort, Guwahati Airport, ITC – Shanghai, Mumbai Airport etc

Reliance is the biggest retailer in India. Company expects Reliance retail to be back to aggressive expansion mode wef Q3 this year. That’s when they see a lot of domestic retail business to come to them

Retail segment in ME markets is doing well

Overall, guiding for > 15 pc growth in retail segment for FY 25

Expect to see high growth coming from Home and Infra segments for FY 25

All verticals combined, company is guiding for 30 pc kind of topline growth with margins at current levels

Avg ticket size per retail store ( except very large format stores like IKEA ) @ Rs 20 lakh to Rs 1 cr. For Infra, its Rs 5 to Rs 40 cr depending on project to project. For Homes, its between Rs 5 lakh – Rs 3 cr per house

Company is going to enter the trade segment in 6-8 months. Initially, the company will get into contract manufacturing for the bigger brands. But the company will only make the differentiated products. In medium term, company also intends to develop its own brand

Disc : holding, biased, not SEBI registered

Phantom Digital Effects Limited (10-06-2024)

I see a lot of comments of receivables being shot up, it’s 51cr for 2024. Could someone point out what thresholds should we consider as high for it? Is it revenue to receivables or are you tracking some other ratio?

SBI Cards & Payment Services Limited (10-06-2024)

What is the interest rate on that emi and this interest rate policy is same for other buy now pay later options are this cost is only charged my credit card companies

DCX Systems Ltd (10-06-2024)

I like the management statement. They are more focused on the business rather than making investors happy

Manappuram Finance (10-06-2024)

What is holding manappuram in recent rally post election results? I think holding corporation issue creates obstacles after Asirvad listing. I don’t know why prompter want to go for holding corporation route for Asirvad listing. Is it makes better control over newly formed company? Any experience person can share his/ her views on this.

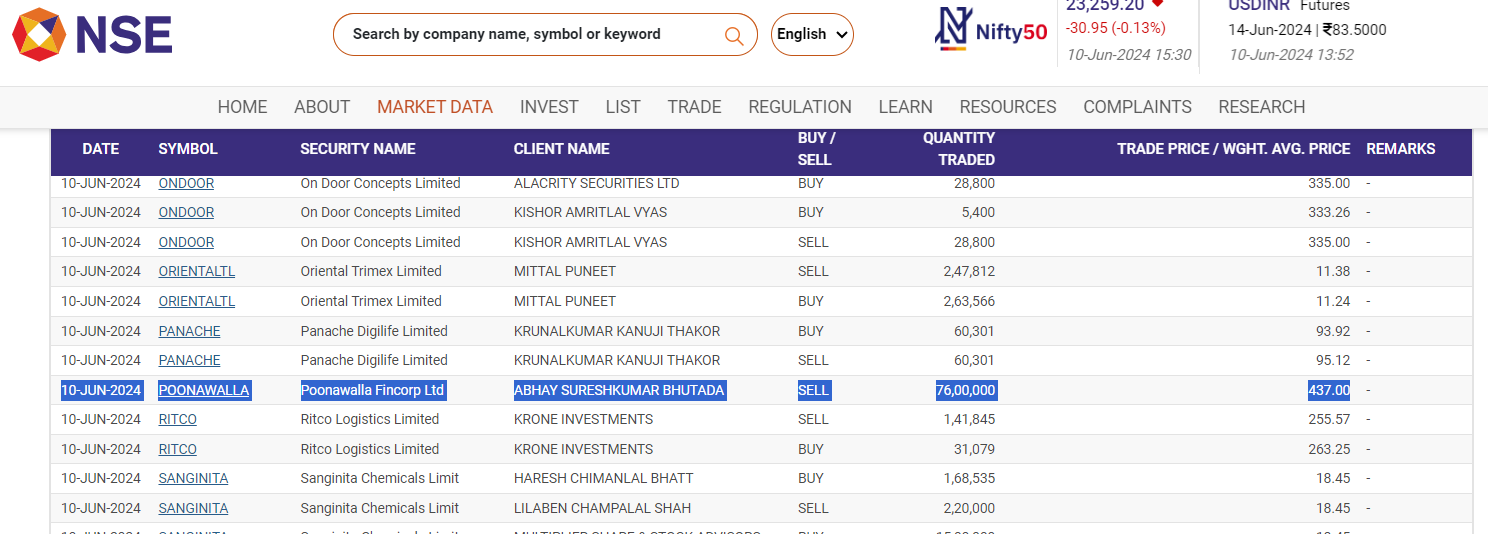

Poonawalla Fincorp formerly Magma Fincorp (10-06-2024)

332 Crs worth of shares sold by the MD

Indian Energy Exchange (IEX) (10-06-2024)

Interesting article ,though might require a Pro subscription from Moneycontrol to access.

The gist of the article :

-

India established a national electricity grid more than a decade back by integrating five regional grids in phases.It may appear that a uniform power tariff should be a logical culmination

-

MBED was the outcome of the deliberation between stakeholders to explore the feasibility and the implementation of a uniform tariff across the country.

-

Unfortunately, MBED hasn’t made much headway so far. One key reason is that it is primarily meant for electricity buy-sale through power exchanges. At present, power exchanges account only for about 7 percent of India’s total electricity generation, while close to 90 percent of power is contracted through long-term power purchase agreements (PPAs).

-

Electricity, being on the Concurrent list, is caught between cross currents. As both the Centre and the states have jurisdiction over the power sector, New Delhi cannot make tariffs uniform or even change them unilaterally. Significant amendments will have to be made to the Centre and state laws to take it forward.

-

States with lower power generation costs may resist Kumar’s demand for “one nation, one power tariff” as an average uniform levy may translate into higher prices for their consumers.