one very crucial red flag: frequent resignations of compliance officer (all officers resigning within 1 year)–>in 2020, 22,23,24. Does anyone have any inside info? why so much frequeant resignation in this KMP post?

Posts in category Value Pickr

Zomato – Should you order? (02-06-2024)

Sir, I implore you to read their financial statements.

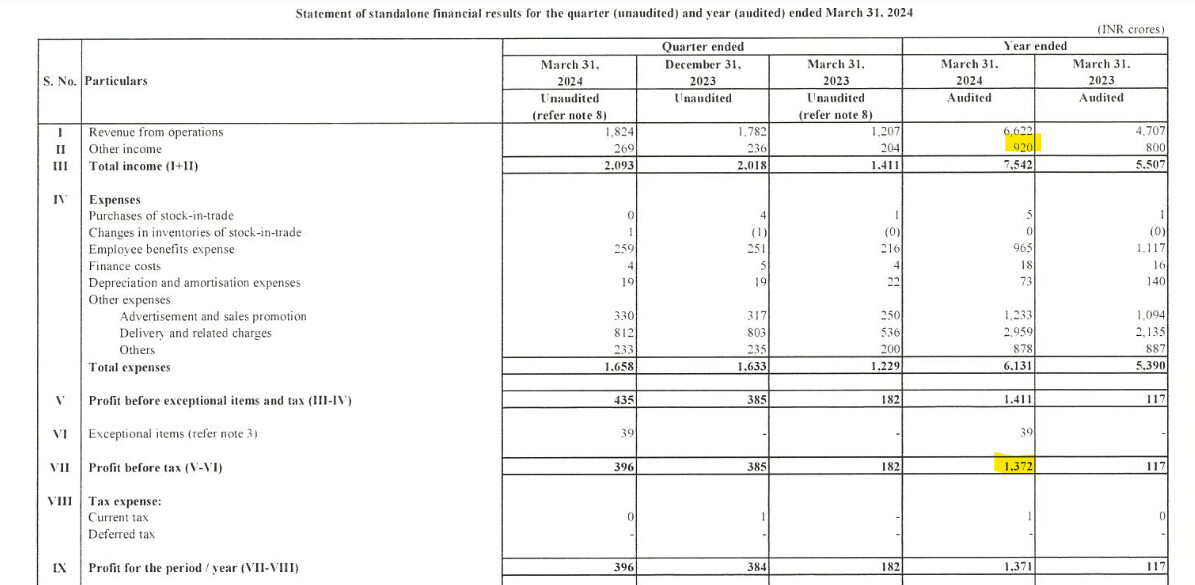

Zomato posted a standalone PAT of around 1400 crores and Q4 standalone PAT was ~400 crs. Even if you exclude other income (treasury), Zomato is PBT +ve with growing profit pools. See screenshot below:-

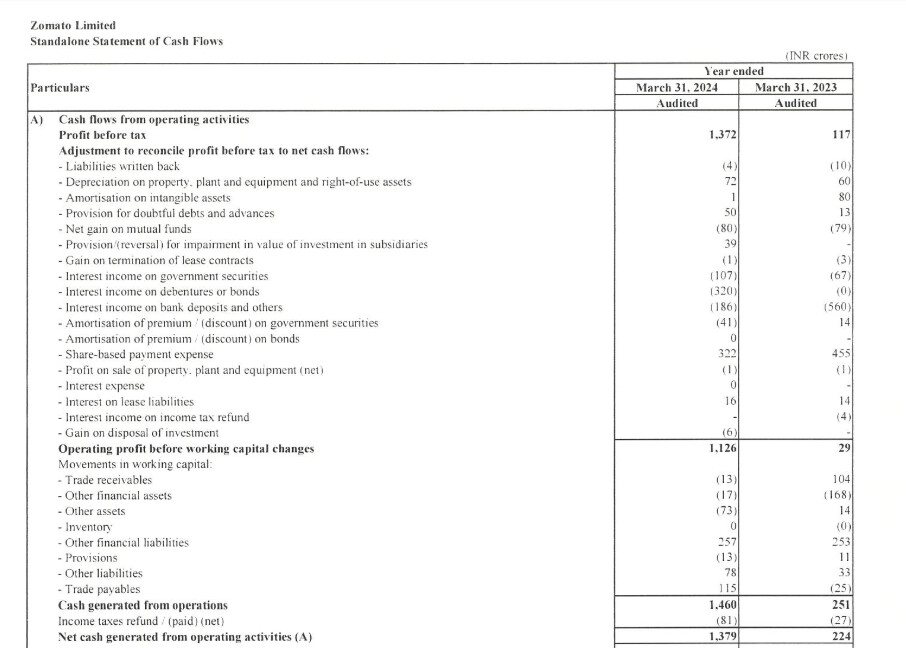

On the point of cash flow, attaching their cash flow statement:-

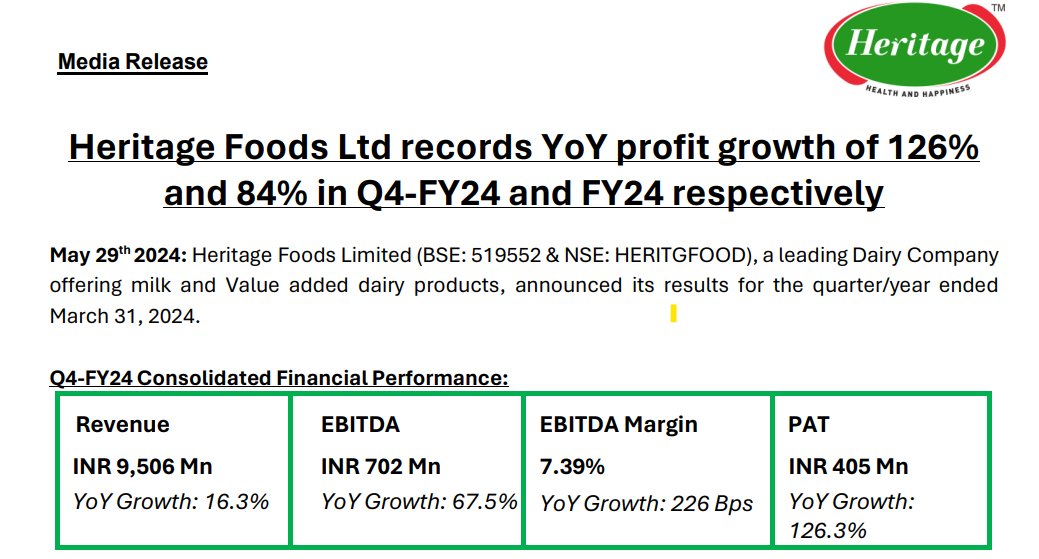

Heritage Foods Ltd (02-06-2024)

58% of revenue comes from milk however future business outlook based on management commentary includes a focus on increasing VAP share to 40% of revenue (which will take margin even higher), expanding the product portfolio (already launched 2 new ice cream: Fig Honey Cashew & Berry Burst & Vibez Ice cream) and penetrating new geographies.

Furthermore, Heritage Nutrivet Limited robust Top-line growth YoY 50% and bottom line YoY grown Exponentially 360%.

PG Electroplast – Potential for cooler returns? (02-06-2024)

- PG Electroplast Limited targeting 46% growth in group operating revenue for the next financial year.

- Company aims for a consolidated net profit of at least INR 200 crores.

- Anticipated 44% growth in the product business for the upcoming financial year.

- Focus on developing cost and product leadership for room ACs and washing machines.

- JV partnership established with Goodworth Electronics for TV and hardware business.

- Jaina Investments close to INR 6 crores invested in the TV business, potential additional INR 5-6 crores.

- Jaina provides sourcing capabilities and credit from Chinese vendors for TV kits.

- Potential update on IT hardware PLI orders post-election mentioned.

- Plastic molding margin at 7.5% and electronics at 2%, driving growth in the product business.

- Expected turnover of INR 2400 crores in the product business for the next year.

- Seasonality shifted, with RAC business starting late January and extending to late June.

- Actively engaged in discussions with clients for new products and opportunities.

- High interest in RFQ and RFP.

- Capex set at around INR 370-380 crores for infrastructure development.

- Optimistic outlook for revenue growth in ACs, washing machines, and new categories.

- ROCE target set between 15-16% pre-tax for new projects.

- No immediate plans for high-margin, low-volume businesses like aerospace.

- Aiming for a slight improvement in pre-tax ROC E of about 20%.

- Emphasis on growth and seasonality influencing the target of achieving a 25-26% ROC E by FY ’26 or ’27.

- Cash balance of about INR 180 crores and a gross debt of INR 360 crores reported by PG Electroplast Limited.

Zomato – Should you order? (02-06-2024)

Zomato is only EBIDTA positive due to Blink IT.

And Blink IT contributes much of the cash positive to Zomato than their own business.

From the likes of Kenneth to FII are more interested towards new age tech business however they are waiting for a correction to happen.

Sandeep Kamath Portfolio | Momentum Investing (02-06-2024)

Well, nothing rocket science. Past 6-12 months stock performance overlaid by RSI and Stochastic parameters. Point is to buy stocks that have done well in the preceding 6-12 months…

What I can add is also this – its largely irrelevant what exact methodology you use to rank stocks if you want to do factor investing. I back-tested multiple strategies and they all gave market-beating returns…the challenge is to stay put with the strategy over the long term which is not easy.

Zomato – Should you order? (02-06-2024)

A similar story from The Arc

Heritage Foods Ltd (02-06-2024)

Heritage has seen growth in Odisha. Atleast in Bhubaneswar, I saw a lot of their products. But the pricing is off. Their buttermilk is Rs. 20 compared to Rs. 15 of Amul.

Sandeep Kamath Portfolio | Momentum Investing (02-06-2024)

Well, by any conventional valuation model, some of these names were probably over-valued even in Jan when I went live with this portfolio…but then some of these are up 20% or more in the last 4 months…

Thats the whole premise of factor based investing…you detach yourself from everything else other than price. So while price dictates my entries, price will also drive my exits.

Zomato – Should you order? (02-06-2024)

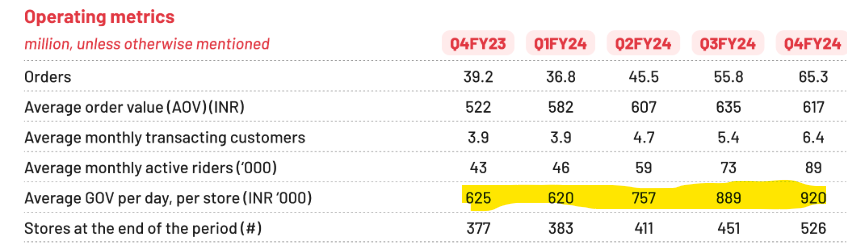

This might be a little overblown:-

GoV per store per day (avg. Q4) = 9.2 lacs (mature stores would have upwards of 10 lacs)

Total GoV in a year = 33.58 crores

3% commission = 100 lacs

Salary + Rental (Annual) = 25 lacs + 25 lacs = 50 lacs ( i have assumed 6-7 employees… 20 seems too high)

Overheads = 15 lacs

Net income to franchise owner = 35 lacs

Some points to note:-

- average GoV per store per day likely to be significantly higher for mature markets of Delhi. At 15 lac per day (assumption) for mature stores, net income bumps upto 60 / 70 lacs

- GoV per store per day itself is trending up for the company

- At current net income levels, payback period for franchise owners is under 2 years (even if I include deposit which is refundable)

- As categories get added and Blinkit take rates go higher, some of it will percolate down to franchise owners, strengthening the model

Key Monitorable

- For q-com to succeed, GoV for MT / GT have to reduce in key urban markets – NCR, BLR & Mum – so keep an eye out for SSSG for Dmart, Reliance Retail, etc… the SSSG has to show stagnation or decline – same for Amazon GoV