I am not sure whether you chekc the history of investors and sales.

and I visited their website and their team is null

Please don’t get into that trap.

I am not sure whether you chekc the history of investors and sales.

and I visited their website and their team is null

Please don’t get into that trap.

Kindly share the source/link. Thanks

IKIO Lighting –

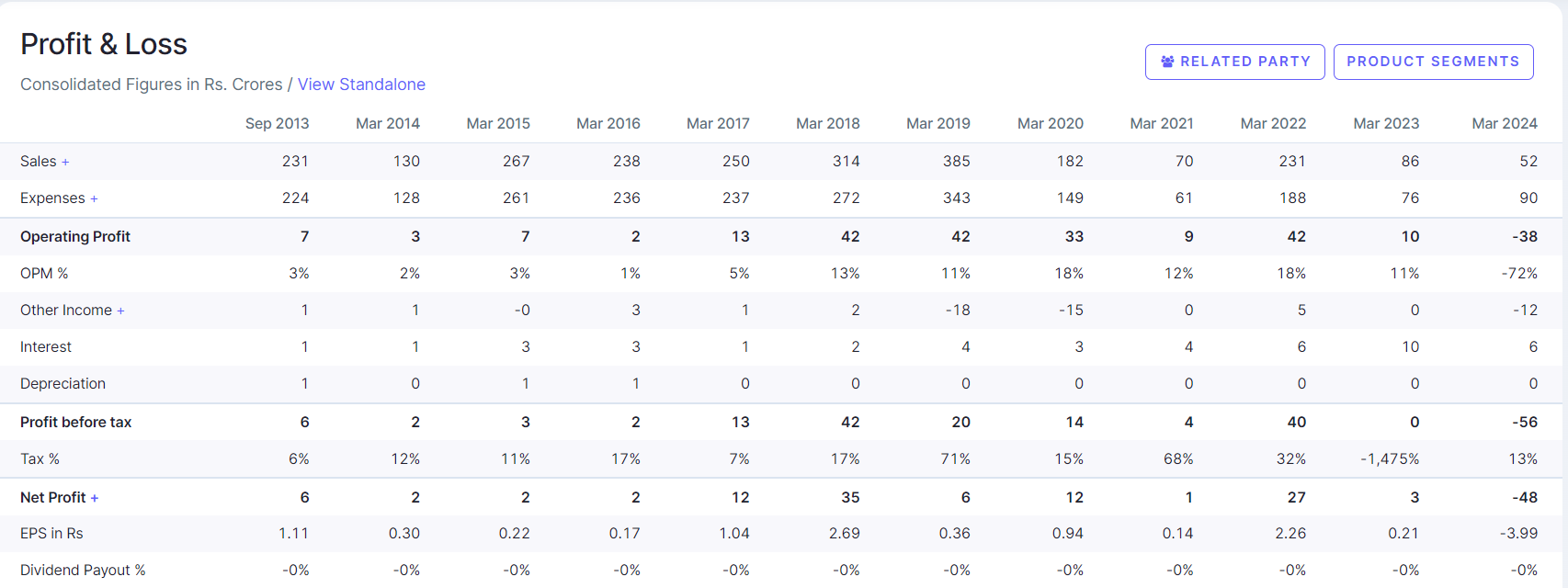

Q4 and FY 24 Concall and results highlights –

Q4 outcomes –

Sales – 94 vs 114 cr , down 18 pc

EBITDA – 17 vs 26 cr, down 26 pc ( margins @ 18 vs 22 pc. However the gross margins expanded by 7 pc to 42 vs 35 pc YoY !!! )

PAT – 9.5 vs 14 cr, down 31 pc

FY 24 outcomes –

Sales – 438 vs 446 cr, down 2 pc

EBITDA – 93 vs 99 cr, down 7 pc ( margins @ 21 vs 22 pc, however the gross margins expanded by 3 pc to 41 vs 38 pc YoY )

PAT – 61 vs 65 cr, down 7 pc

FY 24 – RoE @ 20 pc, RoCE @ 23 pc

Completed Block -1 of Greenfield expansion of 2 lakh sq ft. Trial production has started. Expected to complete Block – 2 of another 2 lakh sq ft by Mar 25. Have started construction for block -3 of another 1 lakh sq ft. Combined capex spend for all three blocks is around 200 cr with a total yearly revenue potential of 1000 cr

( incremental. It may take 3-4 yrs to reach optimum capacity utilisation for all 3 blocks )

Have started manufacturing new product segments like – Earphones, Smart Watches, Solar panel components

Accelerated weakness in Q4 is due to slowdown in Exports. Seeing descent recovery in Q1. Addition of overhead and employee expenses ( due new block -1 going commercial ) led to the dip in EBITDA margins in Q4

Expecting revenues to grow by > 20 pc in FY 25 with EBITDA margins in 20-22 pc band for FY 25. Expecting strong growth in H2 FY 25. A lot of incremental growth to be driven by newer products and categories that company is venturing into

Most of company’s existing LED Lighting facilities are dedicated to supply to Signify Ltd ( selling under the PHILIPS brand name in India ). With new capacities coming on stream, company to supply to additional customers

A lot of customers are visiting company’s new manufacturing block. Receiving very positive response from them. Likely to materialise into good long term partnerships / orders. The new facilities are likely to do asset turns of 5-6 times once they reach optimum capacity utilisation

Exports demand to GCC and USA are picking up. Overstocking related issues are behind

Expect domestic demand to pick up post election results

Company did admit that China + 1 is a significant tailwind for the company

Disc: holding, biased, not SEBI registered ( no other contract manufacturer in electronics space makes a double digit EBITDA margins. IKIO’s margins are generally > 20 pc !!! )

@Ashar_Mann

I was looking at the results of Creative Newtech and looks like their quarterly sales are down by more than 25%. Do you know any reason behind this?

There is massive difference between domestic and international realisation

Regarding chaman lal they have advatage only in maharani brand whose market is smaller

Krbl traded growth against margins as startegy before 2017 , sacrificing growth for margins

Now they are facing pressure as lt foods is eating there market shares and also iran regulations impact there buisness so margin fluctuations but these happened only in recent years before 2016 see krbl was maintaining very very healthy margins

Regarding ltf , company doesn’t immediately hikes price when cost goes up they maintain average ( e.g read last qtr concall when Mr arora addressed red sea issue)

This is old DRHP… They will refile it soon with updated data and valuation. IPO should come by December end as I heard from management

(post deleted by author)

Why there is sudden spurt in price. Do anyone know any recent developments in the company

Hope this helps…