Latest presentation out you can check data here

Latest presentation out you can check data here

FY25 I’m not sure because of Blinkit, otherwise Food Delivery PAT is already at 1800 crs odd run rate (Q4 PAT was 396crs)… losses from other verticals may take the console number to around 1000crs

FY26 onwards, Blinkit should start reporting profits (post expansion phase of FY25), assuming 2% PAT margin on GoV, we get around 800 crs profit (assuming 40k cr GoV by FY26). Food delivery PAT (assuming 25% growth) should be around 2250 crs. Total consol PAT of around ~3100 crs.

Note – above is conservative, because they have guided for 4-5% stable state EBITDA margins on GoV. The actual PAT margin may not too low from that guided number… but still I’ve assumed 2% on GoV. Further, while a 4x GoV growth has been guided, I’ve taken a conservative 40k cr as GoV when it can be higher since macro easing is likely in the following few months.

Also you can read any of the analyst report and these are the rough assumptions… infact most numbers are higher since we’re in a subdued macro environment and in all likelihood, Zomato should go back to 30%+ Rev growth & 31/32% PAT growth on FY25 base, which itself is likely to be atleast 25%

EDIT – Income on treasury may reduce since global rates are likely to come down… Zomato consol has a huge other income component as of now… in either case, Cash is a huge optionality in the business since they’re now generating upwards of 250 cr every quarter

NTPC eyes 10GW nuclear capacity, new subsidiary | Mint (livemint.com)

1.5 Lakh crores over 10 years if it goes according to plan.

Are there any websites official/unofficial which show accurate, real time subscription rates of all IPO’s (including that of SME’s) in India?

Are there any broking apps which also show real time subscription rates of IPO in the app itself?

Chemicals and pharma

I think I finally found the answer.

For Q4 FY24, volume increased 12 % Q-o-Q but selling price dropped by 6.5 %. Domestic volumes grew in high single digits while export volume growth was higher. Operating profit for Q4 was down from Rs.50 crore to Rs.45 crore.

Full year FY24 recorded a volume growth of 9 % in export segment while domestic was flattish, giving an overall volume growth of 2 %. Most of the growth was in non latex chemicals.

Margins declined but the situation has bottomed out, says the management.

Between FY22 and now, the latex market has degrown by 40 %. In the Q4 FY24 concall, one analyst noted that there is some improvement in this in the last one month.

Aggressive dumping from China and other markets continue. This will go on until domestic consumption in China picks up. Demand growth in key destinations such as US and Europe remains muted.

One analyst noted that the top three Chinese players are further adding capacity in accelerator as well as antioxidants.

Overall, things look grim, don’t they.

Meanwhile, work has begun on a Rs. 250 crore expansion at Dahej. Though overall capacity utilization is at just 65 %, the products that the company is planning to expand in here are running at peak capacity, hence the need to invest to capture further growth, says the management. The capacity will get operational in the second half of FY27.

Work on diversification into new chemistries is continuing, says the management but no further details are announced.

In the concall, one analyst noted that the molecules the industry uses have been as it is since past 50 – 60 years and nothing much has changed. Also in terms of the operational efficiencies through improvement in processes, most of the benefits have already been extracted. So the scope for incremental improvement is also limited. I wonder if this explains why almost nothing seems to change at NOCIL as well, not just in term of products and processes but thinking as well. As a debt free company in a capital-intensive business and an extremely efficiently run operation, I have often wondered why NOCIL cannot achieve more. The business remains hostage to what China does, with no efforts by the management to derisk or diversify. The Rs.250 crore expansion will not change this structural vulnerability to external factors.

The company is sitting on more than Rs.400 crore of cash and generates almost Rs.150 crore of FCF per year. If nothing else, annual cash flows are good enough to buyback a whopping 3 % of share capital every year. Even the appointment of a new CEO – often a harbinger of change – seems to have not made a difference. Some out-of-the box thinking, some risk taking, some dynamism is what I would like to see at NOCIL.

(Disc.: Invested)

Gambling/Casino industry because of the GST demand notices.

Few more points:

In India, the peak season for fishing is August-December and the slack season is January-May. Fishing is not allowed in Indian waters during June-July, as it is the monsoon season. Fish meal and fish oil production follows the same season as fishing. The output is stocked to cater to the demand of domestic and exports market.

Industry is dependent on fish landings in marine ecosystem (salt-water) and if there is any natural phenomenon (like typhoons) causing less fish landing then the industry struggles. There doesn’t seem to be any pricing power in case of supply shortage as the customers are businesses who sell to low-income aquaculture farmers

It is vital to note that, unavailability of raw materials i.e, fish species required to produce fish meal and fish oil acts as the major constraints in the fish meal and fish oil industry rather the production capacities available. Company is operating at ~10% capacity currently due to lower fish landings compared to 5 years back.

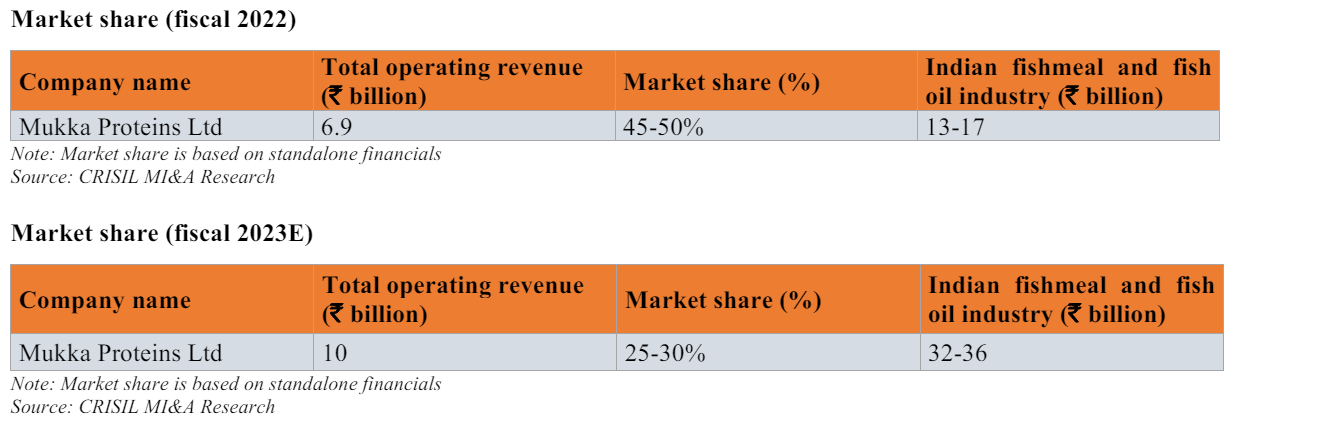

Company has lost a lot of market share in both exports (50-60% to 9%) and domestic market as well (50% to 30%). Major concern on sales here

Due to all these reasons, the company has opted to enter into insect protein as an alternative to fish meal. But the scale is low (~1% sales), company just has a 1 year tender with 1 municipal authority to farm BSFs on their waste dump. No idea if this get renewed. Could be a game-changer but this it would be speculation at this stage as there’s no visibility on winning more tenders

Customer concentration risk: Top 2 (two) customers as on September 30, 2023 are associated with us for over 5 (five) years and contributes 42.17% of our revenue from operations

According to WPI data, marine fish prices keep increasing since Jan 24 which will adversely impact them.

I might be looking to change my end even on my smallish investment

Agree, this LMV3 capacity expansion may not add significantly to its kitty.

But I see it as positive for a PSU company which is trendy And forward looking.

overall Order book goes on increasing and execution quality not bad for a PSU.

When I entered the stock @Rs 1200 a piece in 2022, I had a lot of hesitation, But after having entered the stock and after a little bit of research on Atma Nirbhar Bharat , i was excited to put more money in to it during its journey from 1200 to 1800… it went up to Rs 3800…and then there was a split 1:2 to bring it’s price back to 1900 and now the journey up to Rs 4700 ex split

I am proud to own this stock since then…no looking back as long as the order book , execution quality , and margins remain healthy.

Being a PSU stock, i keep getting good dividends irrespective of bear or bull market…