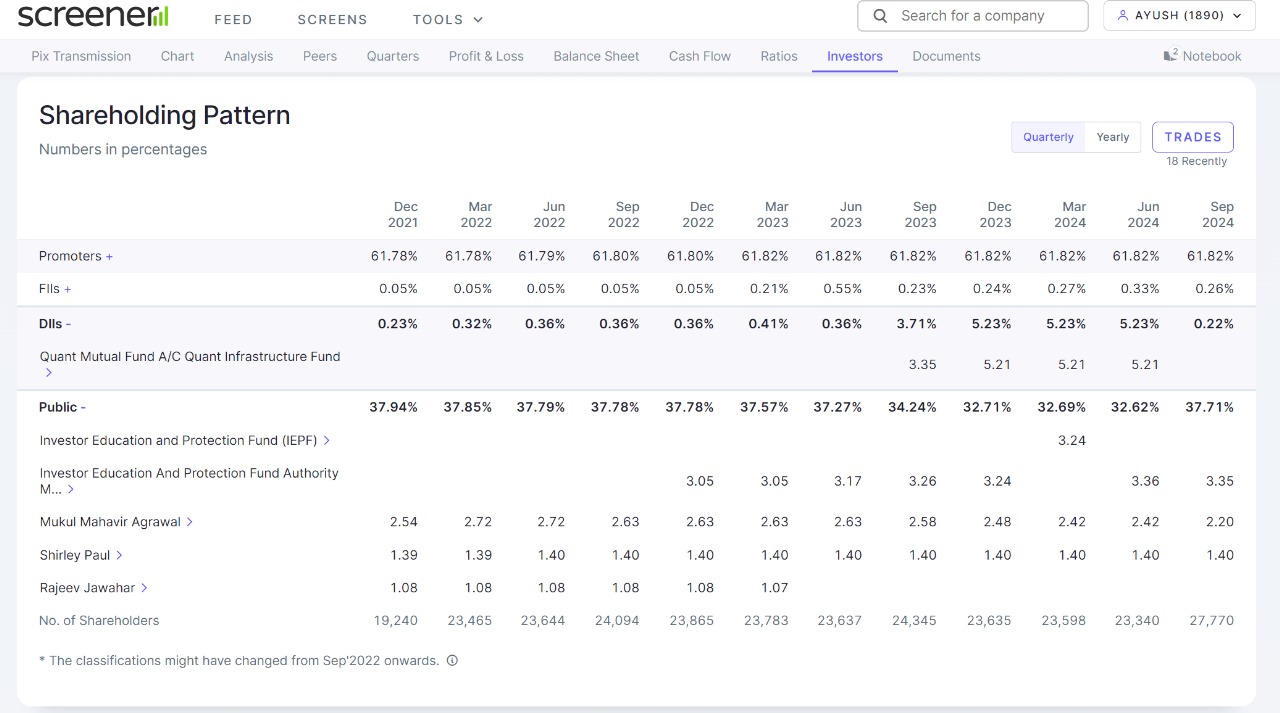

“Preferential issue and allotment of 29,79,579 equity

shares having a face value of Rs. 10/- each for an

aggregate amount of Rs. 10,79,27,80,032.75 (Rupees

One Thousand Seventy-Nine Crore Twenty-Seven

Lakh, Eighty Thousand Thirty Two and Seventy Five

Paise Only).”

https://nsearchives.nseindia.com/corporate/E2E_05112024091652_Reg30OutcomeCleansigned.pdf 1079 crore at 3622/- for 15% stake by LnT