Holding it for the longer term for now. Trigger to exit would be next qtr results if management does not walk the talk. If election results are an upset, the larger India story will be questioned in my view irrespective of a particular stock

Posts in category Value Pickr

Nithin’s Portfolio (31-05-2024)

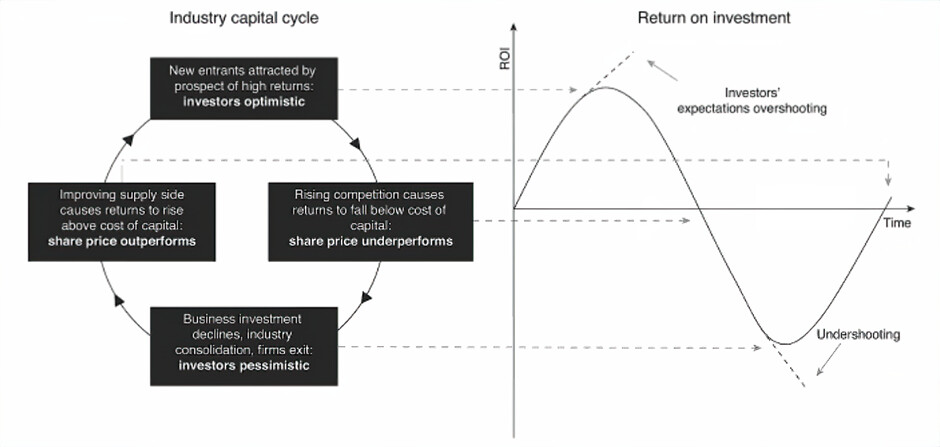

We are in the Business Investment Declines, Industry Consolidation, Firms Exit: Investor pessimistic phase for. (Phase iii)

- Pharma

- Chemicals

Arunjyoti Bio Ventures Ltd – A new co-packer in the arena? (31-05-2024)

Company Overview:

Company was earlier named as Century 21st Portfolio Limited – used to trade in equities and commodities, had wealth management and portfolio and software development operations.

Name was changed to Arunjyoti bio ventures ltd in FY 2015.

However the company did not turn around after new KMP from 2015 to 2022.

But looks like some turn around has been brewing since 2022 July & below info indicates the same:

In July 2022 – The current promoters issued an open offer, took over majority shareholding & also change in management control.

A brief about current promoters background: Has ran distribution business of non-alcoholic beverages for MNC’s in the state of Telangana & Andhra Pradesh for past 20 years.

Immediately after takeover – Company now purchases 2 lands – one in AP ( 3acres, 53 cents) & one in Telangana ( 2 acres 17 cents) on 24th aug & sept 1st 2022.

Beverage business: March 8th 2023 – Company announces to set up two beverage plants in above two land parcels.

Followed by trial production commencement from 18th May 2023.

So in a timeframe of 1 year – New promoters took charge, purchased land & setup beverage plants with initiation of trial production.

Now, there were further amendments & lets take a look below:

- Increase in authorized share capital from 3.5 crores to 19 crores.

- Issue of rights @ 20/share. Also, promoters extended a loan to the tune of ~19 crores & conversion of the same within the objects of rights issue.

Business :

Company has two divisions now:

- Beverage production line for MNC company – also known as co-packer services for MNC’s ( Comparable listed entity could be Hindustan Foods), though for Arunjyoti it looks like the journey has just begun.

- Distribution of the same produced beverages from plant.

Capacities for beverage production:

Telangana plant has 24,000 cases per day with three lines & AP plant has 17000 cases per day with 2 lines. MNC has itself invested for a new line as they are launching a new product & do not want the co-packer to take the risk.

MNC to provide all the feedstock needed for production of beverages. Hence the raw material cost is nil as observed in Q4 FY 24. The only expense on P&L by the company is utilities, employees, warehouse, depreciation & finance. Company also states that they will be venturing in to capacity enhancements & possible integrations across value chain.

Financials:

Although there is a huge spike in sales this year – I assume a lot of growth to be coming in from next quarter due to stabilization of capacities and systems in place for procurement, production & distribution.

Sales: FY 24 : 20.4 crores.

Debt: After rights conversion of promoter loans – I assume debt numbers look different than reported as of 31st March 2024 which is 44 cr. It should be around ~24 crores after debt to equity conversion of unsecured loan extended by promoter.

Earnings are not +ve yet, but with Q1 being a hot summer, I expect sales & earnings to be better than FY 24 Q4.

Market cap looks expensive on trailing TM performance.

In public shareholding recently a couple of big names got added in April 2024.

Disclaimer: Added in family account.

HDFC Asset Management Company (31-05-2024)

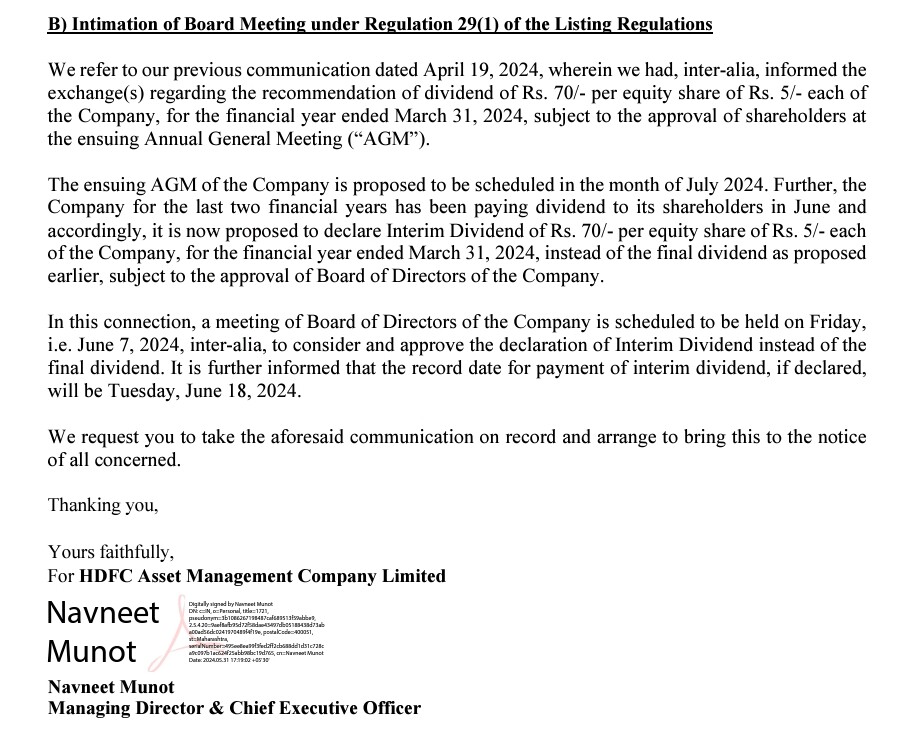

There must be no such rule that states that an interim dividend should not be declared in a FY, for the FY that has finished. So the interim dividend is for FY 24, and as FY 25 is going on, such interim dividends will be announced in the future.

Solex Energy – Undervalued Solar PV Manufacturer or Microcap Value Trap? (31-05-2024)

Disclosure: I am not a financial advisor. This is for informational purposes only. Please do your own research before making any investment decisions.

I am invested in the stock with 200 shares at ~1517 each.

Solex Energy (SOLEX) is an Indian company engaged in manufacturing solar photovoltaic modules and turnkey solar solutions. They currently have a manufacturing capacity of 700MW in Gujarat and are planning a significant expansion.

Growth Drivers:

- Massive Capacity Expansion: Solex is set to add a whopping 800MW capacity by September 2024(Solex Energy buys 800 MW module production line from Wuxi, GMEE Solar – pv magazine India), more than doubling their current production. They further plan to reach 4.5GW by FY26, indicating an aggressive growth strategy.

- Government Push for Renewables: The Indian government plans to add around 40GW solar every year for the next 5 years, and in addition to this there is the PM-SURYA yojna as well.

- Increasing Adoption of Solar Power: Solar energy costs continue to decline, making it an increasingly attractive option corporates as well

Positives:

- Attractive Valuation: With a market cap of only 1200 crore despite significant expansion plans, Solex could be undervalued (assuming they execute their plans effectively).

- Import Curbs: Recent import curbs by the Indian government (After modules, govt now considering non-tariff barrier for solar cell imports | Today News ) and the US government on solar panels from China could benefit domestic manufacturers like Solex by reducing competition, and opens US market for export.

Negatives:

- Execution Risk: Successfully implementing such a large capacity increase is crucial for their growth plans.

- Competition: The solar panel market is competitive in India itself, with established players and new entrants vying for market share.

Immediate Triggers:

- Strong FY Sales: By the end of this fiscal year, strong sales figures could lead to a re-rating of the stock price.

Risks:

- Commodity Price Fluctuations: Solar panel production relies on materials like silicon, whose price fluctuations can impact profitability.

- Trade Policies: Government trade policies can affect import costs of raw materials or finished panels.

- Chinese Threat: The dominance of Chinese manufacturers in the solar panel market can never be ignored.

- Increased Competition: A strong ramp up in capacity by many other players can also intensify competition in the market.

Summary:

The stock seems like a buying oppurtunity given it’s low valuation of just 1200cr, which seems undervalued given it’s plans to reach 4.5GW of capacity, provided Chinese import curbs stay in place in India and in US till FY27 at least.

Nithin’s Portfolio (31-05-2024)

Kenneth Andrade’s Recent Interview

- Capital Goods & Capex Dominated stocks are trading to significant premium where any of the large consumers.

- 4 Pharma companies as top 10 holdings : World’s generic manufacturer and capex cycle is almost year, over the course of last 5 years the industry has cleaned up its balance sheet and they are net positive. The ability to generate significant amount of profitability from the existing capex. 2024-25 will be years where this industry will hit its all time high terms of profitability and cash flow generation. Growth + category leaders + balance sheet + favorable valuation.

- Banks & Finance : Kenneth doesn’t have them as he mentions its an historic trade – he chose to be on asset side and not on liability side.

- His Macro Trade/Directional trade would be capex and industrials

- Breadth of the non capex/industrial is narrowing significantly.

- He states that his bet is not on industries but on capex themes

- Global Cycle : Metals/Export/Pharma – Global GDP growth is held up by defense, industrial capex, Governments are going to be largest spenders, consumers are taking back seat due to inflation

- Government put their balance sheet to work on capex side on rebuilding the entire industry, they will have to generate cash (i.e. were the inflation cycle is sitting)

- Kenneth is favorable on commodity, defense.

- IT companies : Significant hiring done with expectation for growth – now cutting down the head counts. IT will be in static phase

- With respect to the power/railway or others – everything boils down to commodities – which can generate huge free cash flow (so he is more interested towards metals, steel, bearings)

- New age companies : Zomato/Paytm – he plans to buy on second cycle, waiting for market to mature and markets correct. – tracking radar.

- Consumer : The valuation is not favorable

- Chemical market is fairly stressed across globe especially agro chemicals

- Consumer space : Middle class is heavily stressed, household debt – consolidation will happen – tracking.

- EV/Energy Transition/Climate Change : Not participating will wait for second cycle

- Generic Pharma/Pharma is mapping to the entire IT cycle that the IT has been through since. Pharma is the lowest cost manufacturer, getting market share from international business, US companies (generic business are extremely leveraged), Balance sheet of Indian companies are in favor, Interest rate going up in US,

India has the physical capacity + Financial capacity = where US has got none.

HDFC Asset Management Company (31-05-2024)

I get that. But if they call it as interim dividend, shouldn’t it be for FY25 and not FY24?

HDFC Asset Management Company (31-05-2024)

They have declared a new interim dividend, instead of the final dividend. They have not said anything about the final dividend in the above notice. Maybe as they are declaring a new interim dividend of same amount, maybe there won’t be the final dividend. Or, they will give both.

Not invested.

HDFC Asset Management Company (31-05-2024)

Does anyone understand what this means? In the last board meeting, company declared a final dividend of Rs. 70 per share as the final dividend for the completed year FY 24. Now they want to meet next week and re-declare it as an interim dividend for FY24. If the intention is to declare multiple dividends in one fiscal year, that is good news (especially if they also anticipate much higher profit growth). But why would declare it as interim dividend for FY24. Would make sense calling it so for current year

IZMO- bet on new technologies in Auto retail & defence (31-05-2024)

The company is not showing any significant FCF, it’s increasing intangible asset ( the quality of asset may only be known to the insiders) and nil dividend are some worrisome things for me. It had also promised some equity sell of its one of the US subsidiary (Frog Data) before FY 24 but didn’t update on that.