@Sandeep_Mehta1 There is another thread for it. You can get it there.

Posts in category Value Pickr

Lt foods (daawat) (01-06-2024)

Court has rejected oriental insurance stay application. Ltfoods will receive the amount 161cr along with 6% interest.

Smallcap momentum portfolio (01-06-2024)

Vishwanath – can you please share the microchip PF?

Microcap momentum portfolio (01-06-2024)

Update for entry on 3rd June 2024.

50D EMA (20368) > 200D EMA (18281); hence, we can continue without any change.

- KPIGREEN

- RTNPOWER

- KIRLOSENG

- PURVA

- TECHNOE

- NETWEB

- IFCI

- CHOICEIN

- ARVIND

- VOLTAMP

- KESORAMIND

- STAR

- ANANTRAJ

- JKIL

- MSTCLTD

- TARC

- KIRLOSBROS

- JYOTICNC

- AZAD

- THOMASCOOK

- IIFLSEC

- WOCKPHARMA

- ELECTCAST

- JPPOWER

- ASTRAMICRO

Based on A → Z for easy tracking:

- ANANTRAJ

- ARVIND

- ASTRAMICRO*

- AZAD*

- CHOICEIN

- ELECTCAST

- IFCI

- IIFLSEC*

- JKIL*

- JPPOWER*

- JYOTICNC*

- KESORAMIND

- KIRLOSBROS

- KIRLOSENG

- KPIGREEN

- MSTCLTD

- NETWEB

- PURVA

- RTNPOWER

- STAR

- TARC

- TECHNOE

- THOMASCOOK

- VOLTAMP

- WOCKPHARMA

Exits:

BALMLAWRIE, INGERRAND and TVSHLTD make an exit.

MOIL, SCI and TIMETECHNO stay within the top 30 and hence remain.

Entries:

IIFLSEC, JKIL and JYOTICNC make an entry.

AZAD is higher on momentum but is less than 6m on the bourses; hence has not been considered.

ASTRAMICRO and JPPOWER cannot enter as there is no vacancy.

Microcap momentum portfolio (01-06-2024)

@hariharancj You have nearly stolen my update!!! Small differences; all stocks in the list are the same. Order is slightly different. Also, AZAD is less than 6 months. Therefore, I will not include in my pf for now. Will post my update.

Curious Case of Coal India (01-06-2024)

As per news, Govt is looking to double Coal India’s production, which if translates to doubling profits in 6 years, wudbe 12% annual growth. Can we expect any positive PW re-rating for coal India?

Anyone who has view on Coal India?

- With renewables picking, how long would Coal usage in energy production rise?

- Some Thermal power plants have been given approvals to increase coal production in their captive mines. How do we see this impacting Coal India’s production

- Any other usage of coal which may increase in next few years as coal India’s sale to Thermal plants would fall in coming years?

Considering these points, Does it makes sense to hold Coal India (considering Dividend & Price increase)?

Smallcap momentum portfolio (01-06-2024)

@james_kerala This smallcap pf has given 2.7% from April 1st to May 31st. The other pf based on microcap index has given around 8% for the same period.

Sky Gold ltd. – Will it reach the sky? (01-06-2024)

No idea personally but he does analyse high flying shares and cuts down to the bone.

So mostly where there is divergence betwwen B/S and P/L statement and Cash flow

WPIL Ltd – Global Water Pumps (01-06-2024)

Q4 FY24 Concall notes

Domestic Operations

- Total Domestic Revenue: Rs. 1,077 crores

- Growth: 7.4% YoY

- Domestic Product Business: Rs. 261 crores

- Growth: 19% YoY

- Order Book: Rs. 348 crores

- Domestic Project Business: Rs. 816 crores

- Growth: 4% YoY

- Record Order Execution: Rs. 343 crores in Q4

- Order Book: Rs. 3,054 crores

- Notable Development: Madhya Pradesh Jal Nigam contract termination, 8 other projects on track

International Operations

- Order Book: Rs. 458 crores (as of 31st March 2024)

- Gruppo Aturia: Strong demand in MENA region, robust aftermarket revenues

- WPIL South Africa: Focus on water sector, aftermarket contracts from Eskom Power

- Sterling Pumps and United Pumps Australia: Robust order books, strong growth expected

- WPIL Thailand: Record revenues in FY24, continued momentum expected

Strategic Developments

- Navy Order Execution: On track, contributing to revenue growth from FY25 onwards

- Product Division Outlook: Improved due to new products for oil, gas, sewage, and drainage

- Inorganic Opportunities: Pursuing acquisitions, positive outcomes anticipated by mid FY25

- Focus on Core Industrial Pump Business: Following successful divestment of Rutschi’s nuclear business

Challenges and Disputes

- Madhya Pradesh Jal Nigam Contract: Disputed termination due to delayed land allotment, exploring contractual remedies

Future Outlook

- Strong Revenue Visibility: Positive outlook for FY25 with growing order book and successful project executions

Profitability

- Domestic and International: EBITDA margins approximately 17%-18%, within the band of 15%-20%

Navy Order

- Framework Agreement: Rs. 17-18 crores

- Completion Timeline: Expected within the next 6 months (ongoing for 12 months)

Cash Balance

- Current Balance: Rs. 630 crores

- Planned Deployment: Focus on inorganic growth opportunities (actively pursuing acquisitions, results expected from mid-FY25)

Sundry Debtors

- Increase: Rs. 288 crores due to high invoicing in March

- Collection: Expected to be collected in the normal course during the first quarter

Madhya Pradesh Jal Nigam Contract

- Terminated Contract Value: Rs. 155-160 crores

- Remaining Contracts: 8 contracts in various stages worth Rs. 1,100 crores

- Order Book Status: Terminated contract value removed from the order book

- Reassignment Status: Contract not awarded to anyone else yet

Working Capital

- Increase: From 79 to 120 days

- Reason: High invoicing in the last quarter, particularly in March

- Normalization: Expected to normalize by the end of the first quarter

Project Business

- Scope: Turnkey EPC projects covering water, irrigation, industrial, and municipal sectors.

- Order Book: Includes AMRUT and JJM projects, majorly in Assam, West Bengal, and Madhya Pradesh.

- Project Sizes: Rs. 200-600 crores.

Competitive Landscape

- Competitors: Range from large players like Larsen & Toubro to smaller companies.

- Tender Participation: Varies; larger projects attract fewer participants.

Margins and Financials

- EBITDA Margins: Targeting 15%-20%.

- Order Book Impact: Mitigated loss of Rs. 155-160 crore contract through other projects and bank guarantees.

Market Trends

- Segment Dynamics: Increase in rural water supply projects, offsetting decrease in irrigation projects.

- Future Opportunities: Continued demand with significant pipeline projects worth Rs. 1-1.5 lakh crores annually.

Execution and Payments

- Consistency: Similar execution and payment conditions compared to the past.

- Sector Diversification: Selective participation in sewage projects; balanced focus across water sectors.

Financial and Operational Outlook

- Revenue Growth: Current revenue at Rs. 800 crores; ample business opportunities for growth.

- Long-term Sustainability: Sector anticipated to sustain and drive revenue growth.

Product Segment Overview

- Execution Timeline: Orders typically span 4 to 8 months, depending on product type.

- Revenue Growth: Diversified product portfolio yielding strong growth and profitability.

- Segment Focus: Strong order book from growing segments like Navy and sewage drainage.

- Profitability: Margins remain robust, targeted between 15% and 20%.

Recent Orders

- Nature of Orders: Framework orders with long-term implications.

- Significance: Represents potential recurring source of orders over 20-30 years.

Domestic Order Book Analysis

- FY23 vs. FY24 Order Book: Decrease from Rs. 36,410 million to Rs. 30,543 million.

- Reasoning: Slowdown attributed to recent elections.

Revenue Growth Trajectory

- Expectations: Anticipating good growth in both project and product segments.

- Execution Challenges: Earlier challenges, like supply chain constraints, gradually addressed, paving the way for streamlined execution and growth.

Pipeline and Opportunities

- Execution vs. Booking:

- Balancing focus on both execution and booking new orders.

- Inquiry Pipeline:

- Significant inquiries in various sectors, ensuring no challenge in replacing current revenue levels.

- Opportunity Scale:

- Tenders in water segment alone range from Rs. 5,000 to Rs. 8,000 crores, providing ample opportunities.

- Geographical Expansion:

- Exploring opportunities in multiple states and sectors for a more balanced portfolio.

- Order Book Growth:

- Expected to align with revenue growth and industry norms.

Ganesh Benzoplast – Cash rich chemical storage/tank king (01-06-2024)

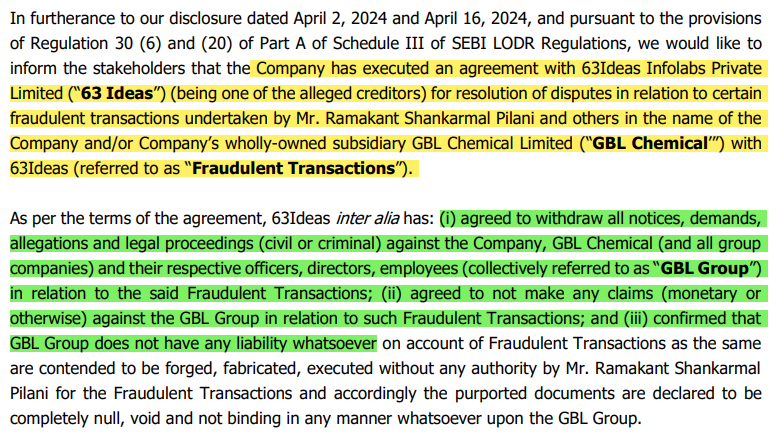

One Key trigger going forward can be the relief received by the company regarding the potential liability as a result of the fraudulent transaction entered by Ramakant Pilani (who is not regularly involved in the business anyways).

Interestingly, Ramaknat Pilani’s son has also resigned from the board, so the business will be led by Rishi Pilani & co. (who were as it is responsible for the turnover & doing all the talk with the investor community).

It is very difficult to understand the holding structure as majority shares are held by their group co., However, there can be a possible supply overhang if Ramakant Pilani & co. decide to exit their holding completely.

Operationally, Q4 results were pretty decent on the LST segment considering their capacity is already operating at full utilization & growth will start flowing only after the commercialization of the LPG terminal.

Concall on June 5th will be really interesting!