In January, warrants issued by the company got converted to actual shares. This leads to the dilution of shareholding

Posts in category Value Pickr

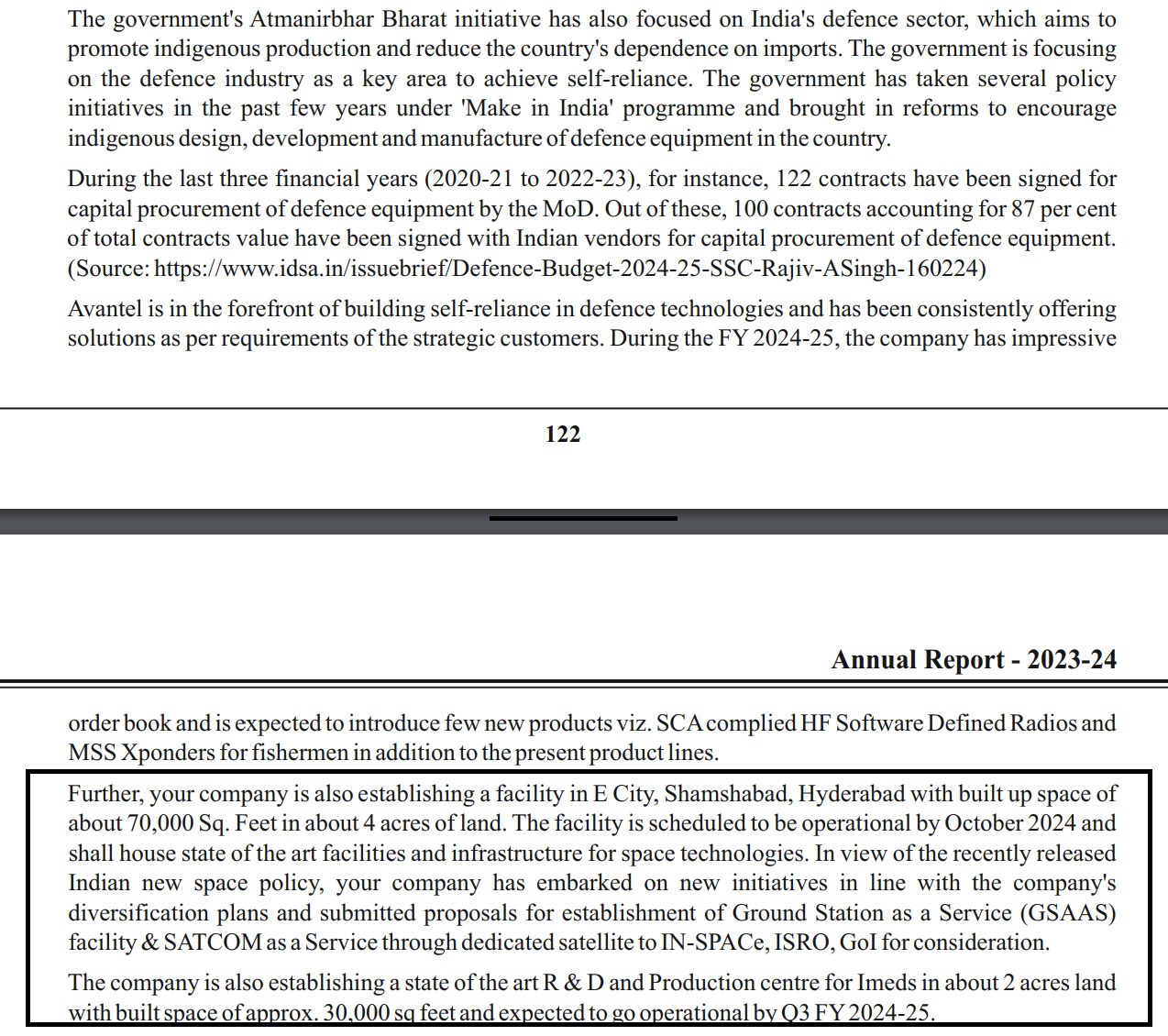

Avantel (01-06-2024)

AR 2023-24

All E Technologies, making businesses ready for AI (01-06-2024)

very nicely articulated Aadhar.

All E Technologies, making businesses ready for AI (01-06-2024)

Everything is good for the company except for Ajan Mian’s conservative approach. There is around 100 crore cash on the balance sheet, so the company should do aggressive marketing and try other business applications. The promotor looks very honest and is taking time to find the target company.

The Anti-Portfolio (01-06-2024)

@LarryWink After taking a preliminary glance, on most fundamental parameters, i find Shilchar and Indo Tech better companies than TRIL…Am I reading it wrong?

Transformer & Rectifier India Limited (01-06-2024)

On most of the fundamental parameters, I find Shilchar and Indo Tech are better companies than TRIL …Am I reading it wrong?

Carysil (earlier Acrysil) – Kitchen sinks (01-06-2024)

Just an update post. Sold my holding in carysil post Q4 result. Valuation comfort not there and growth seem to be slow. Not too happy with acqusitions as a way of growing business. Looking at better opportunity with some.growth visibility .

May look at re enter at a convenient time

The Anti-Portfolio (01-06-2024)

Vikaj ji…me again ! ![]()

So i tried to check on them after trading & holding after an year ![]() >https://nsearchives.nseindia.com/corporate/TRIL_08042024153813_PresentationQ4202324.pdf

>https://nsearchives.nseindia.com/corporate/TRIL_08042024153813_PresentationQ4202324.pdf

They do seem impressice in their chic presentation

| Revenue | 1270 cr |

|---|---|

| Export | 140 cr |

| EBITDA margin | 12.93% |

| PAT | 3% |

| Order Book (on 23.05.24) | 2941 cr |

| Enquiries under negotiation | 17000 cr |

Just like I could say, without knowing much and trading in the 70s, then holding since the 90s, and now after it became 7% of PF, ऊँट के मुँह में जीरा ![]() .They say results are not by chance but are the result of meticulous planning and execution of key strategies. To my not-so-intelligent brain, I presume all listed names offer a rosy picture if the story is good and paint a soothing picture if the story isn’t.

.They say results are not by chance but are the result of meticulous planning and execution of key strategies. To my not-so-intelligent brain, I presume all listed names offer a rosy picture if the story is good and paint a soothing picture if the story isn’t.

However, I think transformer exports have opportunities, especially in the US:https://www.woodmac.com/news/opinion/supply-shortages-and-an-inflexible-market-give-rise-to-high-power-transformer-lead-times/.

While they are barely profitable, I get pumped up to take a bet based on forward-looking guidance. I wish someone could teach me to calculate forward PE ![]() . Could it turn out to be a bait? What an expert would have done in such scenarios?

. Could it turn out to be a bait? What an expert would have done in such scenarios?

Edit – Their export is 11% now & plan to increase it to 25%.Last year they recieved 2000 Cr orders and if they are negotiating 17000 crore. What can stop them from 3000cr at top ?

Carysil (earlier Acrysil) – Kitchen sinks (01-06-2024)

Carysil has done clear case of misguidance.

Q3 they had the conviction to scale to 1000cr stock rose up to 1100.

Some of the insiders sold at peak.

Now they are guiding of achieving 1000cr with inorganic acquisition,if at all it happens.

- Always take guidance of aggressive commentary management with pinch of salt. Those who are tracking this company knows it very well.

Senco Gold: Upcoming gold story! (01-06-2024)

Q4 FY24-

Guided for margin expansion from 7.3% to 8%

Guided- Top line-18-20%, Bottomline-15-20%

– Efforts to increase stud ratio by 1-3% annually to mitigate price pressure and improve gross margin and EBITDA.

Company added 23 showrooms in FY24. Total showroom count is 159. Company guided to open 20 showrooms in FY24 and exceeded the guidance.

- Management plans to add between 15 to 20 new stores in the upcoming year.

Stud ration increased from 10.4% to 11.4%(In North- stud ratio is 17.2, higher than average). Stud ratio is less compared to Titan and Kalyan but the trajectory is upwards. Stud ratio is the % of diamonds in a gold ornament. Jewelers get more margins in diamonds. Hence, more the stud ratio better the profit margins.

– Focus on growth will be primarily in Eastern and Northern India, with a mix of West and South.

- Optimum Gold Metal Loan (GML) percentage target is around 75% to minimize borrowing costs.

– Strategic locational advantage in Kolkata helps mitigate pressure on margins compared to competitors.

Revenue grew 40% and PAT grew 24% YoY. Senco grew faster than Titan and Kalyan in Q4. Senco exceeded the sales growth guidance of 20%.

Showroom growth of 17%, SSSG Growth of 19%, sales growth of 29%, EBITDA growth of 18.6% and PAT growth of 14.2% for the full year.

Company achieved 13% volume growth in Gold and 18% in Diamond

The Inventory value increased from 1,885Cr to 2,457Cr in anticipation of Akshaya Tritiya and higher gold price.

Inventory turnover ratio is 2.4x and inventory days is 151 days.

ROE went down from 19% last year to 15.7% due to high showroom roll-out

Key Financial Metrics:

-

Revenue growth of 28.5% in FY24

-

PAT growth of 14.2% in FY24

-

Total revenue of Rs. 5,240 crore in FY24

-

EBITDA margin at 7.3% with a target to increase to 8%

-

Average sale price (ASP) of Rs. 41,000 for the full year

-

Average ticket value (ATV) in the range of Rs. 63,000

-

Gross margin for the current year at around 15.3%

Management Commentary Highlights:

-

Senco Gold had a successful year post listing in FY24, focusing on wealth creation for shareholders and stakeholders.

-

Launched new initiatives like metaverse platform, ONDC enlistment, and tie-up with eBay for global market access.

-

Opened new stores in Central India and expanded product portfolio with 23 new collections.

-

Revenue from operations grew by 28.5% in FY24, with retail business growth at 25%.

-

PAT grew by 14.2% to Rs. 181 crore in FY24.

-

Focus on customer acquisition with 45-50% new customers and 55% repeat buyers.

-

Introduced new brand SENNES for lab-grown diamonds and leather accessories.

-

Emphasized premiumization, customer value chain, and brand positioning for ASP increase.

Insights into Business Verticals:

-

North region stores have a stud ratio of 17.2% and average sale per store of Rs. 27 crore, showing growth potential.

-

Retail growth in North at 22% with SSSG of 19%, indicating a growing business in the region.

-

Export income contributed to higher revenue growth in 4Q, with specific details on export income not provided.

Forward Guidance & Outlook:

– Focus on expanding in East and North regions, with plans to add 15-20 stores in the coming year.

-

Continued efforts to capture market share and stabilize profitability in the face of competition.

-

Opportunities for growth in North region, with a stud ratio of 17.2% and average sale per store of Rs. 27 crore.

Export income contributing to revenue growth, with potential for further expansion in the export segment.

Overall, Senco Gold had a successful year in FY24, with strong revenue growth, focus on customer acquisition, and strategic initiatives to drive business expansion. The company remains optimistic about future growth prospects and is committed to delivering value to shareholders.