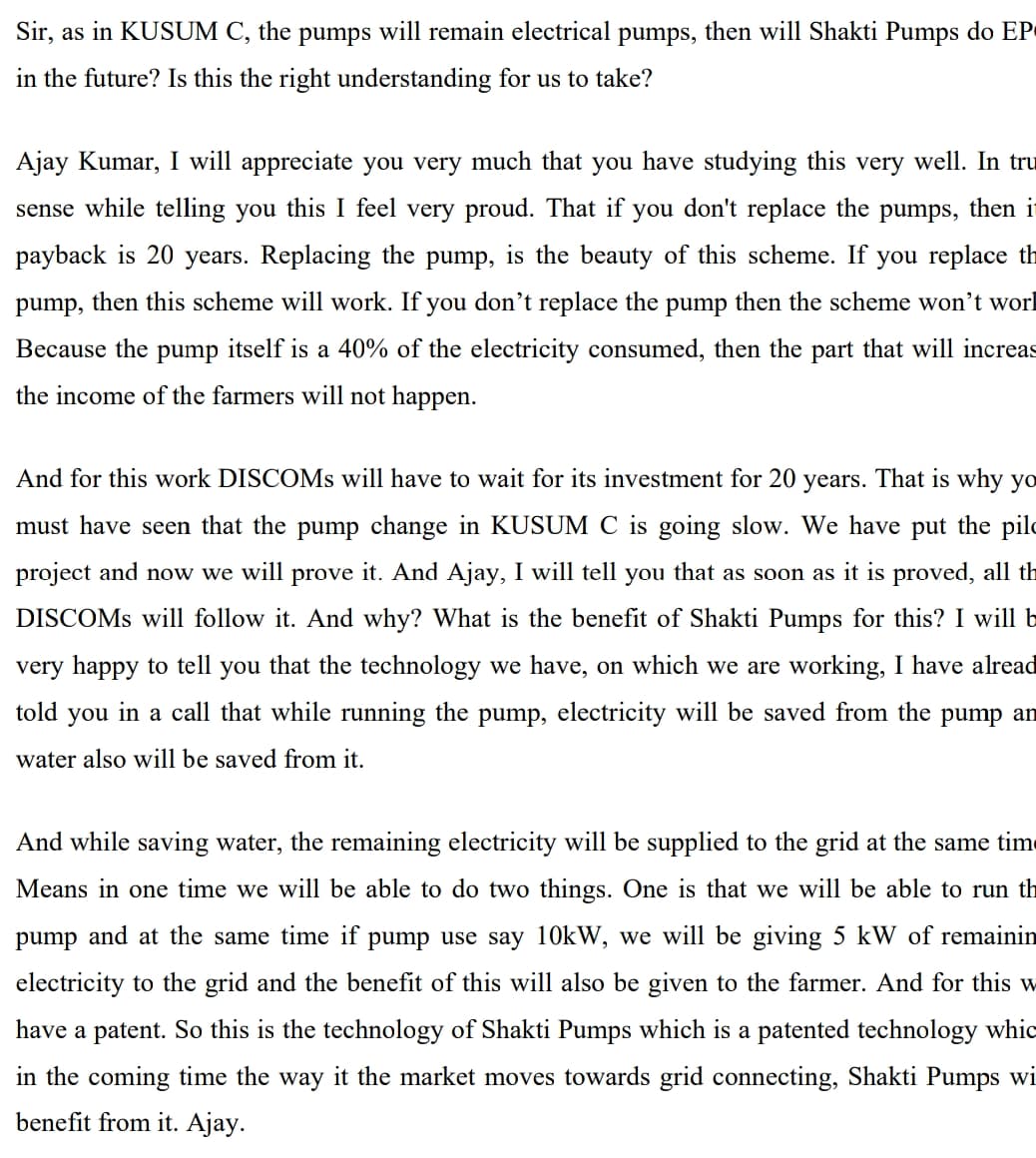

Interesting information from the recent comcall. Promoter thinks that for Kusum C scheme the pump needs to be replaced to realize the extra energy savings and Shakti pump’s patent has value. This is going to be huge once/when it gets validated considering the size of kusum C scheme. The ajmera pilot holds immense significance in my view.

Management has also given a guidance of 500 cr again for q3 and Shakti pumps bulls have been proven right so far. Not that I am complaining. ![]()